Perceptive Capital Solutions' Transition Hinges on Freenome Deal and Trust Account Utilization

A blank check company focusing on healthcare targets approaches a critical milestone with an impending business combination.

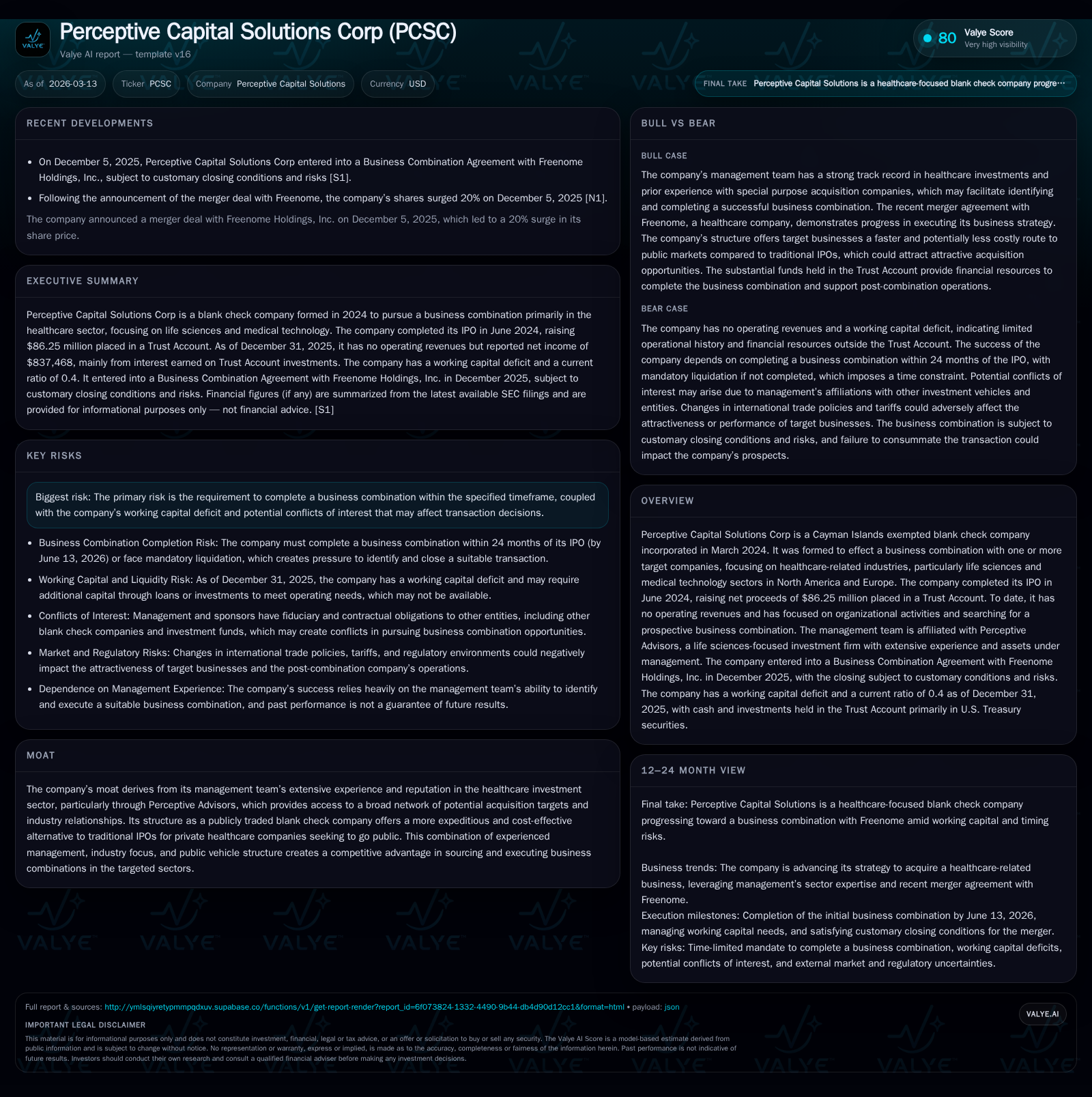

Perceptive Capital Solutions Corp, a Cayman Islands-based blank check company established in 2024, has raised approximately $86 million through its IPO to pursue a business combination in healthcare. Its management’s pedigree from Perceptive Advisors grants it access to specialized industry networks, targeting life sciences and medical technology firms primarily in North America and Europe. The company is currently positioned to complete its initial business combination with Freenome Holdings, with the closing expected in the first half of 2026, subject to approvals. While it reports no operational revenues and carries a working capital deficit, the bulk of its funds remain secured in a trust account, earmarked for the acquisition and subsequent growth initiatives.

Company Overview and Historical Performance

Perceptive Capital Solutions Corp is a recently formed blank check (SPAC) entity incorporated on March 22, 2024, under Cayman Islands jurisdiction [S1]. It was established specifically to identify and effectuate a business combination within healthcare-related industries, with acute focus on North American and European life sciences and medical technology companies [S1]. Leveraging the expertise of Perceptive Advisors — an investment firm centered on healthcare with over $9.5 billion assets under management as of December 31, 2025 —the company benefits from an experienced management team well-versed in sourcing innovative healthcare investments [S1].

The company completed its IPO on June 13, 2024, issuing approximately 8.6 million Class A ordinary shares at $10 each, including full exercise of an over-allotment option plus a private placement with sponsors for $2.86 million [S1][S21]. The net proceeds totaled roughly $86.25 million and were placed into a Trust Account invested primarily in short-term U.S. Treasury securities [S4][S9]. To date, Perceptive Capital Solutions has generated no operating revenues as it remains focused on preparing for its initial business combination; expenditures reported are connected to administrative costs related to this pursuit [F1][S6].

Financially, the company recorded an operating loss worsening from $494k in fiscal year (FY) 2024 to nearly $3 million in FY2025, marking a sharp increase (-503% YoY) attributable primarily to organizational growth and transaction preparation expenses [F1]. Despite this operating loss, net income reported was positive at approximately $837k for FY2025 compared to roughly $1.9 million in FY2024 (-56% YoY), driven by interest income earned on assets held in the Trust Account [F1][S6]. Operating cash flow reflected negative trends consistent with operating losses: -$864k (FY2025) versus -$353k (FY2024) [F1]. The firm carried a negative shareholders’ equity position of about -$4.8 million by end-2025 versus -$2.1 million at end-2024 [F1]. The current ratio stood at around 0.40 due to current liabilities exceeding current assets ($2.25 million liabilities vs. $907k assets as of December 31, 2025), underscoring the need for capital influx beyond the Trust Account for ongoing operations [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 837468 | -864653 | -3 | -56.2% |

| 2024 | 1910392 | -353623 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -17.5 |

| 2024 | -90.3 |

Source: SEC companyfacts cache [F1].

Table shows lack of revenue but increasing administrative costs leading to wider operating losses alongside positive net income reflecting non-operating income sources.

Future Growth Prospects and Business Combination Milestones

Perceptive Capital Solutions’ primary growth driver hinges on successful execution of its initial business combination (IBC). As disclosed in December 2025 filings, the company entered into an agreement to merge with Freenome Holdings Inc., a life sciences firm specializing likely in leveraging multi-omics for early cancer detection technologies [S1]. This deal—subject to customary closing conditions including stockholder approvals—is anticipated to conclude within the first half of calendar year 2026 [S1]. Upon closing:

- The SPAC will domesticate from Cayman Islands to Delaware jurisdiction;

- It will rename to "Freenome Inc." reflecting continuation under Freenome's corporate structure;

- Various equity conversions will occur converting Class B shares into Class A common stock at defined exchange ratios calculated on implied equity values near $725 million [S1].

This transition marks Perceptive Capital Solutions’ ultimate step from a shell vehicle into an operating public company within a vibrant sector benefiting from secular trends such as aging populations and expanding precision medicine applications.

Nonetheless, several constraints could limit growth or affect transaction success:

- Time sensitivity: The SPAC is bound by its initial charter requiring consummation of IBC by June 13, 2026 — failure results in mandatory liquidation [S8][S15];

- Working capital limitations outside Trust Account pose operational funding risks prior to completion [S9][F1];

- Potential conflicts between sponsor interests and public shareholders could influence transaction terms or approval outcomes [S1];

- Macroeconomic and geopolitical factors such as shifting international trade policies or tariffs could indirectly affect target valuations or post-combination performance given cross-border operations prevalent among life sciences entities [S2].

Financial Forecasts and What To Watch

While explicit forward guidance is unavailable given the blank check structure pending deal closure, key variables will be observable around:

- Shareholder approval votes for the business combination;

- Redemption elections impacting cash availability;

- Completion timing relative to statutory deadlines;

- Post-merger pro forma capitalization changes issued via subsequent SEC filings.

Analysts should monitor forthcoming proxy materials detailing redemption rights distribution methodology which will materially influence cash flows available post-merger for operational scaling or further acquisitions.

Returns and Capital Allocation Dynamics

Classical return metrics such as ROE are challenging given absence of operating revenue and current negative equity balance standing near -$4.8 million against net income generation driven largely by passive income streams from Trust Account investments rather than active operations [F1]. The approximate trailing ROE calculated by dividing net income by negative equity yields around -17%, reflective more so of accounting structure than operational efficiency.

Capital allocation focuses on deploying IPO proceeds securely: funds reside predominantly invested in short-dated U.S. Treasury Bills managed under strict Trust Agreement constraints ensuring principal protection until business combination consummation or liquidation events [S4][S9]. Interest accrued (~$3.8 million FY2025) supplements working capital but withdrawals are limited annually (max ~$300k) aside from tax payments [S9].

Management has no declared dividends or share repurchase programs pending deal closure given constrained capital deployment options inherent to blank check vehicles but anticipates flexible consideration mix involving cash, debt or equity instruments for the combination itself allowing negotiation agility depending on target preferences [S26]. Sponsor-backed working capital loans up to $3 million are convertible into post-combination shares if required; executed loans provide temporary relief for operational expenses prior to closing but imply dilution risk downstream if converted [S9][S15].

Competitive Moat and Risks Summary

The competitive advantage of Perceptive Capital Solutions springs chiefly from its leadership’s deep immunology/biotech investing knowledge base coupled with Perceptive Advisors’ robust ecosystem encompassing venture capital firms, public investors specialized in biotech/life sciences sectors and healthcare executives across relevant geographies [S6]. This network enhances deal sourcing pipelines often inaccessible to typical SPACs lacking domain expertise.

Risks remain material due to:

- Deadline-driven liquidation threat imposing pressure on deal valuation discipline;

- Economic volatility affecting fundraising conditions post-merger;

- Potential misalignment between sponsor incentives and minority public shareholders especially concerning redemption mechanics or control post-closing;

- Trade policy uncertainties that can distort underlying target fundamentals unexpectedly despite historical financials appearing stable under different tariff regimes [S2].

Summary

Perceptive Capital Solutions represents a classic healthcare-focused SPAC archetype backed by an experienced sponsor group targeting life science innovation drivers through public market access facilitation strategies increasingly sought after by private biotechs amid tightening IPO windows. Its transition away from a shell entity hinges critically on successful closure of its Freenome transaction during H1 2026 when it will shed its blank check status and aim at growing operational scale leveraging accumulated capital resources prudently locked inside trust arrangements until consummation.

The company’s financials reflect typical pre-business combination stage characteristics — no operating revenues yet elevated administrative costs — backed by strong trust account liquidity but limited non-trust working capital necessitating sponsor support if delays occur.

Going forward monitoring shareholder approvals alongside redemption levels will provide clear visibility into execution risk while watching broader macroeconomic factors influencing healthcare innovation markets remains prudent.

Disclaimer: This analysis is intended solely for informational purposes based strictly on publicly available documents without any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments