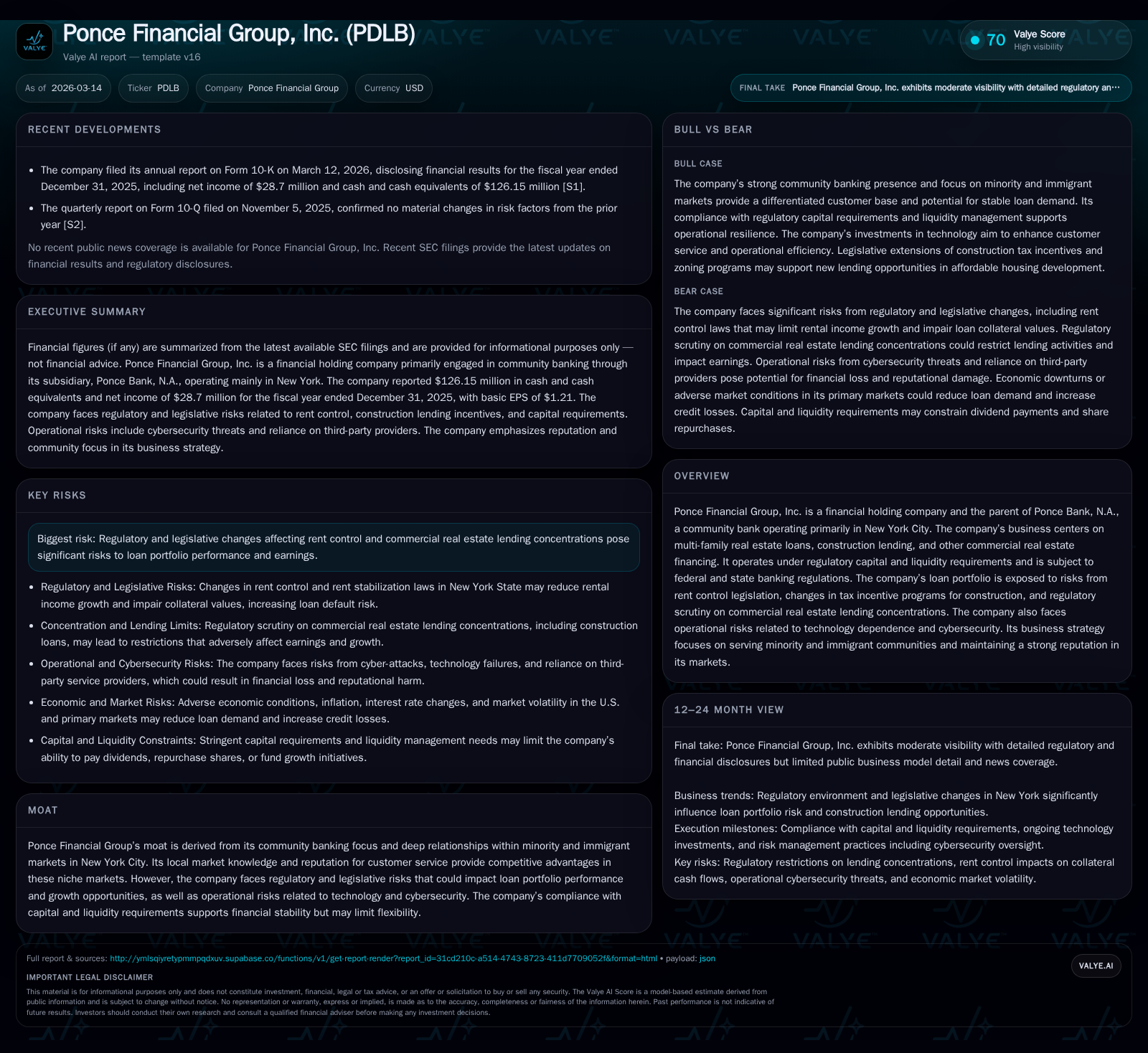

Ponce Financial Group’s Growth Fueled by Community Focus and Commercial Real Estate, Counterbalanced by Regulatory and Liquidity Constraints

Ponce Financial Group capitalizes on niche multi-family real estate financing in NYC but faces heightened regulatory, operational, and market risks that will shape its trajectory.

Ponce Financial Group, Inc. operates primarily as a community bank in New York City, concentrating on multi-family and commercial real estate lending, underpinned by deep ties to minority and immigrant communities. After recovering from losses in 2022 and minimal income in 2023, the company posted strong profitability gains through 2025, driven by loan portfolio growth and enhanced operating cash flow. Despite this progress, its business is exposed to legislative challenges affecting rent control policies and tax incentive programs, as well as liquidity management pressures amidst a volatile funding environment. Capital requirements are met but limit flexibility around dividends and share buybacks. The company invests steadily in technology and risk controls to address cybersecurity and operational risks. Going forward, its ability to sustain growth hinges on adapting to evolving local regulatory landscapes while maintaining community trust and capital discipline.

Company Overview

Ponce Financial Group, Inc. is a financial holding company headquartered in the Bronx serving predominantly New York City markets through its subsidiary Ponce Bank, N.A. The company’s core business centers on lending for multi-family residential properties, construction projects, and various commercial real estate transactions. This niche focus roots the firm's competitive moat in its community banking model emphasizing relationships with minority and immigrant populations—a segment historically underserved by larger regional or national banks [S1][S13].

Historical Performance Trends

The company’s financial results reflect an impressive turnaround from prior years marked by losses and near-breakeven operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 29 | 56 | 1 | +161.6% |

| 2024 | 11 | 7 | 3 | +2018.1% |

| 2023 | 1 | 6 | 0 | +105.6% |

| 2022 | -9 | 10 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | 55 | 5.3 |

| 2024 | 11 | 4 | 2.2 |

| 2023 | 11 | 6 | 0.1 |

| 2022 | 2 | 9 | -1.9 |

Source: SEC companyfacts cache [F1].

Net income grew by over sixfold between FY23-25; operating cash flow showed a similarly steep acceleration reflecting improved core earnings quality ([F1]).

Several factors contributed to this performance improvement: the expansion of earning assets particularly real estate loans aligned with market recovery; prudent expense control; enhanced credit loss management; and improvements in deposit base stability.

Business Model Drivers

Niche Lending Focus

The company's specialization in non-owner-occupied multi-family housing loans places it at the crossroads of regulatory exposure but also high customer loyalty within targeted communities [S18]. Rent regulation policies notably inhibit landlords’ revenue growth potential—limiting borrowers’ cash flows—and thereby introduce elevated credit risk compared to typical single-family mortgage loans.

Regulatory & Legislative Headwinds

Several legislative actions since mid-2019 have restricted landlords’ ability to raise rents (elimination of vacancy/loyalty bonuses, removal of high-rent deregulation exceptions). Furthermore, new rules implemented by the NYC Rent Guidelines Board limit rent hikes to approximately 3% annually through October 2026—with discussions about rent freezes underway [S1][S25].

This legislative framework suppresses collateral values underpinning many loans held by Ponce Financial Group and could increase default rates if borrowers cannot meet debt service obligations.

Construction lending growth is influenced by expiration of historic tax incentive programs like NY’s former "421-a" program replaced recently by the "485-x ANNY" program requiring affordable units and compliance with wage mandates [S9][S25]. These changes add complexity—potentially restricting pipeline volume.

Capital & Liquidity Management

The bank meets or exceeds all minimum Basel III capital requirements including buffers (CET1 at least 7%, Tier1 leverage minimum at least 4%), which promotes safety but constrains capital deployment for dividends or buybacks [S10][F1]. Approximately one-fifth of deposits exceed FDIC insurance limits (22%), exposing the firm to risks of uninsured deposit withdrawals especially during systemic stress scenarios [S4][S6].

Deposit dependency is critical given the short-term nature of liabilities versus long-term illiquid loan assets, making liquidity management essential given potential deposit attrition or wholesale funding cost increases [S5][S16].

Operational & Technology Risk Controls

The firm operates in a high-volume transaction environment increasingly reliant on outsourced data processing vendors [S20][S21]. Cybersecurity risks remain elevated given ongoing threats; a dedicated security function reports regularly to board committees overseeing risk management [S23][S26]. Investments aim both at customer-facing enhancements as well as internal process efficiencies but require substantial ongoing expenditure.

Growth Prospects & Constraints

Growth opportunities reside primarily within expansion of lending into existing minority-focused neighborhoods plus possible incremental moves into neighboring communities sharing similar demographic profiles [S13][S14]. The firm's customer intimacy could enable tailored products not easily replicated by larger competitors aiming at broader markets.

However, growth is tempered by:

- Regulatory limits on commercial real estate concentrations—construction loans constitute ~145% of risk-based capital while broader CRE loans reach nearly double this threshold—triggering increased examiner scrutiny [S8][S9];

- Legislative limits on rental income raise delinquency risk among multifamily portfolios;

- Potential tightening of monetary policy influencing borrower repayment capacity;

- Competitive pressures potentially affecting deposit gathering capability;

- Industry-wide uncertainties stemming from geopolitical events or economic shocks impacting credit quality [S22][S24].

Absent explicit guidance disclosures from Ponce Financial Group about future milestones or forecasts beyond compliance status reporting [N/A], monitoring these regulatory developments alongside loan portfolio performance metrics will be critical indicators.

Capital Allocation & Returns

With an estimated Return on Equity at approximately ~5.3% for FY2025 ([F1]), returns appear modest relative to banking industry averages but reflect conservative capital provisioning.

Free cash flow generation approximates $54.6 million (operating cash flow net of capex) providing internal funding capacity for strategic initiatives including technology upgrade investments (~$1 million capex FY25) [F1]. Dividend payment details were not disclosed explicitly; however, regulatory buffers maintained imply some room for payout albeit limited.

Notably, the company has consistently completed share repurchases (~$11 million annually based on last available data) prior to FY2024 though recent specific buyback amounts were undisclosed [F1]. Equity incentive plans represent non-cash expense headwinds impacting net income marginally [S11].

Sector Context & Moat Analysis

Community banks like Ponce benefit from localized knowledge especially in ethnically concentrated urban centers where cultural affinities facilitate deeper engagement than larger banks typically offer . Such positioning fosters client stickiness but requires nimble adaptation when local politics or demographics shift—gentrification-induced displacement threatens core customer bases [S14].

The company's moat is thus dual-faceted: relationship-driven localized banking focused on underserved segments combined with disciplined prudent risk management responsive to evolving regulations.

Risks Summary

- Heightened exposure to rent control legislation restricting borrower revenue growth threatens credit quality.

- Limits imposed by federal regulators on CRE loan concentrations could force deleveraging potentially impacting revenue generation.

- Volatility in uninsured deposits coupled with reliance on wholesale borrowing sources create liquidity vulnerabilities.

- Operational risks inherent in third-party technology dependency increase cybersecurity exposure despite established controls.

- Political or social shifts adversely affecting targeted minority/immigrant markets could reduce demand for banking products.

- Variable macroeconomic conditions including inflationary pressures may erode net interest margins or elevate loan defaults.

Conclusion

Ponce Financial Group's demonstrated profit recovery post-2022 loss underscores resilience derived from community-rooted business lines that benefit significantly from focused market knowledge and niche specialization in New York City’s multi-family real estate sector. However, fundamental headwinds emanating from amplified regulatory scrutiny over commercial real estate portfolios, rent regulation laws curbing borrower revenue prospects, and structural liquidity fragilities necessitate vigilant strategy execution.

Maintaining compliance with evolving capital standards whilst investing judiciously in technology infrastructure for operational integrity represents a balancing act crucial to preserving their franchise value amid uncertain external conditions shaping future growth trajectories.

Disclaimer: This analysis is informational only based on publicly available documents as of March 14, 2026; it does not contain investment opinions or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments