Shimmick Corp’s Transition Challenges Highlighted by Backlog Growth and Profitability Pressures

Despite backlog expansion and new business initiatives, Shimmick Corp posted significant operating losses in fiscal 2025, reflecting execution risks amid its infrastructure focus.

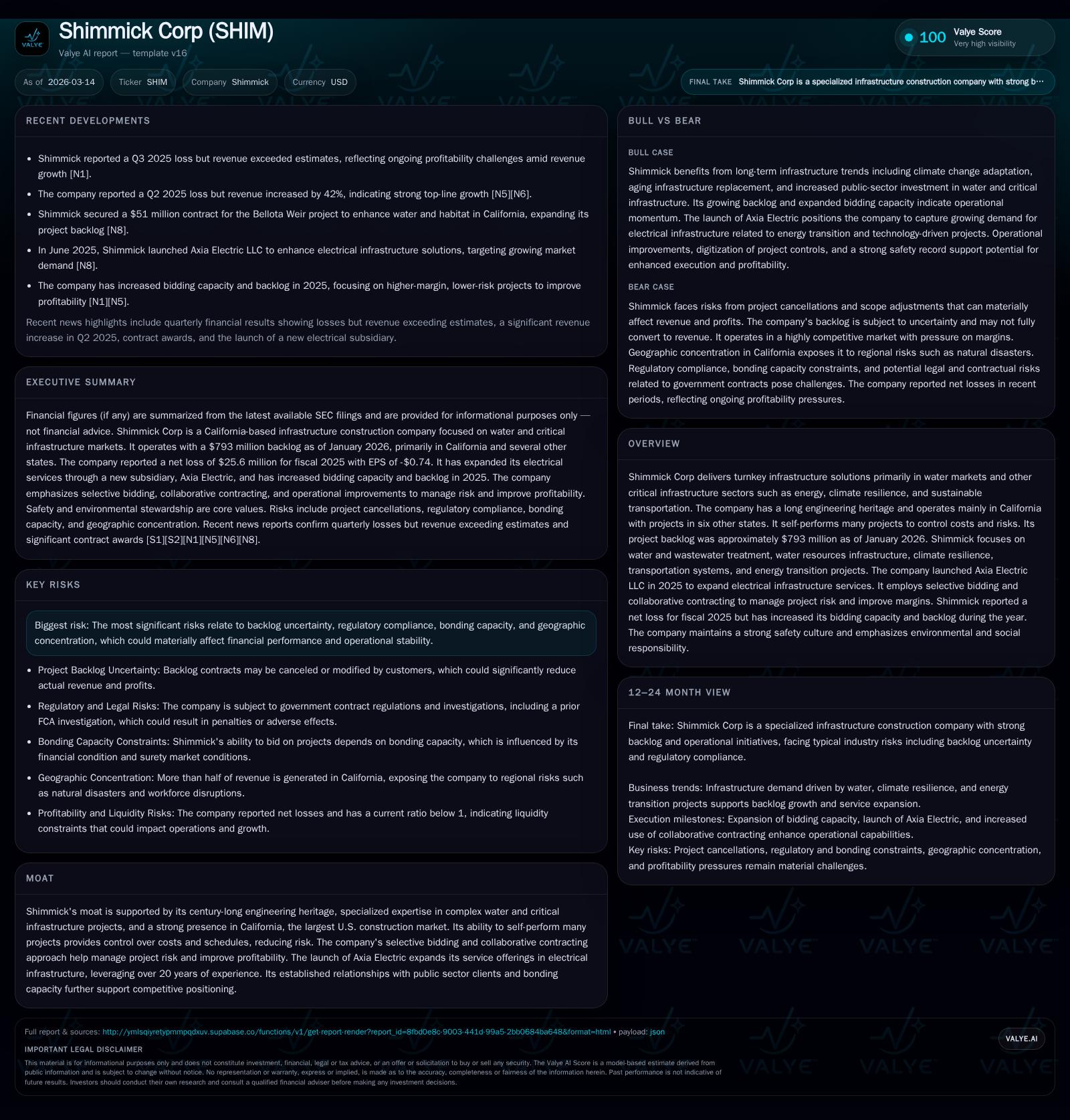

Shimmick Corp, a century-old infrastructure contractor specializing in water and critical infrastructure projects mainly in California, has increased its project backlog to approximately $793 million as of early 2026. However, fiscal 2025 saw a deepening net loss of $25.6 million and negative operating cash flows, underscoring operational challenges during its post-spinoff transformation. The company is focusing on selective bidding, collaborative contracting, and expanding electrical infrastructure services through Axia Electric to improve margins and growth prospects. Key risks include backlog uncertainties, regulatory compliance, bonding capacity, and geographic concentration.

Company Overview and Historical Performance

Shimmick Corp is a turnkey infrastructure solutions provider with a deep engineering heritage exceeding a century, primarily active in California's water markets alongside critical infrastructure sectors such as energy transition, climate resiliency, and sustainable transportation [N/A][S20]. Historically part of AECOM until its divestiture in 2021, Shimmick completed its IPO in late 2023 and has since been independent under new ownership [S20].

The company's operational model emphasizes self-performing key project components to maintain control over costs and schedules while pursuing selective bidding strategies to manage risk exposure effectively [S1][S8]. Its project backlog reached approximately $793 million as of January 2, 2026—a notable expansion supported by increased bidding capacity and pipeline growth focused on mitigated-risk projects replacing high-risk legacy contracts inherited from AECOM [S10][S11].

A summary of key financial metrics captures the stark transition Shimmick has undergone:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|---|

| 2025 | -26 | -65 | -19 | 6 |

| 2023 | -3 | -88 | 0 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -71 | 45.2 |

| 2023 | -95 | -3.6 |

Source: SEC companyfacts cache [F1].

(FY denotes fiscal year ended January; all figures from [F1])

Operating income swung dramatically negative by roughly 4560% compared to FY2023, accompanied by an even steeper deterioration in net income [F1]. Despite some improvement in operational cash flows (a reduction in negative CFO by about 26%), liquidity remains constrained as indicated by the sub-1 current ratio of approximately 0.89 at year-end (current assets $175M vs current liabilities $196M) [F1][S21]. Capital expenditures declined slightly but remain around $6-7 million annually.

Growth Prospects

Shimmick's future growth hinges largely on strategic execution within its core markets—water/wastewater treatment, water resource infrastructure (including dams/reservoirs), climate resilience efforts, transportation systems upgrades, and an expanding foothold in energy transition through newly formed subsidiaries such as Axia Electric LLC launched in June 2025 [S11]. Axia Electric aims to capitalize on specialized electrical contracting opportunities driven by EV fleet accommodations, renewable energy integration into projects, data center constructions, and power distribution solutions [S11][S8]. This builds on Shimmick's track record of over twenty years self-performing electrical work within its project portfolio.

The company has deliberately shifted away from large-scale, higher-risk contracts received under former ownership toward smaller-mid sized engagements that yield improved margins—enabled substantially through selective bidding processes combined with collaborative contract structures emphasizing early partnership between client and contractor to mitigate design errors, manage cost overruns proactively, and optimize schedule adherence [S8]. Increased representation of such collaborative contracts within backlog should help stabilize profitability in coming years.

Federal/state funding trends supporting infrastructure modernization amidst climate change adaptation create an addressable market estimated at roughly $1.5 trillion U.S.-wide for infrastructure construction alone with mid-single digit growth expected over next decade—a favorable backdrop for Shimmick’s growth ambitions given its positioning in California (largest U.S construction market) plus programs focused on water security and resilience projects [S4].

Forecasts and Milestones

Explicit guidance is not provided in disclosures; however, management emphasizes ongoing backlog expansion aligned with increased bidding capacity and pipeline quality improvements toward less risky projects that foster stronger profitability profiles—expectations being that growth can be sustainably fueled organically or via bolt-on acquisitions targeted towards complementary services within critical infrastructure segments [S10][S11]. Notably, cautious approach persists regarding backlog cancellations or modifications inherent with government-funded contracts that represent ~96% prime contract share of backlog—these factors inject uncertainty about future revenue realization timing or magnitude despite encouraging order book growth.

Areas warranting attention include execution progress on Axia Electric scaling efforts throughout calendar year 2026 alongside incremental shift toward more collaborative contracting models which should progressively reduce downside volatility tied to fixed-price project cost inflation or design omissions.

Returns and Capital Allocation

The company does not generate positive returns currently; net losses widened significantly impacting equity position which turned negative at -$56.6 million as of fiscal year-end—the implication being a deficit capital base relative to liabilities raising solvency questions if trends persist without corrective measures or external capital infusion [F1]. Return on equity calculation is not meaningful given this deficit.

Cash flow remains challenged with free cash flow approximating negative $71.5 million after adjusting operating cash flows for capital expenditure needs—the sizeable negative cash conversion signals working capital intensiveness typical of heavy civil construction intensified here by operational inefficiencies during transition phase [F1].

No dividend payments have been declared or anticipated given capital preservation priorities amid losses; share repurchase programs are also absent though the company has access to an 'At the Market' equity offering facility enabling up to $7.8 million issuance capacity potentially leading to dilution but essential for liquidity reinforcement if needed [S26].

Industry Positioning and Moat Considerations

Shimmick leverages longstanding engineering legacy dating back over one hundred years coupled with niche expertise spanning complex water-related infrastructure that supports environmental public health objectives—a combination strengthening its competitive moat particularly within California where entrenched customer relationships across municipal water districts and transit agencies create barriers for entrants [N/A][S20]. Self-performance capability further differentiates it by allowing stronger control over critical aspects such as labor productivity and supply chain coordination.

However, concentration risks are elevated due to geographic focus: more than half revenue originates from California exposing vulnerability to state-specific economic cycles or disasters such as wildfires which impacted operations previously in early 2025 inducing workforce disruptions affecting profit margins temporarily [S7][S29]. Diversification efforts into other states remain nascent requiring substantial resource investment with uncertain outcomes.

Competitive intensity remains high given multiple large national/international contractors chasing similar governmental contracts predominantly awarded through low-bid processes or increasingly via qualified contractor selections under collaborative delivery frameworks—mandating continuous innovation in bid strategy along with investment in technology and skilled personnel retention [S25].

Risk Profile Highlights

Material risks stem principally from backlog uncertainties since contracts are generally cancelable at customer discretion often with limited compensation beyond work completed—raising revenue realization doubts despite sizable gross backlog reported reflecting contractual total awards rather than secured profit streams outright [S10][S14]. Fixed-price arrangement exposure means unexpected cost overruns or inflationary pressures can quickly erode margins especially if change orders lag approvals.

Bonding limitations may restrict contract pursuit scale as surety support historically tied partly to prior owner AECOM’s credit profile which now requires Shimmick itself to establish sufficient bonding capacity—failure here would directly constrain project selection capabilities impacting top-line growth potential [S1][S23].

Legal/regulatory adherence presents perennial threat particularly concerning government contract compliance governed by EPA/OSHA standards plus False Claims Act scrutiny noted from closed DOJ inquiry revealing heightened oversight environment requiring robust internal controls lest penalties arise affecting reputation/cash flows adversely [S15][S19].

Dependence on subcontractors/suppliers amplifies execution risk intensity due to potential performance failures or price volatility especially tied to commodities essential for construction materials application—delays or cost surges could cascade financial impacts disproportionately on profit margins due to tight industry competition placing downward pricing pressure concurrently [S1].

Conclusion

Shimmick Corp's recent financials underscore significant growing pains during its post-divestiture transformation aimed at reshaping the company towards sustainable profitable growth emphasizing high-value water and critical infrastructure markets primarily concentrated geographically in California. The company’s strategic pivots including expanded selective bidding disciplines, rollout of specialized electrical services through Axia Electric LLC, and increasing footprint into collaborative contracting frameworks strategically align it well with evolving market demands fueled by climate resilience imperatives.

Nevertheless, the steep worsening of profitability metrics alongside net losses reducing shareholders’ equity into negative territory highlights considerable execution challenges ahead compounded by inherent industry cyclicality, contract cancellation risks and regulatory/compliance complexity endemic within public-sector reliant construction businesses.

Monitoring milestones related to backlog conversion quality improvements, Axia Electric scaling success as well as prudent liquidity management will be crucial for moving beyond the current deficit operating posture towards restoring positive returns.

This analysis is based solely on publicly available filings including Shimmick Corp’s SEC disclosures dated March 13, 2026 ([F1],[S#]) without any speculative projections or forward-looking statements beyond documented company communications referenced herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments