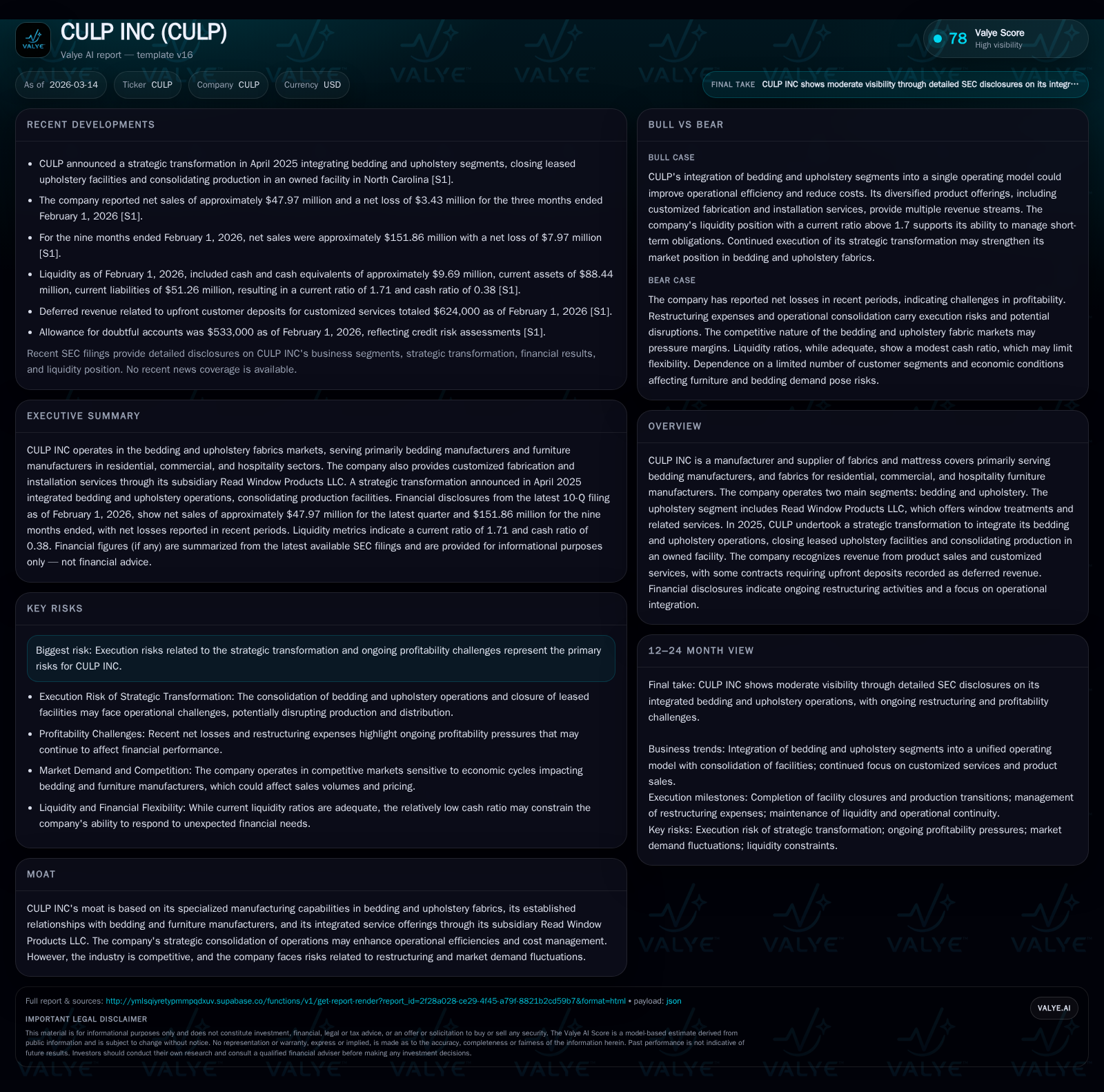

CULP INC’s Strategic Operational Overhaul and Earnings Trajectory

Evaluating the financial and operational impact of CULP INC's 2025 transformation amid continued profitability pressures.

CULP INC has experienced significant operational shifts following its 2025 strategic consolidation of bedding and upholstery segments, aimed at driving efficiencies. Historically, the company showed modest revenue growth but mounting operating losses culminating in a substantial FY2025 operating loss. The ongoing restructuring has pressured cash flows and profitability, with liquidity supported by a strong current ratio. Future performance hinges on successful integration completion and stabilized earnings, while risk remains from execution challenges and cyclical demand patterns. Capital return via dividends persists despite negative cash flows, highlighting cautious allocation in a turnaround phase.

Historical Growth Patterns and Underlying Drivers

CULP INC's historical financial performance exhibits a pattern of relatively stable top-line revenues paired with significant fluctuations in profitability. From FY2015 through FY2018, revenues hovered around $77 million to $78 million USD, displaying marginal year-over-year increases—specifically a 1.1% revenue growth noted between the most recent years available [F1]. However, this revenue stability belies growing challenges at the operating level. Operating income swung from mildly positive or breakeven levels in early fiscal years to pronounced losses thereafter.

Net income followed a similarly volatile path; net profits peaked at approximately $12.7 million USD in FY2018 but declined dramatically in subsequent periods, culminating in an operating loss of $18.4 million USD by FY2025 [F1]. The recent uptrend toward losses correlates with margin compression and restructuring-related charges that have negatively impacted EBITDA metrics.

Operational cash flows provide further insight into financial stress: after a positive operating cash flow year in FY2023 (+$7.8 million), CFO plunged to negative territory by FY2024 (-$8.2 million) and sharpened further to -$17.7 million in FY2025 [F1]. This decline signals challenges in working capital management and operational liquidity amid strategic shifts.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) |

|---|---|---|

| 2025 | -18 | -18 |

| 2024 | -8 | -11 |

| 2023 | 8 | -28 |

| 2022 | -17 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) |

|---|---|---|

| 2025 | ||

| 2024 | 6 | 1752000 |

| 2023 | 6 | 1752000 |

| 2022 | 6 | 1752000 |

Source: SEC companyfacts cache [F1].

*Dividends and buybacks reported through FY2024 [F1]

This pattern suggests that while top-line sales generation remains somewhat resilient due to established customer relationships and product mix stability, CULP struggles to convert sales into sustainable profits—a core challenge intensified by the operational upheavals initiated recently.

The 2025 Strategic Transformation: Operational Integration and Its Consequences

In Q4 fiscal 2025, CULP executed a strategic pivot by consolidating its bedding and upholstery manufacturing operations into a single integrated business model under one brand identity [N1][S9]. This transformation involved shuttering leased facilities previously dedicated to upholstery activities located in Burlington and Knoxville, North Carolina. Their functions were merged into an owned facility based out of Stokesdale, North Carolina.

This move addresses several pain points common in textile manufacturing: fragmented production footprints leading to inefficient fixed cost absorption and increased overheads from dual administrative structures. By uniting the bedding and upholstery units physically and organizationally, CULP aims for synergy realization through lean manufacturing principles such as waste minimization and enhanced throughput.

Operationally, such consolidation should enable optimized capacity utilization—better balancing labor deployment against equipment usage—and reduce redundant expenditures on facility leases or leased equipment maintenance liabilities [S9]. Moreover, tighter integration may expedite supply chain responsiveness given proximity benefits between fabric production and finishing stages.

However, these consolidation efforts typically incur short-term structural costs including employee severance expenses (noted as accrued restructuring), lease termination charges for former locations, and transition logistics overhead [S9]. The strain reflected materially in the FY2025 results with significant impairment charges impacting operating income negatively.

The company also leveraged the integration as an opportunity to better align its service portfolio through Read Window Products LLC—enhancing its capabilities for customized installation services alongside traditional fabric supply—which diversifies revenue streams but adds complexity to contract management owing to upfront deposits recorded as deferred revenue [S9].

Current Financial Position and Profitability Headwinds

CULP's most recent filings reveal ongoing headwinds linked both to restructuring costs and intrinsic profitability constraints within highly competitive specialty fabric markets [S2][S4][F1]. As of February 1, 2026, cash and cash equivalents stood at approximately $9.7 million USD against current liabilities of $51.6 million USD resulting in a healthy current ratio near 1.71—indicating sufficient short-term liquidity to meet obligations [F1].

Nevertheless, this liquidity is tempered by operating cash flow deficits that underscore persistent challenges managing working capital cycles amidst integration [F1]. Deferred revenue from customized services shows as contract liabilities on the balance sheet; these deposits contribute to working capital dynamics but also require precise scheduling of revenue recognition tied closely to service delivery timelines—generating variability in reported revenues quarter-to-quarter [S9].

On the debt front, revolving credit facilities remain a financing source complemented by supplier finance arrangements predominantly concentrated across US-based operations [S4][S9]. While these credit lines offer flexible liquidity buffers during restructuring phases, their cost implications affect net margins given interest expense accruals embedded within selling/general administrative outlays.

Restructuring accruals notably increased heading into FY2026 confirming that selected integration costs extend beyond initial projections impacting earnings negatively until full synergies unfold – increasing execution risk exposure [S2][F1]. Meanwhile, the shift away from multiple leased premises reduces future lease liabilities but raises transitional capital expenditure needs associated with plant enhancements supporting combined operations.

Outlook and Key Indicators for Future Performance

Explicit guidance remains absent from public disclosures—an understandable stance given transformational uncertainty—but qualitative commentary suggests focal points for monitoring recovery progress include:

- Completion of production transition phases eliminating legacy facility dependencies.

- Evidence of EBIT margin stabilization or improvement post-synergy cost offsetting.

- Trends in new orders particularly from core mattress OEMs and commercial furniture manufacturers who form mainstay client segments.

- Managing deferred revenue turnover reflecting efficient backlogs clearance without inducing service bottlenecks.

Stakeholders should track quarterly commentary on these milestones given their outsized influence on earnings trajectories amid competitive pressures noted industry-wide around price sensitivity for textile materials [N1].

Capital Allocation: Dividends, Buybacks, and Cash Flow Dynamics

Despite operational difficulties manifesting as multi-year negative cash flows from operations (-$17.7 million USD by FY2025), CULP has maintained a consistent dividend payout exceeding $5 million annually through recent periods alongside modest repurchase activity amounting around $1.75 million USD per annum up to FY2024 [F1].

This deliberate capital allocation signals management's intent to uphold shareholder value amid cyclical volatility while balancing investment needs tied to restructuring-related capital projects [F1]. The approximate return on equity stood near 9.8% as of recent filings—a modest figure reflective of profit dilution yet suggesting some capital efficiency relative to equity base size [F1].

Negative free cash flow trends underscore constraints on discretionary spending capacity with limited room for aggressive buybacks or expansions unless profitability inflects positively soon . Maintaining dividends under such conditions might stem from confidence in eventual turnaround or contractual shareholder expectations within cyclically sensitive specialty textile manufacturing sectors.

Competitive Moat and Industry Context: Specialty Manufacturing Nuances

CULP's competitive moat is rooted primarily in specialized fabric production tailored for bedding manufacturers alongside upholstery segments supplying residential through hospitality furniture markets—areas demanding both scale-grade textile quality control plus nimble customization abilities .

Read Window Products LLC adds an integrated service dimension providing window treatment fabrication/installations enhancing total solution offerings—resulting in increased customer stickiness due to multifaceted engagement beyond mere fabric supply chains .

Such integrated capabilities create switching costs not easily replicated by lower-cost commodity fabric producers thereby safeguarding niche market presence despite broader sector commoditization risks seen elsewhere. Product fulfillment agility matched with quality standards governs competitiveness especially where OEM consistency influences contract awards.

Risks from Restructuring Execution and Market Demand Fluctuations

The primary risks facing CULP derive from execution uncertainties around its consolidation strategy including potential cost overruns beyond anticipated severance or lease termination expenses which would erode expected synergy benefits. Disruptions during transition phases may impair supply reliability triggering client dissatisfaction risking order deferrals or cancellations.

Furthermore, cyclical demand inherent within B2B bedding/furniture sectors poses volumetric unpredictability influenced by macroeconomic factors like housing starts or hospitality capital expenditures affecting fabric consumption levels. Price competition pressures could compress margins further especially if rising raw material input costs are not fully recoverable via pricing adjustments.

Effective risk mitigation will involve disciplined project management as well as proactive customer engagement ensuring smooth contractual fulfillment tied closely to integration milestones.

Conclusion: Monitoring Metrics for a Stabilizing Turnaround

CULP INC’s path forward hinges critically on navigating through the synergy realization phase stemming from its ambitious operational overhaul launched in fiscal year 2025.[N1][S2][F1] Investors should watch carefully:

- Improving operating income trends reflecting declining restructuring charges.

- Positive inflections in EBIT margins signaling cost structure normalization.

- Stabilization or reduction in accrued restructuring liabilities providing clarity on transformation completeness.

- Operating cash flow turning positive indicative of restored working capital health.

While dividend continuity provides some reassurance on financial resilience during this cycle,[F1] negative cash flows reflect remaining headwinds necessitating cautious optimism rather than aggressive extrapolation of gains. Ultimately CULP’s niche technical fabric expertise combined with integrated services offers a credible platform for recovery once transitional frictions abate—pending successful structural execution against known risks.

Disclaimer: This report is prepared solely for informational purposes based on publicly available data as of March 14, 2026. It does not constitute investment advice or recommendations regarding securities ownership or transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments