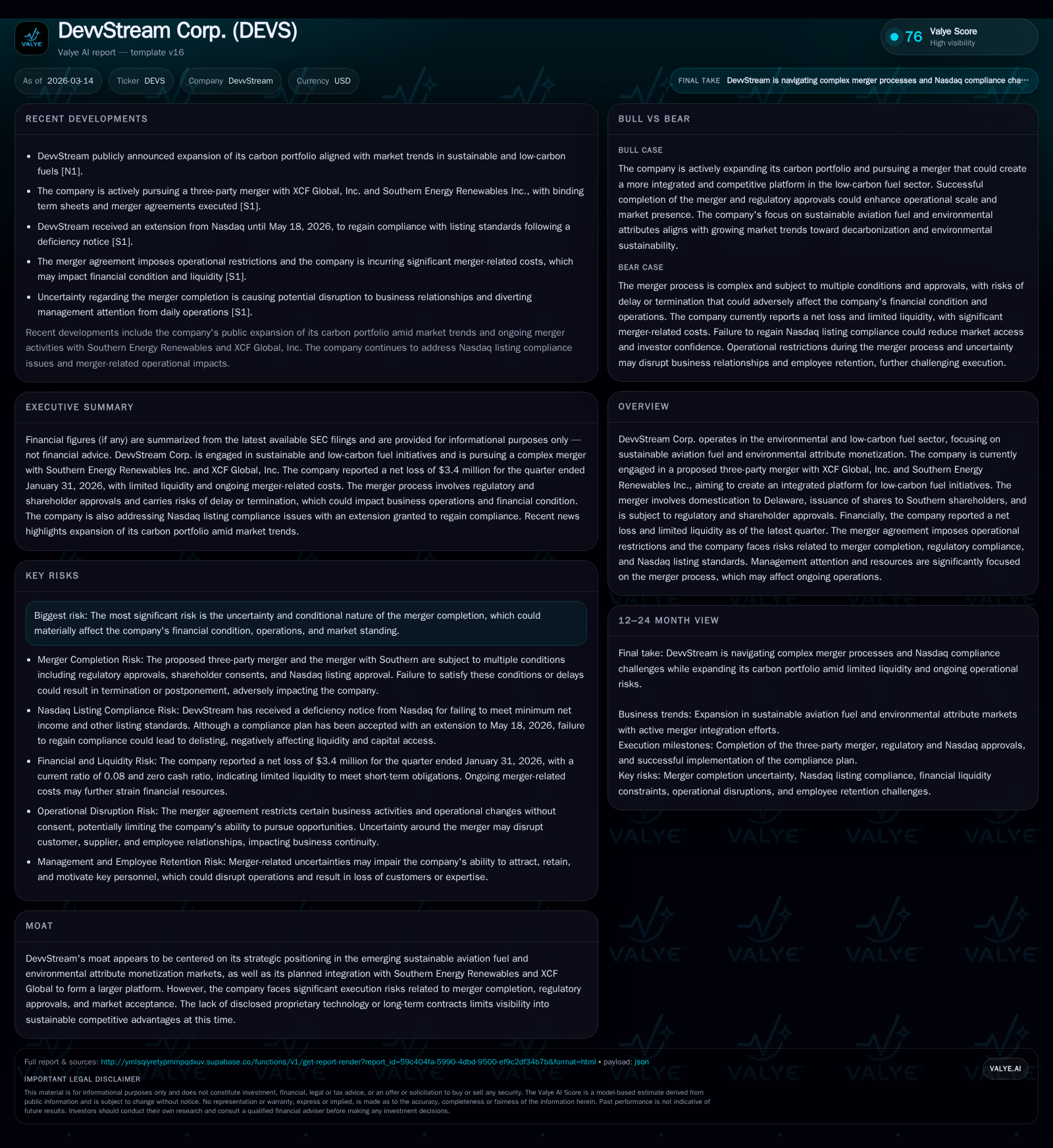

Merger Uncertainties and Liquidity Challenges Shadow DevvStream’s Growth Trajectory

DevvStream Corp.’s pursuit of a transformative merger in the sustainable aviation fuel space coincides with mounting financial and operational constraints.

DevvStream Corp. is actively pursuing a complex three-party merger intended to integrate sustainable aviation fuel (SAF) production and environmental attribute monetization capabilities, positioning itself within the emerging low-carbon fuels sector. However, its financial footing is precarious, reflected in sustained losses, negative operating cash flows, and acute liquidity shortages. The company faces substantial execution risks from merger-related operational restrictions, regulatory approvals, and Nasdaq listing compliance deadlines. These factors collectively limit near-term business flexibility and cast uncertainty over DevvStream’s growth prospects.

Historical Financial Performance: Revenue Growth Undermined by Steep Losses

DevvStream’s financial trajectory over recent fiscal years illustrates modest top-line increases clouded by escalating losses. Revenue as of FY2025 reached approximately $25.8 million [F1], indicating some degree of commercial traction or expanded operations. Despite this growth, profitability metrics depict deterioration: operating income worsened from a loss of $431 thousand in FY2021 to nearly $5.2 million negative by FY2023 [F1].

Most notably, net income plunged from positive results of about $11.5 million in FY2022 down to a loss exceeding $12 million in FY2025 [F1]. Operating cash flow similarly declined, registering roughly -$6.4 million in fiscal 2025 [F1]. This reflects unprofitable operations with cash burn exceeding internal generation capabilities, foreshadowing liquidity stresses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -12 | -6 | ||

| 2023 | 0 | -3 | -5 | -99.8% |

| 2022 | 12 | -1 | -2 | +201.1% |

| 2021 | 4 | 0 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 61.6 |

| 2023 | -0.3 |

| 2022 | -115.8 |

| 2021 |

Source: SEC companyfacts cache [F1].

The equity position is notably negative at approximately -$19.6 million as of FY2025 year-end [F1], underscoring accumulated deficits that compound risk and complicate capital access.

Strategic Focus on Sustainable Aviation Fuel and Environmental Attributes

DevvStream targets the sustainable aviation fuel (SAF) market alongside environmental attribute monetization such as carbon credits or Renewable Identification Number (RIN) credits—initiatives gaining momentum amid airline industry decarbonization mandates [N1].

The company aims to leverage biomass feedstocks like wood-waste for green methanol and carbon-negative SAF production through Southern Energy Renewables’ planned Louisiana facility [S26]. This strategy integrates physical fuel outputs with associated environmental commodity streams within emerging regulatory frameworks incentivizing renewable fuels.

Operational Constraints and Regulatory Risks Impacting Growth

Operational flexibility is restricted by merger agreement clauses requiring Southern’s consent for business activities until deal closure or termination [S8][S15]. This constrains pursuit of new commercial opportunities during potentially extended negotiations.

Regulatory risks include evolving SEC oversight on environmental claims verification alongside Nasdaq listing requirements related to stockholders’ equity minimums and market capitalization thresholds [S4][S9][S11]. Failure to meet these standards risks delisting with adverse effects on investor confidence.

Moreover, antitrust clearance under the Hart-Scott Rodino Act remains outstanding for the Southern merger completion [S7][S10], adding timing uncertainty.

The Proposed Three-Party Merger: Rationale and Execution Challenges

On January 26, 2026 DevvStream entered a binding term sheet with XCF Global Inc. and Southern aiming to establish an integrated platform focused on SAF production and environmental attributes monetization [S2][S23]. The plan includes domestication into Delaware law with Southern shareholders receiving approximately 70% ownership upon closing—a reverse takeover structure [S29].

Completion depends on definitive agreements acceptable to all parties plus customary closing conditions including regulatory approvals and shareholder consents [S7][S10]. Termination rights exist if milestones are unmet.

Support & lock-up agreements among major shareholders further underscore deal complexity by ensuring vote outcomes while restricting share transfers during this period [S21][S27]. Non-completion risks include market price declines, impaired supplier/customer relations, litigation exposure over breach claims, significant sunk advisory costs and operational distractions [S5][S8][S10].

Liquidity Crisis and Nasdaq Compliance Deadline Looming

As of January 31, 2026 interim reporting period end DevvStream held no cash equivalents with current assets around $2 million against liabilities exceeding $26 million yielding a critically low current ratio near 0.08 [F1][S4].

Nasdaq notified the company of deficiencies citing failure to meet minimum net income requirements compounded by insufficient stockholders’ equity or market capitalization alternatives [S9][S11][S28]. An extension was granted until May 18, 2026 for compliance remediation tied mainly to capital events related to the merger process [S3][S28].

Failure beyond this date risks delisting which would materially impact share price dynamics, liquidity for investors, institutional interest levels and capital access for DevvStream plus potential erosion of confidence among suppliers and customers [S4][S9].

Capital Allocation: Focused on Operations Amid Negative Cash Flows

The company has made no dividend payments or share repurchases consistent with typical development-stage profiles prioritizing reinvestment amid sustained negative operating cash flows reaching approximately minus $6.4 million most recently [F1][S22][S24].

Equity dilution arises from share issuances linked to merger arrangements where Southern shareholders will hold about 70% post-transaction control—typical of reverse mergers designed as recapitalizations [S27][S29]. Return-on-equity calculations based on losses relative to negative equity reflect poor earnings performance rather than value creation currently visible [F1].

Key Milestones Through 2026

Critical upcoming events include the May 18 Nasdaq compliance deadline extension expiration; September 3 cutoff for completing the Southern merger or extending it under specified conditions; finalizing definitive three-party merger agreements; obtaining required antitrust clearances; and monitoring liquidity improvements tied to capital raises or strategic partnerships [S2][S3][S10].

Investors should also watch developments such as bond financing approvals supporting Southern's biomass-to-fuel facility which could materially affect valuation dynamics post-integration [N1][S26].

Management’s Risk Acknowledgment Amid Transformational Challenges

Management discloses extensive execution risks surrounding transaction completion including regulatory hurdles; prolonged approval processes diverting resources; potential litigation threats; employee retention challenges due to role uncertainties; and strained vendor/customer relations driven by deal-related delays or hesitations [S5][S8][S10][S14][S15].

These disclosures reflect pragmatic awareness but highlight vulnerability inherent in transformative restructurings dependent on uncertain future outcomes rather than established momentum.

This analysis synthesizes facts drawn exclusively from available SEC filings ([F1],[S#]) and recent news sources ([N1]) without conjecture or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments