Rapid Micro Biosystems Pursues Growth Despite Sustained Operating Losses and Supply Challenges

Rapid Micro Biosystems advances automated microbial quality control (MQC) with its Growth Direct platform, but financial losses and strategic risks persist.

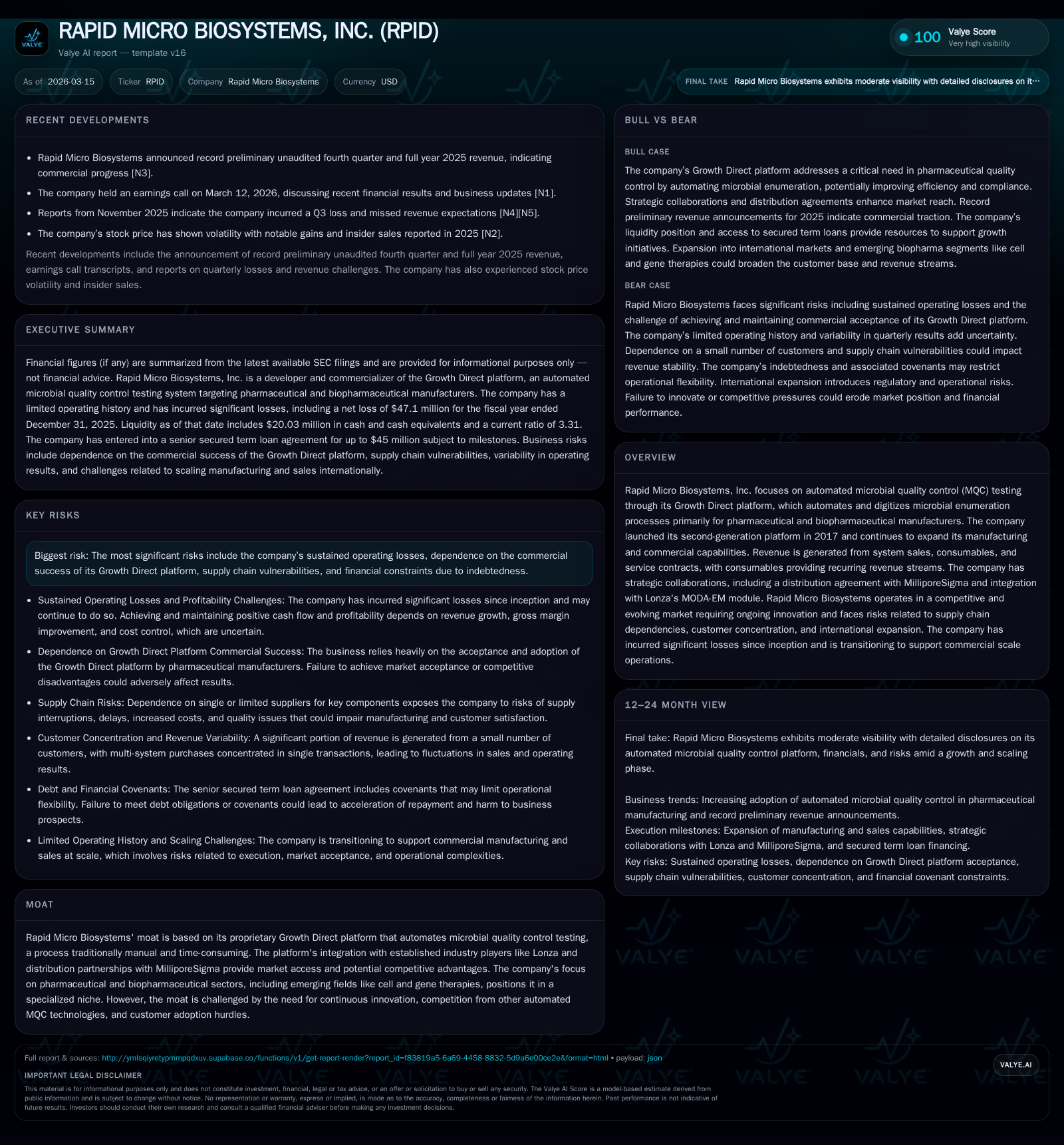

Rapid Micro Biosystems, Inc. centers its business model on the proprietary Growth Direct platform, aiming to automate microbial quality control testing for pharmaceutical and biopharmaceutical manufacturers. Since launching its second-generation system in 2017, the company has steadily increased revenue, driven by system placements and recurring consumables sales; however, it continues to incur substantial operating losses. Strategic collaborations and international expansion underpin growth ambitions but introduce operational and regulatory complexities. Capital requirements remain significant, with a newly arranged secured credit facility backing operational funding amid ongoing negative cash flow.

Company Overview and Historical Performance

Rapid Micro Biosystems has carved a niche within the automation of microbial quality control (MQC) testing through its proprietary Growth Direct platform. This technology digitizes traditionally manual microbial enumeration processes used predominantly by pharmaceutical and biopharmaceutical manufacturers. The firm launched its second-generation platform in 2017, which remains the backbone of its current commercial offerings [S1].

Financially, Rapid Micro has experienced modest top-line acceleration amidst continued operating losses: product and service revenue grew approximately 19.7% year-over-year (YoY) from $28.1 million in 2024 to $33.6 million in 2025 [F1]. This revenue mix features increasing contribution from recurring revenues tied to consumables sales—a critical element for predictable cash flow—growing by roughly 15.5% YoY to $17.8 million at the end of 2025 [S1]. System placements also rose from 21 to 28 during that period, with cumulative placed systems climbing to 190 units [S1].

Despite these gains, operating income deficits remain large though progressively narrowing; the operating loss declined to $47.4 million in 2025 from $49.9 million in 2024—a modest 5.1% improvement [F1]. Net loss followed similar trends despite incremental revenue growth, signaling ongoing investments in scaling manufacturing capabilities, expanding commercial presence, product development efforts, and navigating regulatory approvals [S1].

Operating cash flow improved somewhat—from a negative $44.2 million in 2024 to negative $31.1 million in 2025—but Free Cash Flow remains significantly negative ($-31.9 million), reflecting low capital expenditure needs relative to operational burn [F1]. The company’s capital structure shows equity depletion from accumulated deficits totaling over $522 million since inception as of December 31, 2025 [F1]. However, liquidity appears stable for now with a cash balance of approximately $20 million and a strong current ratio of about 3.3x as of FY-end [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -47 | -31 | -47 | 1 | -0.5% |

| 2024 | -47 | -44 | -50 | 1 | +10.6% |

| 2023 | -52 | -45 | -57 | 2 | +13.7% |

| 2022 | -61 | -59 | -63 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -32 | -141.9 |

| 2024 | -46 | -62.2 |

| 2023 | -47 | -44.5 |

| 2022 | -65 | -37.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue growth is robust while net income marginally improved but remains negative.

Strategic Positioning and Moat Analysis

Rapid Micro’s defensive moat fundamentally derives from its automated Growth Direct platform that modernizes MQC testing by reducing labor dependency while boosting throughput accuracy—a traditionally slow process often constrained by manual plate counting methods [S1]. Integration agreements with influential life sciences entities such as MilliporeSigma (distribution partner) and Lonza (system integration via MODA-EM module) provide vital market penetration footholds that may discourage new entrants lacking similar alliances [N1][S15][S18].

The company’s focus on pharmaceutical quality assurance dovetails with increasing regulatory pressure demanding stringent environmental monitoring during biologics manufacturing—including emerging modalities like cell and gene therapies—thus expanding opportunity though also raising competitive complexity [S1]. Nevertheless, proprietary technology must continuously evolve amid intensifying competition from other established automated MQC platforms leveraging imaging analytics or molecular biology techniques.

Risks Highlighted by Regulatory Filings

A confluence of operational challenges weighs on Rapid Micro’s growth profile:

Financial Sustainability: The company has historically operated at net losses (~$47 million in FY25) with worsening accumulated deficits exceeding half a billion dollars since inception [F1][S1][S2]. Despite strategic cost-savings measures initiated mid-2024 including workforce reductions, operating costs may rise as commercial activities scale, casting uncertainty on reaching consistent profitability [S2].

Customer Concentration & Supply Chain Dependence: The business relies heavily on repeat purchases of consumables tied directly to placed systems—any disruption here or loss of major customers could materially impact revenues [S15][S18]. Furthermore, global supply chain volatilities necessitate robust mitigation strategies given the precision components required.

Intellectual Property Threats: Rapid Micro faces typical biotech hardware industry risks surrounding patent infringement claims—noted as potentially costly litigation that could divert management focus or restrict commercial rights—and risks related to ownership disputes over patented innovations developed internally or via collaborators [S6][S13][S17].

Regulatory Compliance & International Expansion: Efforts targeting global markets expose the firm to diverse legal regimes requiring stringent quality-system compliance; non-adherence could lead to penalties or reputational damage limiting customer adoption outside core geographies [S22][S24].

Warranty Exposure: Standard one-year warranties on Growth Direct systems carry repair/replacement cost risks which must be closely monitored to avoid unexpected financial strains [S18][S24].

Future Growth Catalysts and Constraints

The company plans to expand its installed base significantly beyond the current cumulative validated systems (~155 units) leveraging advanced sales channels including expanded collaborations with MilliporeSigma globally alongside direct sales efforts targeting pharmaceutical manufacturers primarily across North America, Europe, and Asia-Pacific markets [S1][N1]. Additionally, further technological enhancements—including improving software analytics associated with Growth Direct—and packaging capacity upgrades aim to streamline production economics enhancing gross margins which rose from -24% in FY23 approaching positive territory at ~3% in FY25 signaling improving unit economics albeit early stage [F1][S1].

Challenges remain: successful penetration depends heavily on broader industry willingness to adopt automated MQC solutions replacing legacy manual methods entrenched due to regulatory inertia or customer conservatism; overcoming these adoption hurdles requires concerted educational outreach backed by demonstrable data efficacy gains [S1][N1]. Supply chain disruptions impacting component availability or rising costs due to inflationary pressures could constrain margins unexpectedly as well.

Forecasts, Milestones & Guidance Considerations

Explicit guidance is limited; management emphasizes system placements growth as a near-term KPI driving future recurring revenue streams from consumables usage [S1]. Maintaining an uptick in validated systems signals health of recurring revenue pipeline given typical multi-month validation cycles post-placement—a key operational focus area moving forward.

Recent announcements include multi-system orders from Samsung Biologics expanding client diversity alongside deeper commercial engagement; such high-profile accounts help validate technological value proposition albeit contribution timing is subject to order fulfillment schedules [N1][S3].

Watchpoints include quarterly system placements variability influenced by customer site construction timing or unexpected delays affecting installation schedules; consistency here will indicate more predictable revenue cadence over time.

Capital Allocation and Financial Returns Analysis

No dividends or share repurchases have been reported given ongoing investment phase consistent with negative profitability metrics [F1]. Return on equity is deeply negative (approximately -142% using reported net loss vs equity end of FY25), highlighting structural losses typical for developmental-stage biotech instrumentation enterprises still scaling commercial models.

The August 2025 Loan and Security Agreement provides committed up-to $45 million term loan financing supporting near-term liquidity underscores corporate reliance on external capital markets for operational continuity pending profitable inflection point achievement [S11][S16]. Covenants inherent in this facility limit financial flexibility including prohibitions on dividend payments or incurrence of additional debt without lender consent.

Capital expenditures remain modest (~$850k in FY25), focusing on equipment upgrades rather than large-scale facility expansions consistent with asset-light digital hardware manufacturing aligned with SaaS-like consumables revenue synergy model [F1]. Future capital needs will depend largely on scale-up pace beyond existing facilities.

Conclusion

Rapid Micro Biosystems operates at the convergence of life sciences automation innovation moderated by persistent financial headwinds typical for pioneering medical device companies transitioning toward commercialization scale-up phases. Its proprietary Growth Direct platform combined with strategic distribution partnerships positions it well within pharmaceutical microbial testing automation niches undergoing secular transformation.

Yet significant uncertainties remain surrounding path to sustainable profitability amidst persistent operating losses nearing $50 million annually and risks spanning supply chains, intellectual property defenses, regulatory compliance complexity internationally plus concentrated customer dependencies.

Success hinges upon more widespread adoption of MQC automation technologies coupled with effective cost controls improving gross margins beyond recent modest positive trends while managing working capital prudently under debt agreements constraining flexibility.

Investors should monitor system placement trajectories following recent major orders like Samsung Biologics alongside margin trends and progress toward validating larger installed base units activated for recurring consumables consumption that underpin longer-term revenue visibility.

This report is intended solely for informational purposes based on publicly available documents without any form of investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments