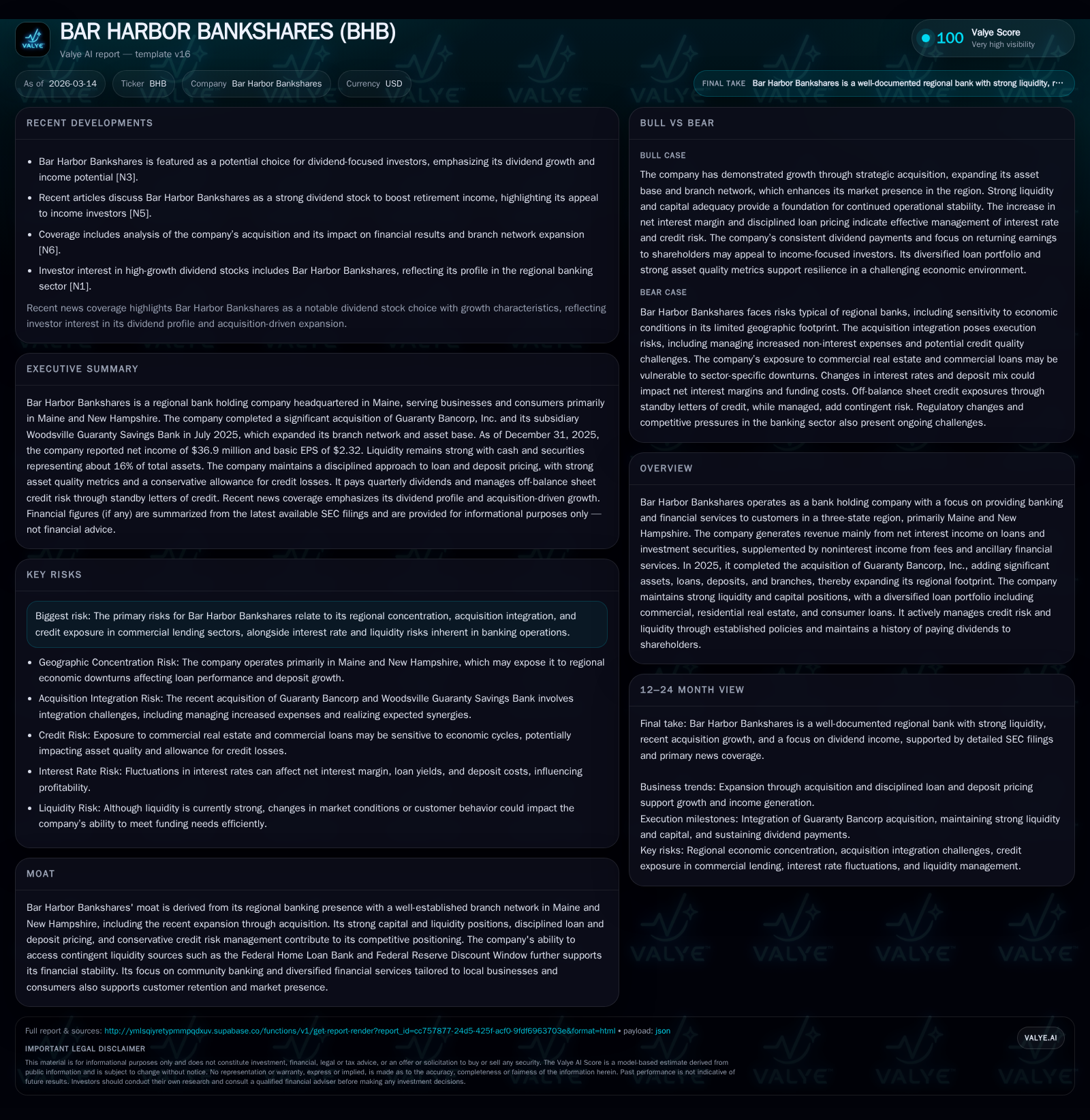

Bar Harbor Bankshares' Acquisition-Fueled Growth Underpinned by Regional Strength

Following its transformative 2025 acquisition, Bar Harbor Bankshares leverages regional focus and disciplined banking to drive growth while managing credit and liquidity risks.

Bar Harbor Bankshares significantly expanded its scale and regional presence in mid-2025 through acquiring Guaranty Bancorp, integrating $658 million in assets and nine new branches primarily across Maine and New Hampshire. Despite this growth, 2025 net income declined 15.2% year-over-year due to acquisition-related expenses and credit impairments, balanced by robust dividend increases and solid capital positioning. The company’s conservative loan pricing discipline, supplemented by diversified credit exposure and strong access to contingent liquidity sources like the Federal Home Loan Bank, underpins its resilient operating model. Looking forward, execution of acquisition integration and sensitivity to interest rate shifts remain key considerations for sustaining earnings growth.

Historic Financial Performance Through FY2025

Bar Harbor Bankshares (BHB) demonstrated stable financial results over recent years with a notable strategic expansion in mid-2025. Net income declined from $43.5 million in FY2024 to $36.9 million in FY2025, a 15.2% decrease primarily due to acquisition-related expenses and credit impairments affecting securities portfolios [F1][S1][S7]. Operating cash flow decreased by approximately 7.8% year-over-year to $48.3 million while capital expenditures fell by about 35%, reflecting cautious investment amid integration efforts [F1].

Shareholders' equity grew significantly by around 16%, reaching $532.5 million at FY2025 year-end, driven by retained earnings accumulation and capital impacts from the Guaranty Bancorp acquisition completed in July 2025 [F1][S1]. Dividends paid also rose steadily from $15.3 million in FY2022 to over $20 million in FY2025, underscoring a commitment to shareholder returns despite earnings headwinds [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 37 | 48 | 5 | -15.2% |

| 2024 | 44 | 52 | 7 | -2.9% |

| 2023 | 45 | 47 | 7 | +3.0% |

| 2022 | 44 | 58 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 20 | 43 | 6.9 |

| 2024 | 18 | 45 | 9.5 |

| 2023 | 17 | 41 | 10.4 |

| 2022 | 15 | 55 | 11.1 |

Source: SEC companyfacts cache [F1].

Table illustrates recent fiscal performance highlighting net income contraction in the latest year despite equity growth.

Acquisition of Guaranty Bancorp Expands Regional Scale

The July 31, 2025 acquisition of Guaranty Bancorp added approximately $658 million in total assets including $413 million in loans across commercial, residential real estate, and consumer segments, alongside liabilities dominated by deposits exceeding $531 million [S2]. This transaction expanded BHB's branch network by nine locations primarily across New Hampshire, increasing its footprint to over sixty branches regionally as of September quarter-end [S2][S3].

Purchase accounting recognized goodwill of about $22.3 million and core deposit intangibles near $14 million reflecting anticipated benefits from customer relationships and market expansion acquired [S2]. Third-quarter results post-acquisition showed increased average balances with revenue gains tempered by integration costs such as conversion expenses approximating $1.2 million during the transition [S2][S7]. The enlarged deposit base supports enhanced funding flexibility complementing wholesale borrowing capacity.

Regional Banking Model: Diversification and Discipline

BHB’s competitive advantage lies in its focused regional community banking approach centered on Maine with growing presence in New Hampshire [S2]. The bank employs disciplined loan pricing balancing yield with risk tolerance across a diversified loan portfolio including commercial loans (industrial and commercial real estate) and consumer mortgage products.

This prudent credit strategy reduces concentration risks typical among regional lenders exposed to cyclical local industries or concentrated borrower groups . Complementary financial services tied to loans and deposits such as treasury management and wealth advisory generate stable noninterest income streams that enhance customer retention and financial resilience [S2].

Credit Quality and Liquidity Management Amid Growth

Credit metrics remained robust through expansion phases: nonperforming assets were contained at approximately 0.25% of total assets as of September 30, 2025 with net charge-offs totaling roughly $316 thousand illustrating effective loss mitigation despite challenging conditions [S2][S5]. However, impairments on certain corporate debt securities related to fraudulent borrower activity led to write-downs totaling around $4.9 million during H1-2025 reflecting active risk management [S6][S7].

Liquidity is well maintained with nearly $1 billion of same-day available resources including cash reserves plus unutilized borrowing capacity at the Federal Home Loan Bank and Federal Reserve facilities alongside committed lines of credit providing contingency buffers against seasonal or economic fluctuations [S4][S5]. The bank’s Asset-Liability Management Policy enforces liquidity thresholds around eight percent of total assets ensuring funding stability.

Capital Allocation Priorities: Equity Growth and Dividends

Equity strengthened markedly post-acquisition with shareholders' equity rising over $74 million above FY2024 levels reaching approximately $532 million at FY25 close; regulatory capital ratios confirm strong capitalization per banking standards [F1][S4][S5]. Return on equity for FY25 approximated a moderate but stable figure near 6.9%, influenced by acquisition-related charges but offering scope for improvement as integration progresses fully [F1].

Dividend payments increased steadily over recent years up to more than $20 million annually indicating sustained shareholder return focus; however, no share repurchases have been conducted since before FY2020 signaling preference for liquidity preservation amid growth investments currently [F1].

Operating cash flow reductions align with lower net income but free cash flow remains positive after capex outlays supporting dividends without external capital raises observed during reporting periods.

Milestones Ahead: Integration Execution & Market Sensitivities

Key milestones include monitoring merger synergy realization via quarterly earnings updates tracking efficiency gains versus integration expenses ([N3],[S3]). Observing loan portfolio segmentation shifts will reveal organic originations relative to acquired book changes impacting credit quality especially within commercial real estate concentrations.

Dividend declarations will reflect Board discretion balancing payout sustainability against reinvestment demands ([S4]). Branch network optimization efforts may lead to consolidation or technology enhancements improving service efficiency after scale expansion.

Liquidity position scrutiny focusing on same-day access ratios inclusive of FHLB/Fed borrowings usage will signal stress or strength conditions ([S4],[S5]). Successfully navigating interest rate volatility will be crucial given potential margin pressures from repricing mismatches between variable- and fixed-rate loan products alongside deposit cost dynamics impacting net interest margins (,[N3],[S2]).

Risks remain tied to regional economic cycles influencing borrower creditworthiness though diversified loan composition partly cushions sectoral exposures. Future regulatory or monetary policy changes could alter credit costs or funding environment requiring adaptive risk management.

This analysis is provided solely for informational purposes without investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments