Walmart’s Expanding Omnichannel Model and Cost Management Sustain Moderate Growth in FY2026

Walmart Inc. leverages its scale, omnichannel integration, and disciplined capital allocation to drive steady revenue growth while navigating margin pressures and regulatory challenges.

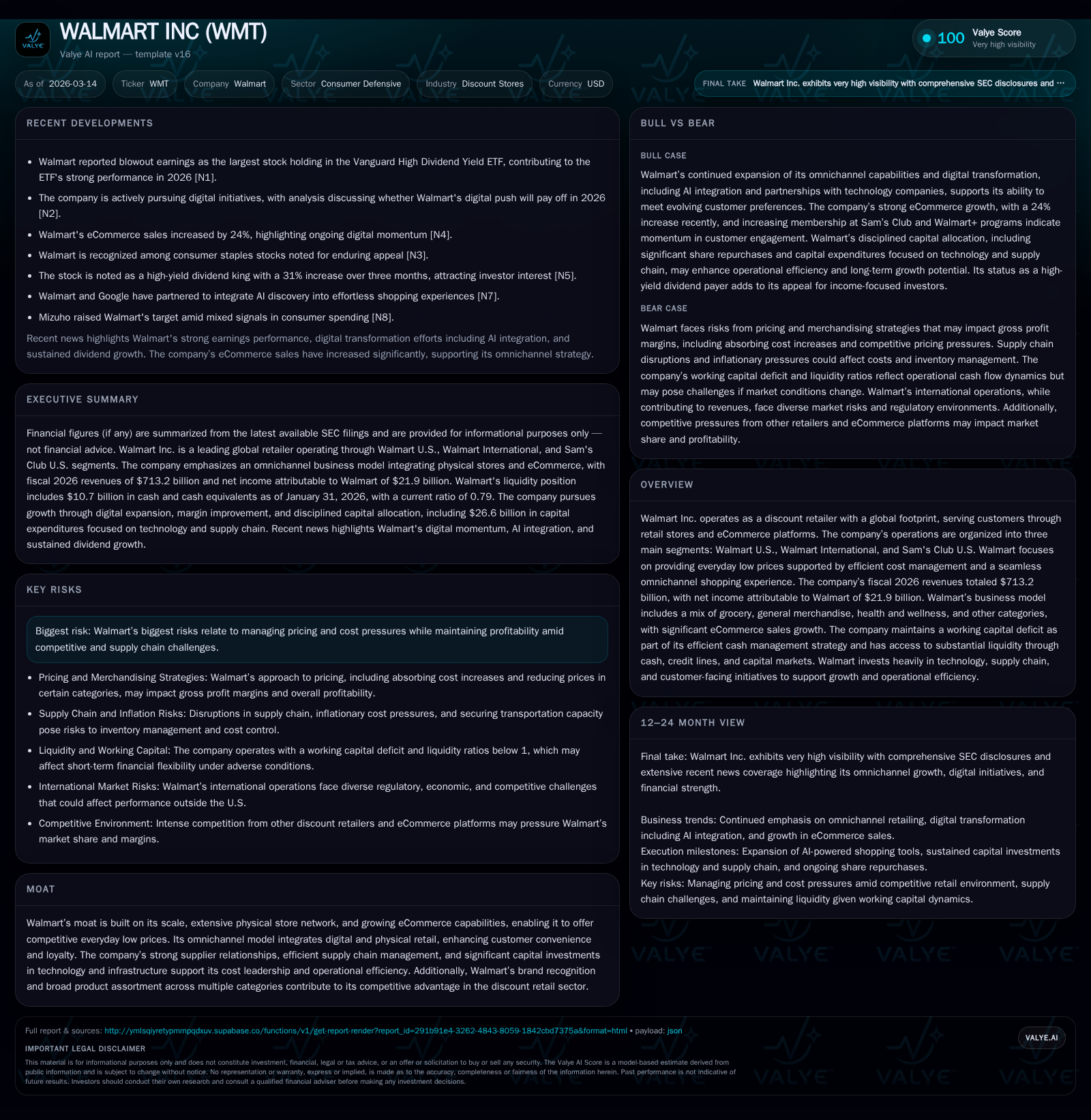

In fiscal 2026, Walmart reported $713.2 billion in revenues, marking a 4.7% increase over the prior year driven by growth in eCommerce and grocery categories. Operating income grew modestly by 1.6%, reflecting higher expenses including claims and compensation adjustments. The company continues to prioritize seamless customer experience through investments in technology, supply chain, and store remodels. Legal and regulatory risks persist, particularly related to Mexico antitrust rulings and ongoing opioid litigations. Robust cash flows support dividends and share repurchases amid cautious margin management.

Historical Financial Performance

Walmart Inc.’s recent fiscal years have demonstrated steady top-line growth supported by both traditional retail and eCommerce channels. For fiscal year ended January 31, 2026 (FY2026), Walmart's consolidated revenue stood at approximately $713.2 billion, reflecting a 4.7% increase compared to FY2025's $681.0 billion [F1]. This trend continues from prior years where revenue grew from $648.1 billion in FY2024 and $611.3 billion in FY2023.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | 713.2 | 21.9 | 41.6 | 29.8 | +4.7% | +12.6% |

| 2025 | 681.0 | 19.4 | 36.4 | 29.3 | +5.1% | +25.3% |

| 2024 | 648.1 | 15.5 | 35.7 | 27.0 | +6.0% | +32.8% |

| 2023 | 611.3 | 11.7 | 28.8 | 20.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2026 | 8.1 | 14.9 | 22.0 |

| 2025 | 4.5 | 12.7 | 21.4 |

| 2024 | 2.8 | 15.1 | 18.5 |

| 2023 | 9.9 | 12.0 | 15.2 |

Source: SEC companyfacts cache [F1].

All figures in billions USD; OpInc = Operating Income; Net Inc = Net Income; CFO=Cash Flow from Operations; Capex=Capital Expenditures.

Operating income increased modestly by about 1.6%, from $29.3 billion in FY2025 to $29.8 billion in FY2026 [F1]. The gross profit rate improved slightly to around 24.2% due to disciplined inventory management and growth in higher-margin businesses mainly within the U.S segment [S16]. However, operating expenses as a percentage of sales increased as general liability claims rose by approximately $0.9 billion alongside share-based comp modifications related to non-U.S operations such as PhonePe [S16].

Net income showed stronger growth (+12.6%) driven partly by favorable tax impacts from the U.S.'s One Big Beautiful Bill (OBBB Act), which allowed full expensing on R&D expenditures though overall tax expense impact remained modest [S1]. Operating cash flow expanded significantly (+14%), reaching roughly $41.6 billion thanks to operational efficiencies and strong collections [F1]. Capital spending grew by about 12%, focused largely on supply chain automation projects, technology implementations supporting omnichannel fulfillment, as well as store remodeling initiatives [S20].

Segment Dynamics & Market Position

Walmart operates three principal segments: Walmart U.S., Walmart International, and Sam's Club U.S., collectively addressing diverse consumer categories including grocery, general merchandise, health & wellness, and digital advertising services.

Within the U.S., comparable store sales increased approximately +4.3% for FY2026 despite no meaningful fuel impact compared to prior years [S1]. Of significance, eCommerce sales continued robust expansion with an estimated growth rate near +24% during early calendar year reporting periods [N6]. By FY2026 end, approximately $99.6 billion of U.S segment net sales involved digital channels representing nearly one-fifth of its total U.S sales volume [S21].

International segment revenue also increased materially though currency fluctuations and local market dynamics exert mixed pressure on margins [S14]. For example, Walmart’s Mexican subsidiary encountered regulatory scrutiny over monopolistic practices involving supplier arrangements resulting in a monetary penalty of around $5 million USD currently under appeal [S4][S5]. Compliance with COFECE’s ruling requires modification of supplier contribution negotiations impacting strategic sourcing approaches.

Among its competitive advantages, Walmart’s moat depends on the expansive physical footprint combined with growing digital capabilities forming an integrated omnichannel customer experience . The company leverages deep supplier relationships for cost leadership while investing heavily in infrastructure that enables seamless inventory replenishment.

Future Growth Prospects & Catalysts

Looking ahead, Walmart aims to accelerate growth via continued omnichannel initiatives including expansion of membership programs such as Walmart+ and Sam's Club memberships that enhance customer loyalty [S1]. Broad category diversification spanning essential grocery through discretionary goods cushions sales against sector volatility.

Digital advertising is another burgeoning line contributing higher margin revenue streams atop traditional retail sales—a structural shift reflecting the value derived from data insights and targeted marketing embedded within Walmart’s ecosystem [S16]. The integration of artificial intelligence into inventory management systems and personalization likewise promises operational efficiencies that could expand margins long term [N3][N4].

However, growth could face constraints from intensifying competition from both brick-and-mortar discounters like Costco or Target as well as pure-play eCommerce giants pressuring pricing power . Moreover, inflationary cost pressures ripple across logistics inputs raising freight costs despite efforts to secure ocean carrier contracts earlier or in bulk [S1][S14]. Regulatory matters—such as ongoing lawsuits related to opioid distribution practices with trials scheduled through late-2027—introduce potential financial uncertainties for provisions or settlements affecting cash flow stability [S9][S11][S12].

Forecasts & Milestones To Monitor

Explicit forward guidance beyond FY2026 has not been detailed publicly; however key performance indicators going forward will likely encompass:

- Comparable store sales trends inclusive of omnichannel penetration rates.

- Momentum in eCommerce sales growth during pivotal quarters.

- Progression of legal appeals such as Walmex’s antitrust case resolution.

- Margin trends reflecting mix effects from higher margin services versus commodity merchandise.

- Capital expenditure allocation shifts towards automation vs expansion projects. Monitoring these data points will reveal how effectively Walmart navigates external cost pressures while continuing innovation-led differentiation .

Returns & Capital Allocation Discipline

Walmart displayed strong capital discipline balancing reinvestment with shareholder returns:

- ROE approximated at around 22%, robust given incremental capital spending requirements [F1].

- Free cash flow—defined here as operating cash flow less capital expenditures—approached an estimated $14.9 billion in FY2026 indicating solid internal funding capacity for dividends and buybacks [F1][S20].

- Dividend payments remain a cornerstone although exact recent payout figures are unspecified within latest filings; historically stable dividend policy supports shareholder income generation .

- Share repurchases accelerated sharply in FY2026 at roughly $8.1 billion compared to prior years signaling confidence in valuation opportunities amid evolving capital priorities [F1].

Liquidity metrics reveal a working capital deficit (current assets less current liabilities negative), typical for large retailers due to extended payables cycles balancing cash conversion efficiency despite tight current ratio near ~0.79 [F1][S13]. Long-term debt totaled approximately $38 billion with favorable credit ratings maintained across agencies positioning Walmart advantageously for refinancing needs without liquidity strain [S13][S18].

Risk Profile & Legal Challenges

Operational risks stem largely from managing price-cost dynamics amidst inflationary headwinds while maintaining competitive everyday low prices driving customer loyalty [S1][S14]. More pronounced are ongoing contingencies:

- Mexico antitrust settlement penalties contested in courts potentially impacting supplier terms and costs [S4][S5].

- Litigation concerning driver classifications under the Spark platform resulted recently in a stipulated settlement judgment accrual of roughly $37 million plus programmatic obligations lasting a decade per FTC mandates [S8][S11].

- Continuing exposure remains around opioid-related civil litigation across multiple jurisdictions including federal multidistrict litigation with upcoming trials slotted through late calendar year 2027 presenting uncertain financial outcomes despite prior sizeable settlements concluded within FY2023–FY2025 periods [S9][S10][S12][S17].

- Foreign direct investment regulatory probe into Indian Flipkart subsidiary persists but is at an early procedural stage without definitive resolution expected imminently affecting international operations risk profile [S19]. These legal matters underpin a need for cautious financial forecasting given potential material liabilities beyond amounts currently recognized.

Summary Assessment

Walmart’s business model continues demonstrating resilience through extensive scale combined with an evolving omnichannel ecosystem that supports stable revenue growth despite margin headwinds from inflation-related costs and legal exposures systemically inherent to large multinational retailers. Its sizable investments into technology-enabled automation serve dual purposes: enhancing customer convenience across digital channels while improving operational efficiency that could incrementally bolster profitability longer term. Though returns remain healthy driven by strong free cash generation supporting shareholder distributions alongside disciplined capital expenditure deployment geared toward future growth areas. The company must carefully balance competitive pricing strategies required by customer expectations against escalating input costs while managing reputational risk linked to ongoing legal proceedings globally. Ultimately Walmart exemplifies a mature industry leader leveraging entrenched assets but facing challenges typical for incumbents requiring constant strategic adaptation within retail's dynamic environment.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments