ProFrac Holding Corp. Faces Steep Losses Amid Industry Headwinds and Cost Pressures

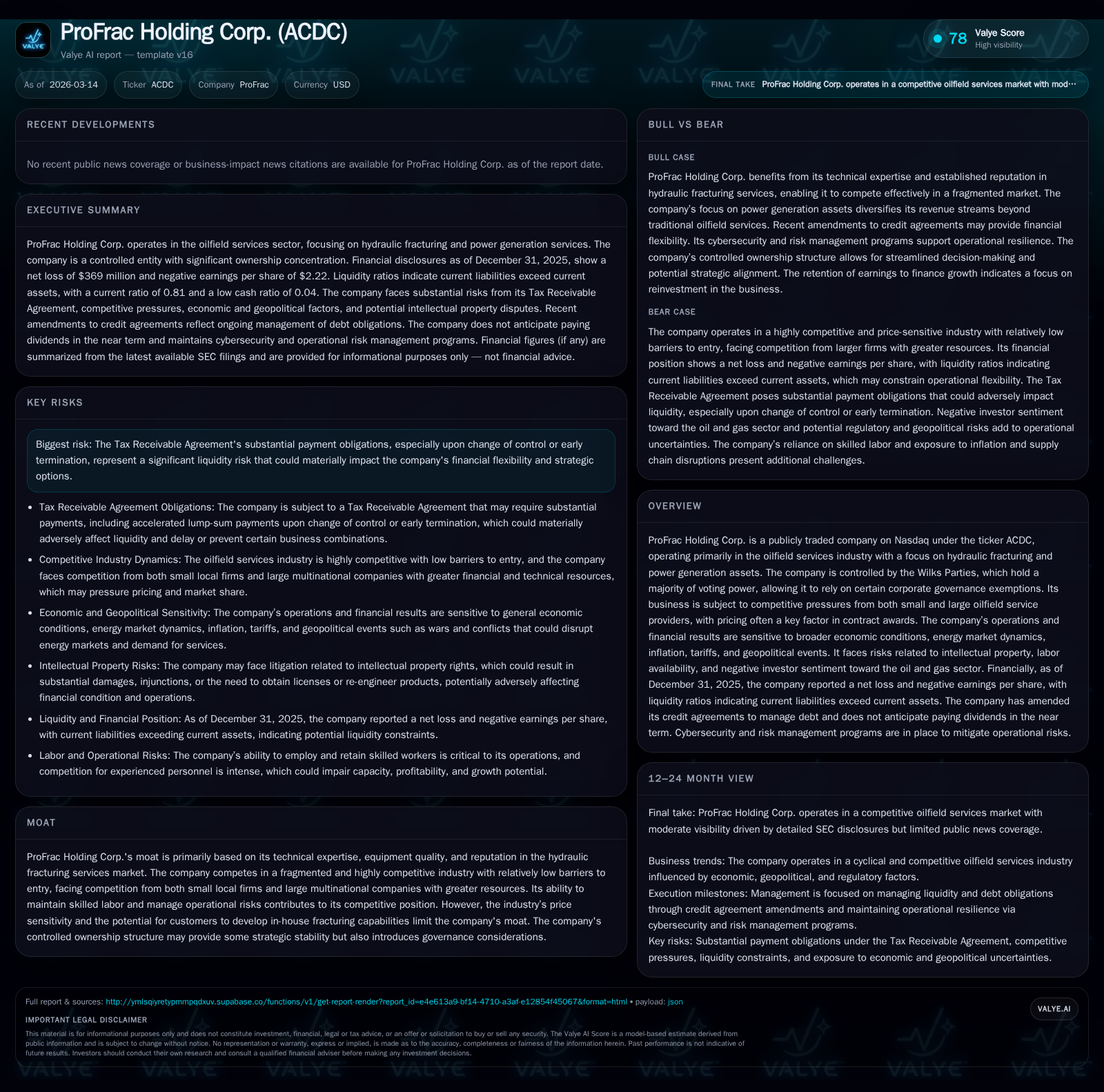

Despite historical profitability, ProFrac reported significant financial losses in 2025, reflecting intensifying competitive and operational challenges within the hydraulic fracturing sector.

ProFrac Holding Corp. recorded a sharp decline in operating income and net income for FY2025, driven by heightened price competition, labor shortages, and increased costs. Operating cash flow remained positive but contracted notably, while capital expenditures were reduced amid tighter financial conditions. The company's liquidity is further constrained by substantial obligations under a Tax Receivable Agreement, which could accelerate with changes in control. ProFrac operates in a fragmented market with both small local and large multinational competitors, facing pressures from customer insourcing and regulatory complexities. Management prioritizes operational efficiency and capital discipline as key factors for near-term recovery.

Financial Performance Overview

ProFrac Holding Corp.'s financial results for fiscal years 2022 through 2025 illustrate significant volatility and deterioration in profitability. Operating income declined from positive $125 million in FY2022 and $167 million in FY2023 to negative $60 million in FY2024 and further down to a loss of $226 million in FY2025, representing a nearly 274% year-over-year decrease in the latest period [F1].

Net income followed a similar trajectory, swinging from a profit of $41 million in 2022 to losses of $98 million in 2023, deepening to losses of $215 million in 2024, and reaching negative $369 million by the end of 2025 [F1].

Operating cash flow (CFO) peaked at $415 million in 2022 but then fell sharply to just $4.3 million in 2023 before rebounding to $367 million in 2024 and declining again to approximately $189.5 million at the end of FY2025 [F1]. Despite losses on an accounting basis, positive cash flow reflects effective working capital management.

Capital expenditures have been reduced from $356 million in 2022 to approximately $170 million in FY2025, highlighting management's focus on controlling investment during periods of financial stress [F1]. Equity contracted from over $1.2 billion at the end of 2023 to roughly $718 million at the close of FY2025 due to cumulative losses eroding shareholder value [F1]. The approximate return on equity for FY2025 is -51%, illustrating ongoing challenges generating returns relative to invested capital [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -369 | 190 | -226 | 170 | -71.5% |

| 2024 | -215 | 367 | -60 | 255 | -120.2% |

| 2023 | -98 | 4 | 167 | 267 | -338.9% |

| 2022 | 41 | 415 | 125 | 356 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 20 | -51.4 |

| 2024 | 112 | -21.4 |

| 2023 | -263 | -8.1 |

| 2022 | 59 | -3.5 |

Source: SEC companyfacts cache [F1].

Note: Negative equity reported for fiscal year ended December '22 likely reflects accounting reclassifications or acquisition effects; subsequent years denote recovery.

Industry Positioning and Competitive Landscape

ProFrac operates primarily within the hydraulic fracturing services sector, which is characterized by fragmentation and intense price competition [S4]. The company's competitive advantages include technical expertise, quality equipment, experienced personnel, and a reputation for safety and reliability.

Competition arises from numerous small regional firms as well as large multinational oilfield service companies possessing broader resources and diversified service offerings allowing aggressive pricing strategies through bundled services or below-market bids [S4][S19]. Contract awards are often bid-based where price plays a dominant role.

Additionally, customers increasingly internalize fracturing operations by deploying their own equipment and crews rather than outsourcing these services—a trend that reduces addressable market demand for independent providers like ProFrac [S19]. Labor shortages further constrain capacity expansion given high demand for skilled fracturing crews across the industry [S12].

Operational Factors Influencing FY2025 Results

The company’s recent earnings report cited rising labor costs driven by workforce scarcity alongside inflationary pressures on materials as significant contributors to margin compression during FY2025 [N1][N2]. Moreover, lower utilization rates on frac sand assets following market downturns resulted in operational inefficiencies affecting cost structures [S9].

While diversification into power generation services targeting data centers and utilities has provided incremental revenue streams, these remain nascent and insufficient to offset pressure within core fracturing operations fully [S11].

Pricing Dynamics and Market Risks

Price competition remains central within ProFrac’s markets where contract awards are frequently determined via bidding processes emphasizing cost competitiveness [S11][S28]. This environment forces downward pressure on service rates while input costs rise.

Furthermore, increasing customer insourcing of fracturing services erodes volumes available for third-party contractors like ProFrac [S19], necessitating strategic adjustments.

Regulatory complexities across geographies contribute additional compliance costs that may affect operational flexibility relative to larger competitors with more extensive geographic footprints able to balance risks across markets [S11][S28].

Capital Allocation and Liquidity Considerations

ProFrac’s liquidity position is influenced notably by obligations under its Tax Receivable Agreement (TRA), which requires substantial payments potentially accelerating upon ownership changes or early termination events—posing material liquidity risks that could affect strategic flexibility [S1][S9][S21][S25]. Estimates indicated potential accelerated payments up to approximately $86 million if triggered abruptly as of December ’25.

Despite operating losses, positive operating cash flow ($190 million) against reduced capital expenditures ($170 million) generated modest free cash flow (~$20 million), supporting cautious reinvestment amid financial constraints [F1].

No dividends have been declared or paid recently; share repurchases were absent during the latest reporting period consistent with preserving liquidity amid earnings challenges [S10][F1]. Current ratio stands below one at approximately 0.81 indicating near-term liquidity pressure given current liabilities exceed current assets slightly [F1].

Broader Risks: Litigation, ESG Factors, and Cybersecurity

Legal risks include ongoing litigation related to supply contract disputes arising from acquisitions with potential adverse financial implications should outcomes be unfavorable [S5][S6], as well as potential intellectual property disputes given competitive pressures around proprietary technologies used within service lines [S7].

Environmental, Social & Governance (ESG) considerations increasingly influence investor sentiment towards fossil fuel-related industries including oilfield services. Disinvestment trends based on ESG concerns may impact capital access costs while regulatory scrutiny adds compliance burdens affecting operations negatively [S8][S24].

Cybersecurity remains an area of focus with dedicated governance programs mitigating risk though evolving threats pose continuing challenges capable of disrupting operations if incidents occur [S16][S20][S28].

Outlook and Strategic Focus

While explicit forward guidance post-FY25 is not provided publicly, key metrics such as contract pricing trends, frac sand market conditions influencing asset utilization, outcomes of pending litigation matters, and timing of TRA payments will critically shape near-term performance.

Management’s emphasis appears centered on operational efficiency improvements alongside disciplined capital allocation aimed at stabilizing margins amid competitive pressures documented during recent earnings calls [N2]. Monitoring peer developments offers comparative insight into sector dynamics affecting ProFrac’s outlook [N3].

Controlled governance structure under majority ownership affords some strategic stability but concentrates execution accountability which stakeholders should monitor closely.

This analysis incorporates data solely from public filings and disclosures through March 14, 2026 without making investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments