Colony Bankcorp Expands Loan Portfolio and Capital Base with TC Bancshares Acquisition

Acquisition accelerates real estate lending growth and strengthens capital and liquidity positions in key Southeastern markets.

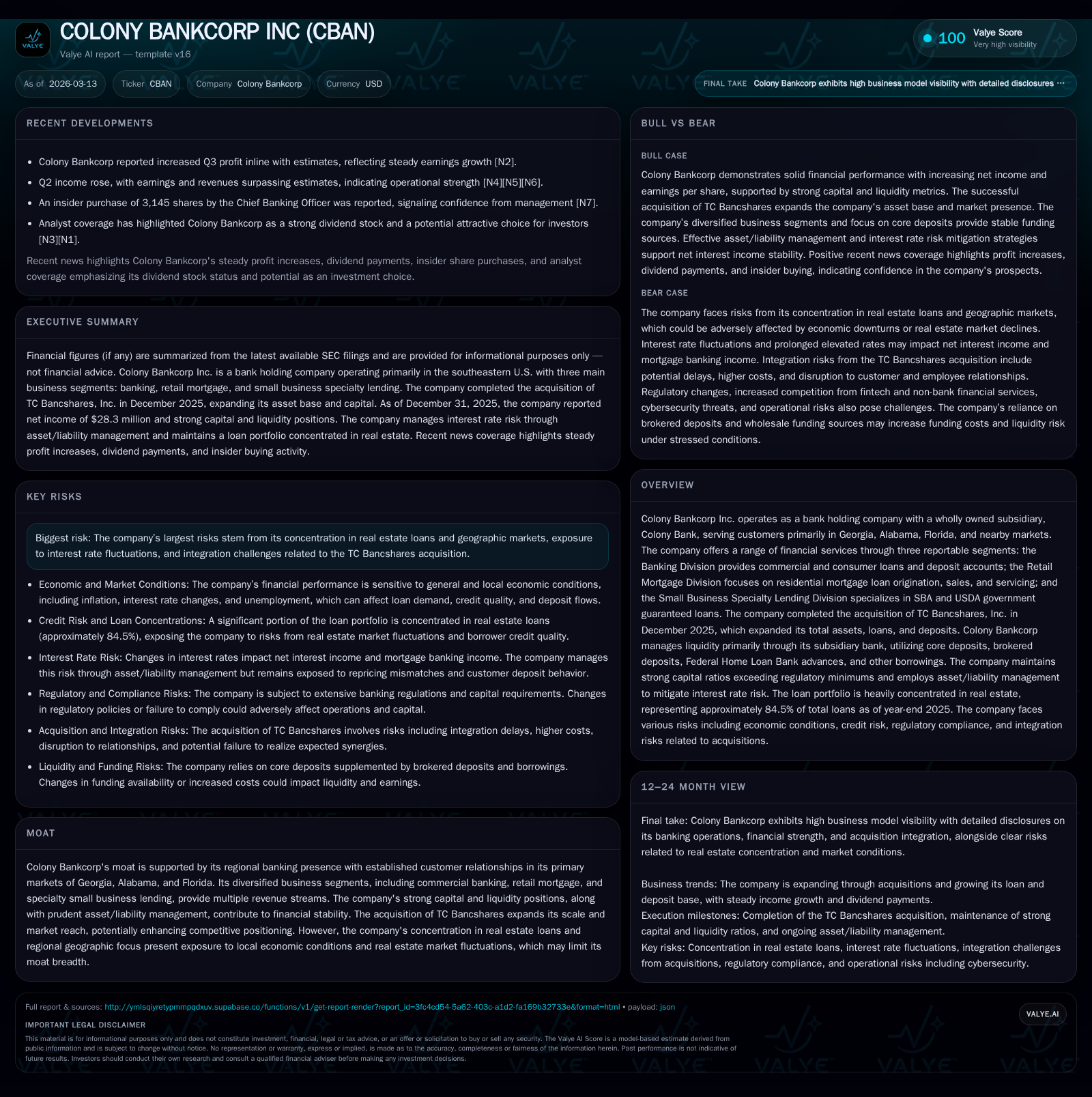

Colony Bankcorp Inc. reported an 18.4% increase in net income for fiscal year 2025, driven by organic growth and the acquisition of TC Bancshares, Inc. The acquisition bolstered loan balances—especially in commercial real estate—and equity capital, enhancing the company’s regional presence across Georgia, Alabama, and Florida. Real estate loans represented 84.5% of total loans at year-end 2025. Strong capital ratios and diversified funding sources support liquidity and regulatory compliance. Management prioritizes core deposit growth and prudent risk management amid exposure to regional real estate cycles and integration risks.

Company Overview and Recent Developments

Colony Bankcorp Inc., a bank holding company operating principally in Georgia, Alabama, and Florida, completed the acquisition of TC Bancshares, Inc. in December 2025 [S1]. This transaction expanded Colony's asset base, deposits, and loan portfolio significantly, enhancing its regional footprint particularly in commercial real estate lending sectors. The company operates through its subsidiary Colony Bank which provides commercial loans, consumer financing, residential mortgage products, and specialized small business lending including SBA/USDA guaranteed loans [S1][S22].

The acquisition added approximately $65.9 million in common stock equity alongside substantial growth in lending assets—construction, land development loans increased by 47.5% to $302.5 million while other commercial real estate loans rose by 26.2% to $1.25 billion as of December 31, 2025 [S1][S14]. This supports a diversified revenue base but maintains a high concentration in real estate collateral representing approximately 84.5% of total loans [S10].

Historical Growth and Financial Performance

From fiscal years 2022 through 2025, Colony steadily increased net income from $19.54 million to $28.25 million reflecting an 18.4% year-over-year increase driven by disciplined loan growth and operational efficiencies enhanced by the acquisition.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 28 | -6 | 1 | +18.4% |

| 2024 | 24 | 23 | 1 | +9.8% |

| 2023 | 22 | 21 | 4 | +11.3% |

| 2022 | 20 | 50 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 8 | 2 | -7 |

| 2024 | 8 | 1 | 22 |

| 2023 | 8 | 0 | 17 |

| 2022 | 7 | 1 | 47 |

Source: SEC companyfacts cache [F1].

Operating cash flow was negative in FY2025 (-$5.55 million), likely reflecting increased loan originations following the acquisition despite solid net income performance [F1]. Capital expenditures remained modest relative to asset growth.

Loan Portfolio Composition and Credit Risk

Colony’s loan portfolio is concentrated primarily in real estate-related lending with construction & land development loans totaling $302 million and other commercial real estate loans at nearly $1.25 billion by end-2025 [S1]. The underwriting process emphasizes collateral-backed lending consistent with internal credit policies.

Non-owner occupied commercial real estate exposures are diversified across multifamily housing ($106 million), hotel/motel ($101 million), retail ($183 million), office space ($138 million), industrial/warehouse (~$74 million), among others [S1]. Residential real estate loans increased by over one-third to approximately $459 million due to organic growth and acquisition contributions.

Consumer lending also grew substantially supported by marine/RV financing as well as unsecured technology-driven Upstart loans targeting borrowers with limited or no credit history [S1].

Management identifies concentration risk mainly within the "Lessors of Non-Residential Real Estate" industry group exceeding a tenth of total loans, necessitating ongoing monitoring amid regional economic cyclicality [S10].

Capital Structure and Liquidity Position

Shareholders’ equity expanded materially to $375.9 million at December 31, 2025 due to the issuance of common stock related to the TC Bancshares acquisition plus net income accumulation less dividends paid [$8 million] [F1][S14]. Regulatory capital ratios are robust with Tier 1 ratio at 13.60% and common equity Tier 1 ratio at 12.67%, comfortably exceeding regulatory minimums; Tier 1 leverage ratio stood at 10.78% versus a required standard of 4% [S14][S16].

Liquidity is supported by a stable core deposit base supplemented by brokered deposits amounting to approximately $132 million or about 4% of total deposits as of year-end 2025 [S16][S17]. Federal Home Loan Bank advances totaled $195 million with additional borrowing capacity of nearly $747 million based on pledged collateral values providing ample contingency funding options [S15][S16][S21][S23].

The investment securities portfolio totaled approximately $383.8 million offering liquid assets that can be sold or pledged for borrowings if needed—enhancing financial flexibility against liquidity demands [S15]. Management employs active asset-liability management strategies balancing liquidity needs against earnings potential.

Business Segment Strategy

Colony operates three primary business segments:

- Banking Division: Commercial and consumer loans alongside deposit services targeting regional businesses and individuals.

- Retail Mortgage Division: Residential mortgage origination and servicing generating fee income linked partly to refinancing activity.

- Small Business Specialty Lending Division: SBA/USDA government-guaranteed loans serving niche small business markets seeking lower risk financing options. Each segment functions under unified governance enabling tailored credit risk assessments while leveraging shared service platforms for efficiency gains [S22].

Growth Outlook Considerations

Growth is expected from ongoing demand for commercial real estate financing fueled by development projects; expansion within specialty government-backed small business lending; consumer lending innovations including digital underwriting platforms; along with continued deposit base expansion through strengthened customer relationships.

Challenges include competitive pressures on deposit pricing potentially increasing funding costs; interest rate volatility impacting margins; integration risks associated with recent acquisitions; plus geographic concentration risks tied to Southeastern U.S real estate market conditions [N1][S2][S10].

Regulatory oversight remains critical especially regarding capital adequacy requirements alongside evolving cybersecurity risk management frameworks detailed in governance disclosures highlighting Board-level Technology Committee engagement [S1].

Capital Allocation Policy & Returns

The Company maintains a consistent dividend distribution near $8 million annually aligned with earnings supporting retained earnings for organic growth and acquisitions funding [F1][S14]. Share repurchases increased moderately to $2.37 million indicating incremental capital returned beyond dividends while preserving balance sheet strength.

Return on equity approximates a moderate level near 7.5% for FY2025 calculated using net income over average equity demonstrating solid profitability considering industry conditions and investments made for growth initiatives [F1].

Conclusion

Colony Bankcorp’s acquisition of TC Bancshares has significantly expanded its franchise size and market penetration across key Southeastern U.S regions while reinforcing focus on real estate lending—a sector that requires careful management given its cyclical nature. Robust capital levels combined with diversified liquidity sources provide resilience accommodating future loan demand amid macroeconomic uncertainties including interest rate fluctuations. Management’s balanced approach towards risk-weighted asset growth alongside disciplined capital returns underpins sustainable long-term value creation within its regional banking niche. Despite inherent risks from concentration exposures and integration complexities, focused governance on credit quality assessment, cybersecurity oversight, and regulatory compliance supports institutional robustness going forward.

This summary reflects publicly available information as of March 13, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments