Sachem Capital’s Recovery after 2024 Losses Hinges on Loan Portfolio Growth and Capital Access

After a steep net loss in 2024, Sachem Capital returned to profitability in 2025 but faces capital constraints and credit risks as it aims to expand its REIT mortgage loan portfolio.

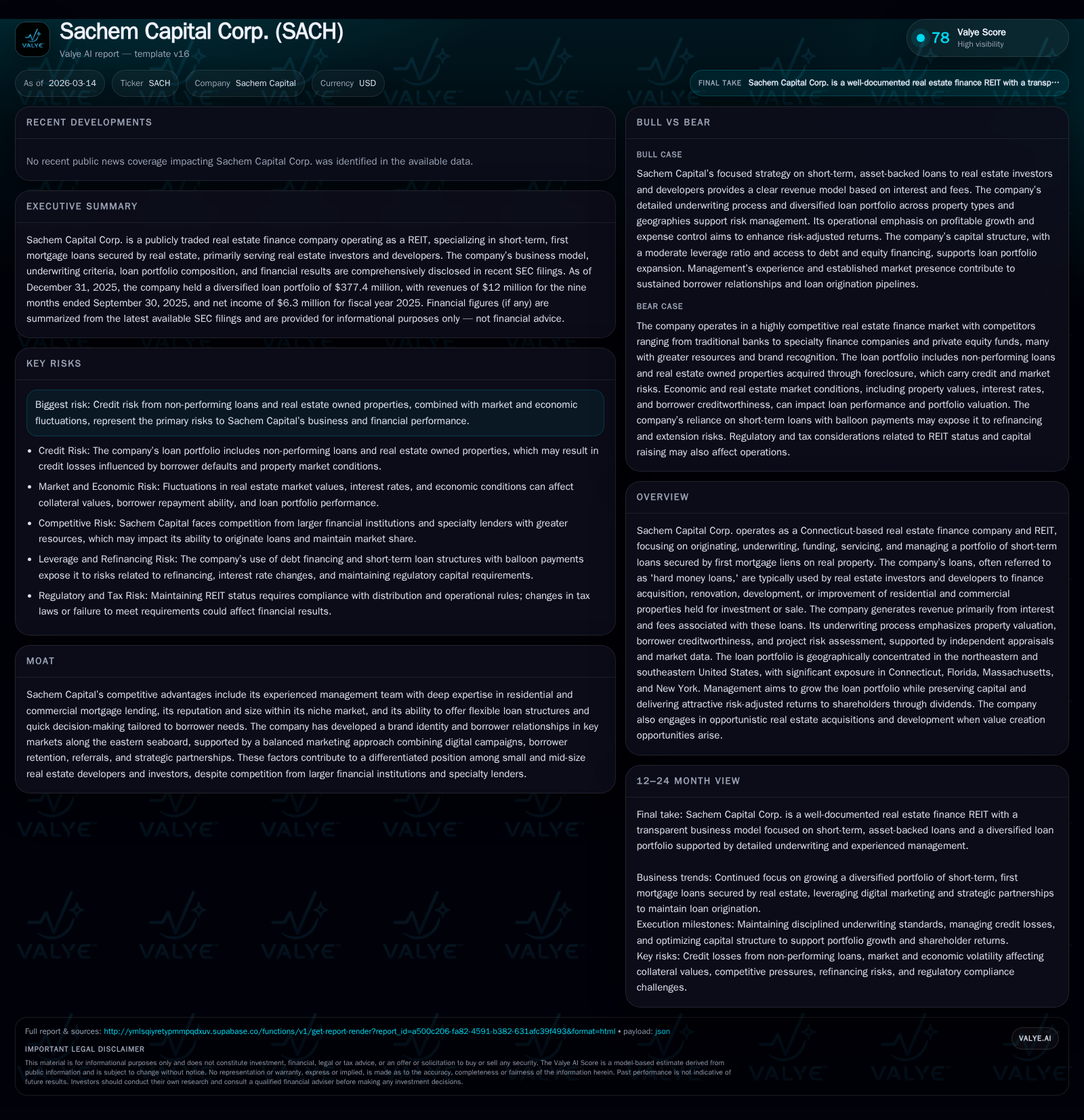

Sachem Capital Corp., a Connecticut-based real estate finance REIT specializing in short-term, first-lien mortgage loans to real estate investors, endured a challenging 2024 marked by an $39.6 million net loss driven by loan sales losses, credit impairments, and reduced revenue. In 2025, improved capital access and lower credit costs helped the company return to profitability with $6.3 million net income on steady revenues. The firm's near-term growth depends heavily on sourcing additional capital amid competitive lending markets and managing elevated nonperforming loans that weighed on past results. Capital structure maturities clustered in late 2026 and 2027 also pose refinancing risks and pressure on dividend payouts. Operationally, the company prioritizes underwriting discipline and leveraging relationships along the U.S. eastern seaboard to grow its loan portfolio with attractive risk-adjusted returns.

Company Overview

Sachem Capital Corp., based in Connecticut and operating primarily along the eastern seaboard of the United States, is a specialized real estate finance company structured as a REIT since its IPO in 2017 [S1]. The firm focuses on originating, underwriting, funding, servicing, and managing short-term (one to three years) mortgage loans secured by first liens on residential and commercial real estate properties held for investment or sale [S1]. These "hard money" loans typically serve real estate investors and developers who require flexible structures for acquisition, renovation or development projects.

Borrowers often provide additional collateral beyond the mortgaged property, such as pledges of ownership interests or personal guarantees from principals. Loans feature fixed interest rates generally between 10% to 13%, with default rates up to roughly double that level [S7]. Underwriting blends independent appraisals, credit assessments including third-party credit reports and financial document verification, alongside market conditions analysis [S8].

Historical Performance

Between fiscal years ended December 31 from 2021 through 2024, Sachem displayed overall growth punctuated by significant volatility:

- Revenue grew from approximately $30M in FY21 to a peak above $65M in FY23 before declining roughly 12% to $57.5M in FY24.

- Net income delivered consistent profits over these years until a dramatic full-year loss of about $39.6M recorded for FY24.

- Operating cash flow remained strong historically but plunged about 79% year-over-year in FY25 thus far.

The net loss in FY24 stemmed primarily from several large impairments: a $22M realized loss on sale of loans; nearly $27M provision for credit losses related to loans held for investment or transferred into real estate owned (REO) status; a roughly $5M valuation allowance for loans held for sale; plus smaller impairment charges on REO assets [S1]. The company also experienced an increase in nonperforming loans which contributed negatively both to revenues and capital availability as their capital markets access became constrained [S1].

Despite the challenging environment of high interest rates affecting borrowing costs and tighter lending conditions during this period across the real estate sector generally (analysis), Sachem managed through restructuring existing credit facilities and securing interim debt capital sources [S1]. This effort alongside disciplined underwriting improvements led to restored profitability for FY25 reported at approximately $6.3M [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | 3 | +115.9% | ||

| 2024 | 58 | -40 | 13 | -12.4% | -348.9% |

| 2023 | 66 | 16 | 22 | +25.5% | -24.0% |

| 2022 | 52 | 21 | 13 | +71.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 0 | 3.6 |

| 2024 | 1489000 | -21.8 |

| 2023 | 226327 | 6.9 |

| 2022 | 9.6 |

Source: SEC companyfacts cache [F1]. (from -39M)

*Dividends reduced starting in late 2023 due to capital constraints; buybacks ceased in FY25. **Capex doubled compared to prior years but remains under $1.2M. (Figures mostly from [F1], dividend details from [S1])

Loan Portfolio Dynamics

As of December 31, 2025, Sachem's mortgage loan portfolio held for investment stood near $377 million—largely unchanged from end-2024 levels (~$377 million), indicating stability but little growth yet post-crisis [S4][F1]. Weighted average contractual interest rates increased modestly from ~12.53% at end-2024 to about 13.10% at end-2025 reflective of higher-rate loan originations [S4]. Term lengths averaged approximately eight months.

Non-performing or non-accrual loans represent significant credit risk: at September 30, 2025 data shows over $100 million of loans held for investments classified as non-accrual representing an elevated share (~28%) of total portfolio outstanding balances [S14][S16]. This compares unfavorably with prior periods though provisions have been made reducing allowance for credit losses from nearly $18.5 million down to about $11 million over twelve months indicating progress but persistent challenges [S14][S16].

Exposures are diversified across several geographies within northeastern and southeastern U.S markets with significant concentrations still present in Connecticut among other states along the eastern seaboard [S20]. Single borrower risk is notable; one borrower comprised roughly ~13-14% of total outstanding principal balance representing concentration risk inherent with mid-sized REIT structures focused on hard-money lending [S18][S25].

Capital Structure

As detailed at December 31, 2025, Sachem carried total indebtedness approximating $278 million comprising:

- Approximately $171 million of unsecured notes payable,

- About $86 million senior secured notes payable,

- Nearly $19 million outstanding on revolving lines of credit,

- A minor mortgage payable balance around $0.9 million, with liabilities secured mainly via first priority liens excluding some REO assets [S10][F1]. This leverage translates into debt constituting roughly 61% of total capital compared to ~62% previously demonstrating slight deleveraging amidst repayment efforts [S5][F1].

A critical near-term liquidity factor is the large volume (~$173 million) of notes maturing between December 30, 2026 and September 30, 2027 creating refinancing risks especially considering market volatility affecting credit spreads and interest rates [S10][S17]. Default-triggering cross-default clauses impact multiple facilities increasing operational risk if any covenant breaches occur.

The Needham Credit Facility requires maintenance of a debt service coverage ratio not less than 1.4x—a covenant Sachem has met but cautions compliance could be jeopardized under certain stress scenarios potentially causing lender defaults cascading across obligations including smaller NHB Mortgage liens securing corporate office property collateral [S10][S16].

No new share repurchases took place in FY25 reflecting earnings pressures while dividends were deliberately reduced starting circa FY24 amid taxable income declines though distributions continue per Board discretion subject to liquidity considerations preserving REIT status requirements [S1][F1].

Growth Outlook

Company published strategy emphasizes accelerating profitable growth via selective origination paired with operational excellence focusing on cost containment relative to revenue scaling [S1]. Given current capital access constraints due to prior year market conditions restricting issuance capability alongside challenging note maturities looming by late '26/'27; growth potential will hinge crucially on successful refinancing or new capital raises enabling expansion beyond current stable portfolio size.

The underwriting approach favors loan-to-value ratios capped typically at ~70%, stretching up to ~85% when factoring renovation/construction cost basis allowing calibrated risk taking per project specifics while leveraging collateral enhancement strategies such as supplementary borrower guarantees supporting asset-backed security quality [S7][S8]. This rigor along with responsive pricing flexibility underpins assumed competitive moat targeting underserved small/mid-size borrowers requiring structural agility uncommon among larger institutions with more rigid frameworks [S20]. Maintaining strong borrower/provider relationships through SEO-based digital marketing campaigns plus referrals adds channels for deal flow critical during tight markets [S20].

Risks remain substantial particularly related to worsening macroeconomic factors that could weaken property values or disrupt local markets hence elevating credit costs further against thinner reserves maintained recently (~$11M) despite shrinkage from prior peak levels [S14][F1]. Additionally refinancing concentrations could exert material pressure impacting dividend capacity or forcing asset sales at discounts if liquidity is impaired.

Returns & Capital Allocation

For fiscal year ending December 31 2025, Sachem reported net income attributable to common shareholders totaling approximately $6.3 million translating into an estimated return on equity close to ~3.6%, notably recovering sharply after substantial losses posted in prior year ($39.6 million loss in FY24) [F1].

Operating cash flow contracted sharply undermining free cash flow generation though remaining positive near $1 million after modest capex expenditures which have increased steadily reflecting incremental investments likely aimed at operational infrastructure improvements or maintaining facilities [F1].

Dividend reductions enacted since mid-2023 align with diminished taxable income resulting largely from constrained origination activity linked with limited growth capital access during adverse market cycles [S1][F1]. No buybacks executed since early FY25 reflecting cautious capital deployment stance emphasizing financial flexibility preservation amid ongoing debt maturities approaching sooner than ideal horizon captivates management focus away from shareholder returns toward balance sheet stabilization.

Competitive Positioning & Strategy Nuances

Despite intense competition from regional banks, specialty finance companies including private equity funds backed platforms often enjoying deeper pockets or established banking relationships Sachem leverages several protective moats:

- Deep localized expertise concentrated along eastern seaboard allowing nuanced market insight,

- Nimbler underwriting pivoting quickly around individual borrower intricacies,

- Flexible structuring accommodating borrower needs enabling higher closing velocity relative to traditional lenders,

- Balanced marketing mix coupling digital presence with direct referrals fueling consistent loan pipeline development[S20]. These factors position Sachem well within niche small-mid size developer/investor segments who value speed plus bespoke term sheets versus commoditized offerings prevalent among larger institutions.

Risks Summary

Key operating risks center predominantly around:

- Credit deterioration tied closely to economic cycles impacting property values,

- Concentrated debt maturities risking refinancing challenges during unfavorable capital markets conditions,

- Elevated nonperforming loan levels possibly constraining available liquidity or requiring further loss provisions,

- Potential covenant breaches triggering accelerated repayments or lender remedies limiting operational agility,

- Restrictions from legal corporate governance frameworks influencing dividend capacity. These material uncertainties underscore the importance of prudent portfolio management accompanied by measured leverage deployment as central pillars ensuring sustainable long-term shareholder value creation.

What To Watch (Analysis)

Without detailed forward guidance disclosed openly within filings recent as of March 14 2026 there is no formal forecast articulated regarding loan origination targets or explicit milestone achievements beyond typical operational objectives described annually. Investors should monitor quarterly updates for:

- Changes in non-accrual loan balances signaling either stabilization or further deterioration,

- Key forthcoming debt maturity refinancing announcements elucidating cost-of-capital expectations,

- Dividend policy adjustments reflecting underlying cash flows trends,

- Growth trajectory evidenced through gross loans disbursed figures capturing demand momentum shifts,

- Any strategic partnership formations enhancing distribution channels. Such developments will gauge whether Sacham can extend its recent recovery path towards robust sustainable expansion versus continuing cyclical headwinds common within specialized real estate finance niches.

This report summarizes public information without incorporating any investment recommendations or price forecasts about Sachem Capital Corp., focusing instead on objective analysis grounded exclusively in disclosed data and filings as of March 14 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments