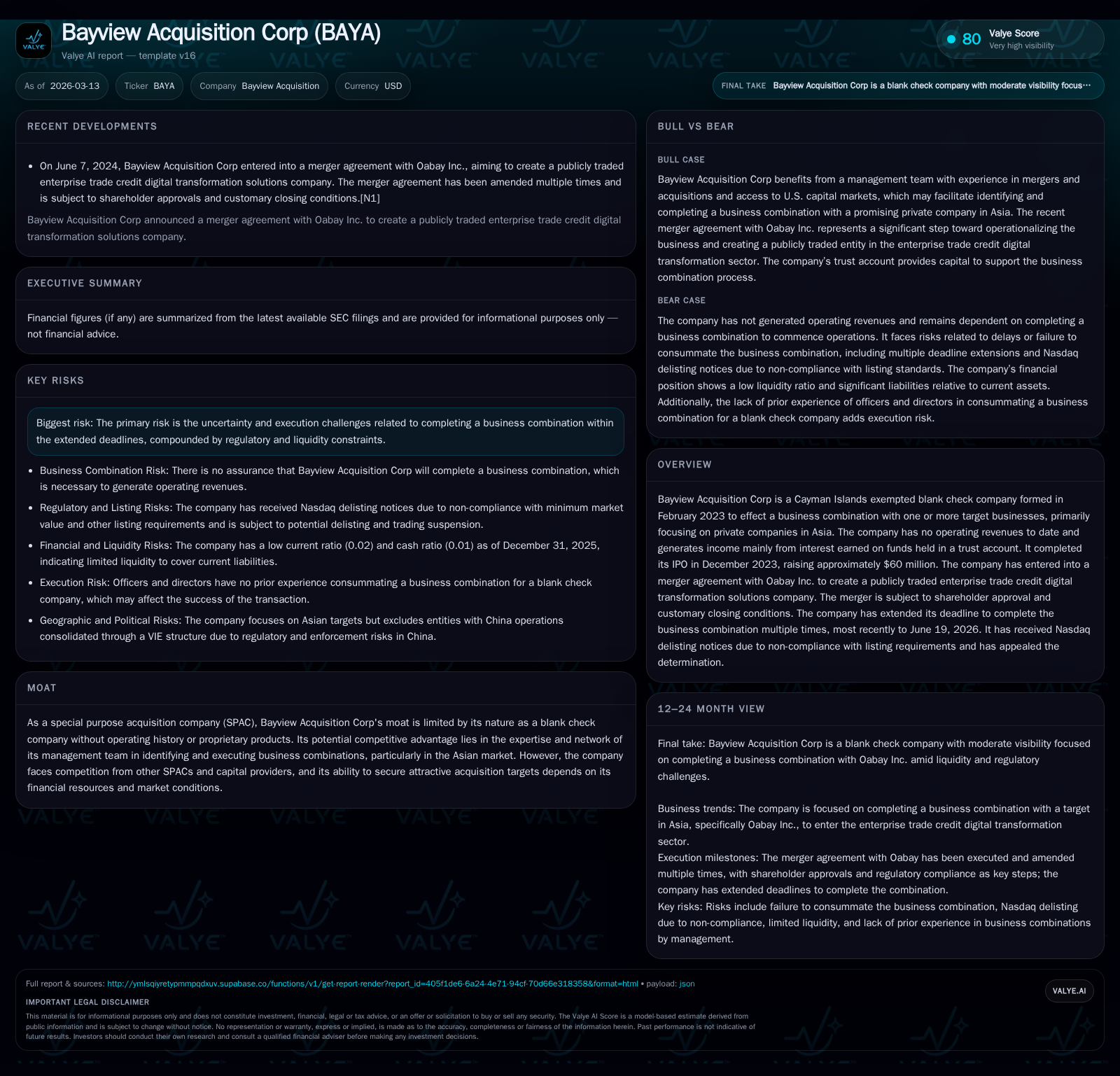

Bayview Acquisition Corp’s Capital Constraints and Merger Deadline Extensions Pressure SPAC Viability

Bayview Acquisition Corp, a Cayman Islands SPAC targeting Asian private companies, faces critical liquidity challenges and Nasdaq compliance issues as it extends its deadline to consummate a business combination.

Founded in early 2023, Bayview Acquisition Corp raised approximately $60 million in its December 2023 IPO, aiming to merge with Oabay Inc. to establish a digital trade credit solutions company. The SPAC has generated no operating revenues and relies solely on interest income from funds held in trust. It has repeatedly extended its business combination deadline to June 19, 2026, amid Nasdaq delisting notices over compliance concerns. The company carries working capital deficits and limited cash reserves while incurring significant costs related to the merger process.

Company Overview

Bayview Acquisition Corp (ticker: BAYA) is a Cayman Islands exempted blank check company established in February 2023. Its principal strategy is effecting a business combination focused predominantly on private companies located in Asia, leveraging what it describes as management expertise and networks within that region [S1]. Since incorporation, Bayview has conducted no operational activities or generated revenue; its financial results hinge entirely on interest income earned on proceeds held in trust following its IPO [S1].

The company completed its Initial Public Offering on December 19, 2023, selling 6 million units priced at $10 each and generating gross proceeds of approximately $60 million. Additionally, simultaneous private placements added $2.325 million in proceeds [S7]. These proceeds are held mostly in a trust account invested primarily in U.S. government securities or money market funds with short maturities to preserve capital and comply with SEC SPAC regulations [S7],[S14].

Concurrently with the IPO completion, Bayview entered into an agreement to merge with Oabay Inc., envisioned as a publicly-listed enterprise delivering trade credit digital transformation solutions [S1]. This merger remains subject to shareholder approval and customary closing conditions.

Historical Financial Performance

Bayview Acquisition Corp’s financial track record reflects startup-stage SPAC dynamics—no revenue generation but incremental net income from interest offsets rising operating costs related to general administration and business combination efforts.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 202599 | -49491 | -986503 | -88.4% |

| 2024 | 1752975 | -488688 | -1027170 | +1949.9% |

| 2023 | 85516 | -4410 | -21539 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 30 | -3.7 |

| 2024 | 24 | -53.8 |

| 2023 | -4.9 |

Source: SEC companyfacts cache [F1].

Table: Bayview Acquisition Corp annual financial summary [F1]

Operating losses have remained stable between FY24 and FY25 amid ongoing administrative expenses necessary for regulatory compliance and deal preparation. Net income declined sharply by approximately 88% year-over-year mainly due to reduced interest income as trust account balances decreased because of public share redemptions and extension payments [F1],[S20]. Operating cash flows remain negative reflecting continuous pre-transaction expenditures.

Buybacks reflect substantial redemption of public shares by shareholders exercising their rights prior to consummation of the business combination—a typical liquidity pressure point for SPACs [F1].

Shareholders’ equity was negative $5.5 million at year-end 2025 compared with negative $3.25 million at end-2024 due to cumulative net losses and redemptions impacting retained earnings [F1]. This implies an approximate return on equity (ROE) of -3.7% using latest annual net income against equity.

Business Model & Strategic Direction

Bayview operates as a blank check company raising capital through an IPO aimed at acquiring or merging with a private target primarily in Asia. Management emphasizes Asia’s expanding private sector growth and technology adoption as key acquisition drivers [S15].

The company excludes targets with China operations consolidated via VIE structures due to regulatory complexities [S15]. The management team brings M&A experience across jurisdictions focused on creating value through U.S. capital markets access post-merger.

The planned transaction with Oabay Inc., specializing in enterprise trade credit digital transformation solutions aligned with fintech innovation themes, represents Bayview's pathway toward operational revenues pending merger closure [N/A].

Growth Prospects & Constraints

Growth depends on successful completion of the initial business combination which would convert Bayview into an operational public entity. The merger with Oabay Inc., if completed by the extended deadline of June 19, 2026, could enable revenue generation leveraging Oabay’s digital platform capabilities [N/A].

Constraints include:

- Multiple deadline extensions requiring incremental deposits into the trust account.

- Liquidity pressures from share redemptions reducing available funds against fixed overheads.

- Nasdaq delisting risks triggered by non-compliance with listing standards creating uncertainty over continued listing status [S15].

- Competitive SPAC landscape targeting Asian companies possibly inflating acquisition valuations or limiting affordable opportunities.

Ongoing costs cover legal fees, regulatory reporting obligations (~$120k annually for office rent plus other general overhead), audit fees (UHY LLP), finder’s fees payable upon deal closing (600k combined shares), director & officer insurance premiums—all cumulatively increasing cash burn before operational cash flow commencement [S22],[S17],[S28].

Capital Structure & Liquidity Analysis

Bayview’s capital originates from sponsor contributions totaling roughly $2.33 million for founder shares plus approximately $60 million IPO proceeds invested conservatively under SEC SPAC rules [S7],[S24].

Public shareholders’ redemption activity reduced trust assets from nearly $40 million at end-2024 to about $11.7 million at end-2025—a significant contraction affecting deal financing capacity [F1],[S14].

The company has issued unsecured promissory notes over $2 million from sponsors or affiliates covering extension payments and transaction costs; however these loans are limited and non-obligatory beyond stated amounts [S6],[S20],[S23].

Cash outside the trust is minimal ($44k at end-2025) against current liabilities exceeding $3.4 million largely comprising accrued legal and administrative expenses indicating strained near-term liquidity [F1],[S8].

Nasdaq listing fees (~$55k annually) add recurring financing demands until merger completion unlocks operational cash flows or alternative funding is secured.

Returns & Capital Allocation

As a pre-merger SPAC entity Bayview's returns metrics are constrained; approximate ROE is negative reflecting operating losses against small equity base impacted by redemptions and accumulated deficits [F1]. There have been no dividends declared nor discretionary buybacks aside from share redemptions executed under redemption rights.

Capital allocation prioritizes merger deadline extensions (each requiring a $50k deposit into trust), legal/due diligence expenditures necessary for transaction progress alongside NASDAQ compliance costs [N/A][S20].

No evidence exists of dividends or discretionary buybacks beyond public shareholder redemptions—appropriate given the non-operational mandate focused strictly on completing the initial business combination without extraneous capital distributions.

What To Watch For: Milestones & Risks

Key milestones include:

- Outcome of March 31 Nasdaq hearing contesting delisting orders influencing continued U.S market access risk [N/A],[S15];

- Shareholder vote approval on merger terms;

- Finalization of definitive agreements clarifying post-combination capital structure;

- Securing additional financing if required;

- Regulatory developments impacting Asian market access relevant to target operations;

- Integration execution risk given management’s lack of prior operating experience post-merger;

- Potential dilution risk from outstanding rights or convertible instruments tied to deal consideration.

These factors underscore typical early-stage blank check firm uncertainties compounded by competitive pressures within Asian tech sectors during volatile macroeconomic periods.

Conclusion

Bayview Acquisition Corp typifies geographically focused SPACs pursuing Asian private growth via public markets. It raised sufficient initial capital but confronts challenges including declining trust assets due to redemptions alongside costly regulatory compliance burdens straining finances pre-business combination closure.

Its strategic partnership with Oabay Inc., while providing direction toward operational revenue generation, remains contingent on favorable governance outcomes like Nasdaq listing retention and shareholder approvals within compressed extended timelines through mid-2026. The firm's viability hinges critically on successful deal closure avoiding liquidation scenarios where accumulated costs might outweigh remaining resources.

Investors should monitor how effectively Bayview manages capital runway extensions amid growing pressures from competitive M&A landscapes while preparing for operational buildout stages post-merger.

This analysis reflects information available as of March 13, 2026. It does not constitute investment advice but aims to provide comprehensive insights grounded solely in disclosed data sources detailed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments