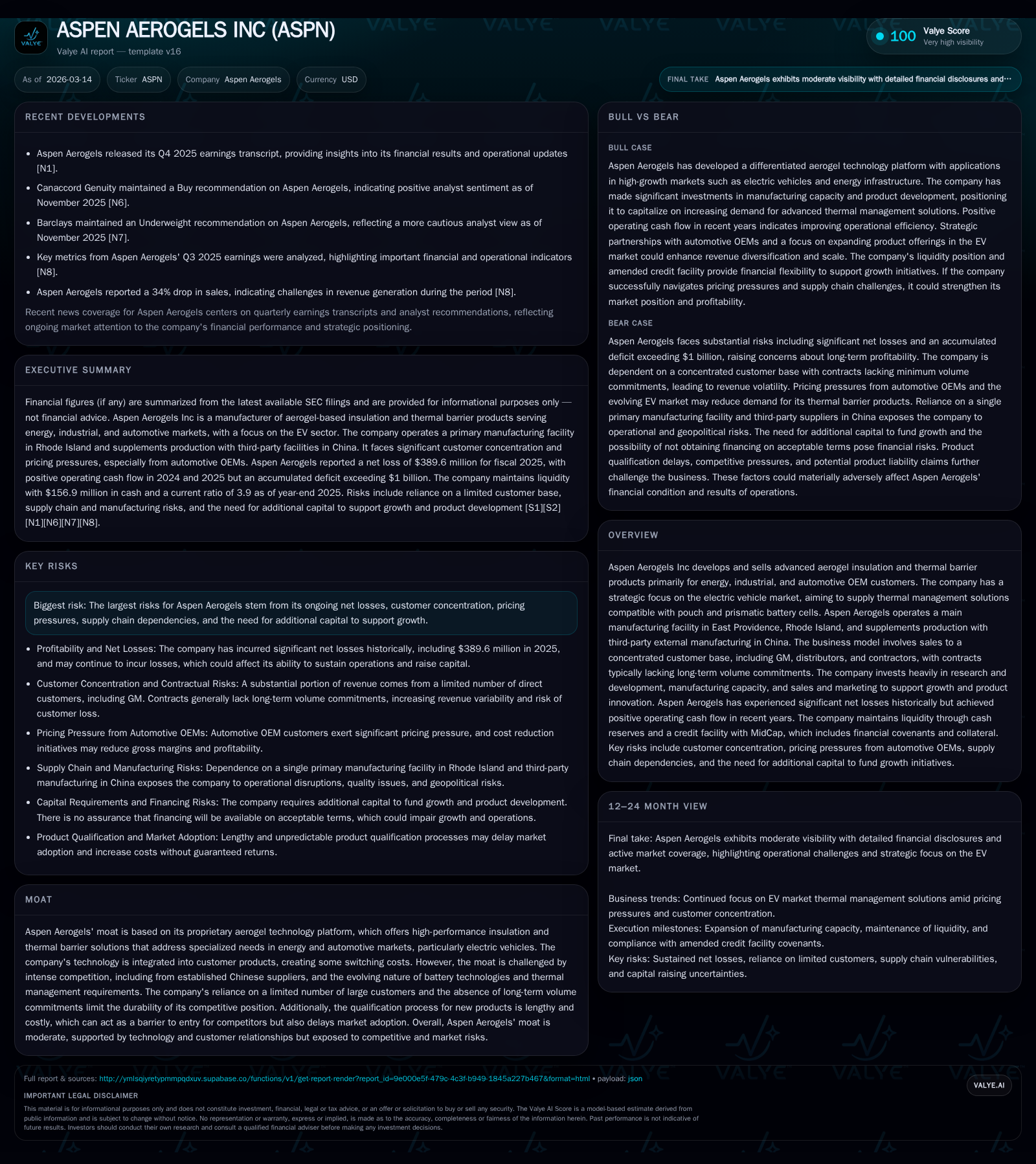

Aspen Aerogels' Financial Reversal: Balancing Innovation and Losses in Thermal Solutions

Aspen Aerogels achieves positive operating cash flow amid large net losses driven by R&D investments and market challenges.

Aspen Aerogels experienced a sharp increase in revenues with a 31.6% year-over-year gain through 2025 but reported a significant operating loss of $378 million. The company’s core technology platform in aerogel insulation supports a moderate competitive moat, particularly in EV battery thermal management, though patent litigation and evolving technologies pose risks. Despite heavy investment in manufacturing and R&D, Aspen’s capital structure shows strain with negative returns on equity and covenant pressures. Close monitoring of customer concentration, supply chain dependencies, and patent disputes will be crucial as Aspen balances its innovation ambitions against operational losses.

Historical Growth Patterns and Key Revenue Drivers Through 2025

Aspen Aerogels’ financial history portrays stark fluctuations reflecting its transition from developmental phases toward commercialization. Revenue was $36.4 million in FY2017 ([F1]) with a 31.6% year-over-year increase recorded for FY2025 compared to the prior period ([F1]). However, this top-line growth accompanied an extreme operating loss of $378 million in FY2025 ([F1]), highlighting that increased sales volumes have not yet translated into profitability.

The divergence between positive operating cash flow ($32.9 million) and deep net losses (-$390 million) underscores capital-intensive investments primarily aimed at expanding manufacturing capabilities and driving research & development initiatives ([F1]). Capital expenditures remained significant at $37.4 million despite declining from prior peak levels.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -390 | 33 | -378 | 37 | -3012.5% |

| 2024 | 13 | 46 | 55 | 86 | +129.2% |

| 2023 | -46 | -43 | -49 | 175 | +44.6% |

| 2022 | -83 | -94 | -79 | 178 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -165.4 |

| 2024 | -41 | 2.2 |

| 2023 | -218 | -9.4 |

| 2022 | -272 | -18.5 |

Source: SEC companyfacts cache [F1].

The reversal from positive operating income and net income in FY2024 to deeply negative results in FY2025 signals intensified spending likely related to scaling production facilities and advancing product pipelines into sectors like electric vehicle (EV) thermal management.

Technology Edge in Aerogel Insulation: Strengths and Competitive Pressures

Aspen’s core advantage lies in its proprietary aerogel insulation platform designed for demanding energy efficiency applications across industrial sectors including automotive OEMs targeting EVs ([S1]). This platform addresses specific thermal challenges related to pouch and prismatic battery cells creating a distinctive value proposition supporting some switching costs for customers.

However, the company faces competition from established Chinese suppliers offering lower-cost materials and patent protections whose validity has been challenged abroad. Several key Korean patents were invalidated between 2023–2024 with appeals pending as of early 2026 ([S1]). These developments erode barriers to entry for competitors using similar technologies.

The aerogel R&D cycle involves lengthy qualification phases extending multiple quarters; Aspen must sustain innovation while reducing time-to-market to capitalize on evolving EV designs.

Market Focus on EV Battery Thermal Management: Opportunities and Risks

Aspen’s strategic focus on EV battery manufacturers reflects anticipated growth linked to automotive electrification trends ([N1], [S1], [S6]). Its technology compatibility with pouch and prismatic cell formats is relevant for key OEM battery architectures but also increases exposure to evolving battery chemistries requiring product adaptations.

Customer contracts typically lack minimum purchase volume guarantees and are often based on purchase orders rather than binding long-term agreements ([S21]). This structure creates revenue volatility tied to manufacturer production schedules.

Extended qualification cycles delay revenue recognition while intensifying upfront R&D expenses—common industry challenges compounded by Aspen's concentrated client base.

Quarterly Momentum and What To Monitor Next

The Q4 2025 earnings report highlighted positive operating cash flows alongside reduced revenues compared to prior periods ([N1], [S3]). Sustained positive cash generation may indicate operational improvements or cost controls despite softening top line.

EBITDA trends warrant attention given their role as covenant triggers under debt agreements ([S24]). Liquidity metrics also require scrutiny amid covenant amendments easing liquidity ratios but signaling compliance risks if revenues remain weak ([S4], [S24]).

Monitoring order patterns from GM—the largest customer representing a sizable share of sales—is critical due to high revenue concentration risk ([S21]). Any demand shifts could materially affect near-term results.

Analysis of Capital Allocation: Debt, Cash Flow, and Returns Dynamics

Aspen amended its MidCap Loan Facility multiple times in 2025 to relax liquidity thresholds (now linked more closely to term loan principal) while removing minimum EBITDA covenants ([S4], [S5]). These changes reflect lender accommodations amid revenue declines but highlight financing fragility.

Capital expenditures declined sharply by over half year-over-year between FY2024 and FY2025 while operating cash flow contracted by about 28% though remaining positive ([F1]).

An approximate return on equity calculation based on net losses relative to equity indicates a steeply negative ROE near -165%, signaling structural challenges converting shareholder capital into profits currently ([F1]).

Cash reserves above $150 million at year-end provide liquidity buffer but persistent net losses result in slightly negative free cash flow after capex (~-$4.6 million), emphasizing careful capital management is necessary ([F1]).

Customer Concentration and Contractual Risks Affecting Stability

Sales are highly concentrated: General Motors accounted for approximately 59% of total revenues in FY2025 with distributors comprising another significant portion (~9%) ([S21]). While concentration streamlines relationships it elevates risk if major customers reduce orders or renegotiate pricing.

Contracts generally lack minimum volume commitments; distributor sales proceed mostly on purchase order basis increasing revenue unpredictability ([S21]). Pricing pressures add further uncertainty amid macroeconomic headwinds or raw material cost shifts.

Downstream dependencies also complicate visibility since direct customers concentrate sales among few end-users.

Supply Chain Strategies Amid Geopolitical and Manufacturing Dependencies

Aspen operates a primary manufacturing plant in East Providence, Rhode Island plus third-party external manufacturing partners mainly in China ([S1]). This dual approach offers capacity flexibility but introduces operational risks including quality control challenges and geopolitical tensions impacting supply continuity.

Reliance on three production lines at the East Providence facility heightens vulnerability to disruptions ([S1]). Robust contingency planning alongside partner compliance reviews is essential given complex US-China trade dynamics.

Navigating Patent Litigation as Barrier or Risk Factor

Since April 2023 Aspen filed patent infringement complaints against Korean entities alleging violations of aerogel patents. Initial investigations favored Aspen but subsequent rulings invalidated key composition patents with appeals pending before Korean IP High Court as of early 2026 ([S1]).

These outcomes weaken Aspen’s regional enforcement power potentially allowing competitors to use similar technologies without effective legal challenge. For a company relying heavily on proprietary formulations as moat components this poses medium- to long-term sustainability risks.

This analysis integrates financial data from SEC filings and public disclosures highlighting Aspen Aerogels’ position balancing innovation-driven positive operating cash flows against ongoing operational losses fueled by heavy R&D spending and market challenges. Investors should monitor developments around OEM contract renewals including GM exposure, debt covenant compliance amid revenue pressures beyond FY2025 data points, patent litigation outcomes affecting IP protections especially in Asia; alongside supply chain resilience under geopolitical complexity impacting overseas manufacturing.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments