Harvard Bioscience Faces Profitability Challenges While Advancing Translational Medicine Focus

The company pursues operational consolidation and product portfolio evolution amid a volatile financial backdrop.

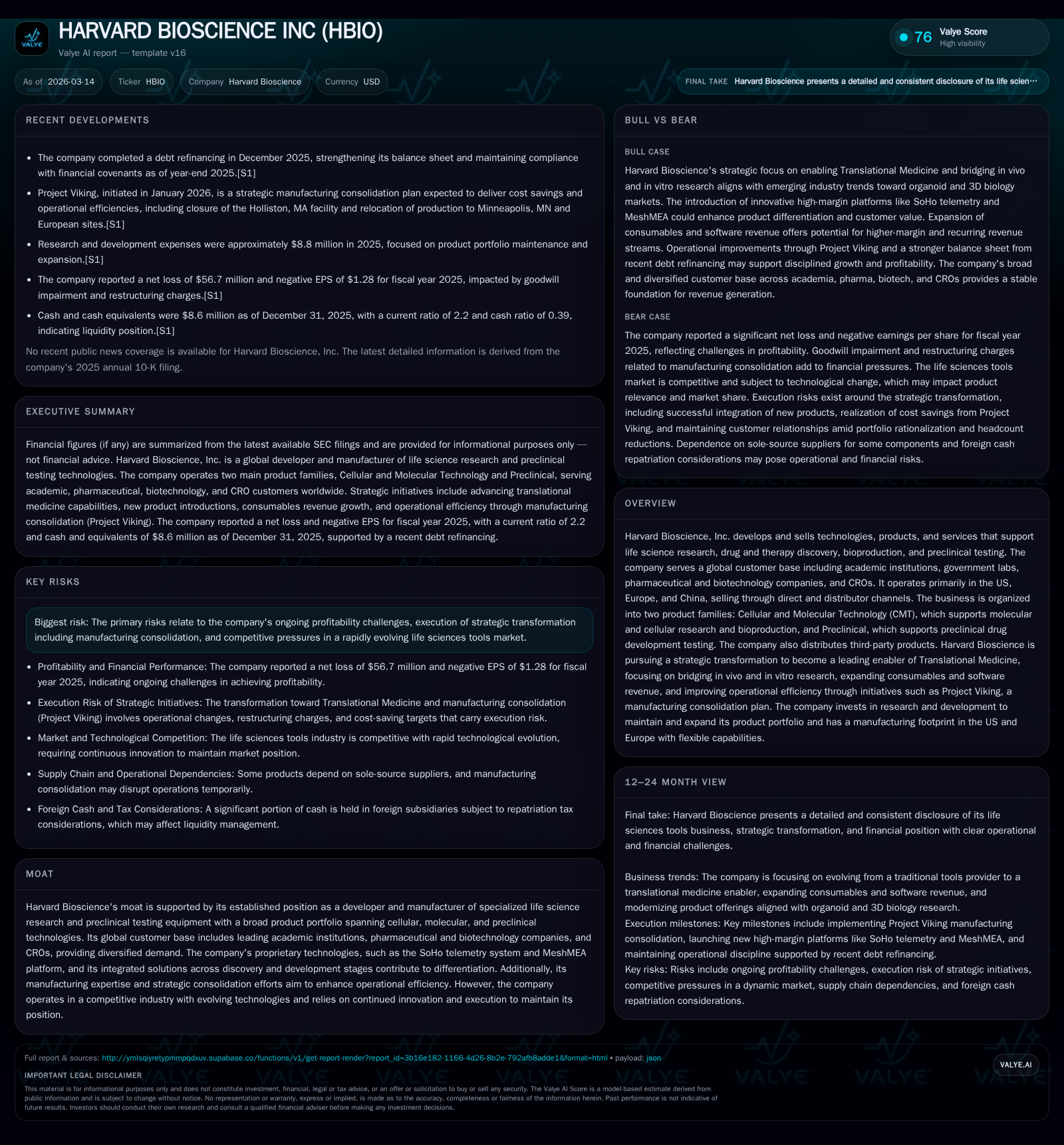

Harvard Bioscience Inc. develops specialized life science research and preclinical equipment, targeting translational medicine through bridging in vivo and in vitro workflows. Despite broad global reach and a diverse customer base, the company reported a steep decline in profitability in 2025, with operating loss expanding to $48.6 million and net losses exceeding $56 million [F1]. The strategic plan centers on manufacturing consolidation to improve margins and a shift toward high-margin consumables and software to increase recurring revenues [S1,S26]. Key risks include execution of Project Viking restructuring, intense competition, and ongoing leverage from debt refinancings in late 2025 [S4-S13].

Historical Performance

Harvard Bioscience has demonstrated fluctuating revenue trends over recent years with an inflection around 2019 when reported revenue surged sharply to approximately $116 million from much lower levels (circa $33.9 million in 2018), partly reflecting acquisition integration effects and broader market penetration [F1]. However, this growth momentum shifted as revenues declined to about $86.6 million in 2025 from $94.1 million in the prior year — a drop of roughly 8% year-over-year considering the latest filings [F1].

Operating income has exhibited considerable volatility reflective of both operational challenges and non-recurring items. After turning positive modestly in 2023 ($1.9 million), operating income plummeted to negative $6.2 million in 2024 before collapsing to negative $48.6 million in 2025, largely attributable to goodwill impairment charges exceeding $47 million recorded earlier in 2025 as well as restructuring expenses linked to Project Viking [F1,S17]. This indicates mounting pressure on core profitability despite efforts to optimize operations.

Net income mirrored these trends with losses escalating annually — from negative $3.4 million in 2023 to nearly -$12.4 million in 2024, before further swelling to an extraordinary -$56.7 million loss reported for the full year ended December 31, 2025 [F1]. This magnitude highlights systemic issues beyond typical cyclicality.

Cash flow from operations provided some respite with a gradual improvement; operating cash flow expanded from roughly $1.4 million in 2024 to nearly $6.7 million last year despite net losses suggesting working capital management contributed positively [F1]. Capital expenditures contracted significantly by over half compared to prior years ($1.26 million in 2025 vs $2.64 million in 2024), helping free cash flow remain positive around $5.47 million — critical given ongoing debt obligations [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -57 | 7 | -49 | 1 | -357.1% |

| 2024 | -12 | 1 | -6 | 3 | -263.3% |

| 2023 | -3 | 14 | 2 | 2 | +64.1% |

| 2022 | -10 | 1 | -7 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | -412.8 |

| 2024 | -1 | -19.6 |

| 2023 | 12 | -4.7 |

| 2022 | 0 | -13.2 |

Source: SEC companyfacts cache [F1]. Note: Revenue YoY computed versus recorded values; Net YoY % reflects large impairments distorting trend.

Business Overview & Strategy

Operating since its incorporation successor entity status since November 2000, Harvard Bioscience maintains a legacy founded on life science research instrumentation dating back over a century but strategically positioning itself for the future through a portfolio spanning cellular and molecular technologies (CMT) alongside robust preclinical testing hardware and software solutions supporting drug discovery workflows globally [S1,S28].

The business serves diverse customers including pharmaceutical leaders such as Amgen, AstraZeneca, Johnson & Johnson, Pfizer; top-tier academic institutions like Harvard University and Cambridge University; plus contract research organizations (CROs) like Charles River Labs — highlighting breadth across commercial R&D ecosystems ensuring exposure across therapeutic modalities and geographies primarily concentrated in the US, Europe, and China [S10,S28].

Management articulates four main strategic pillars:

Leading the Translational Bridge: Leveraging its preclinical heritage to support the industry's shift into organoid/3D biology models enhancing relevance of early-stage drug discovery.

New Product Introductions (NPI): Development of innovative platforms including SoHo™ telemetry systems for wireless implantable monitoring alongside proprietary MeshMEA and Incub8 tissue recording technologies enabling precision analyses.

Consumables Revenue Expansion: Focusing on increasing proportion of high-margin consumables/software aiming for recurring revenue share growth beyond current ~55% baseline.

Operational Excellence & Disciplined Growth: Driving consistent profitability underpinned by manufacturing consolidation efforts (Project Viking), portfolio rationalization removing non-strategic SKUs, cost control measures, alongside leveraging preclinical business cash flows for funded growth investments including inorganic bolt-ons aligned with strategy [S1,S26,S27].

Recent Developments & Forecast Outlook

Significant attention centers on Project Viking, announced January 2026: a strategic consolidation initiative expecting to close the Holliston MA production site shifting capacity primarily to Minneapolis MN hub with other operations moved across European facilities optimized by product lines for enhanced throughput and logistics efficiency [S1,S27].

Project Viking targets annual cost savings estimated at $3M beginning calendar year 2027 escalating to ~$4M annually post-2028 after initial restructuring costs are absorbed ($3.4M-$4.4M pre-tax charges including ~$0.6M non-cash asset write-offs tied primarily to facility exit). These savings aim at margin improvement offsetting competitive pricing pressures prevalent in life science tools markets prone to rapid technological evolution requiring continuous upgrades [S27].

Additionally, December-end refinancing extended debt maturities through end of calendar year 2029 via Term A ($10M), Term B ($22.5M), Term C ($7.5M convertible loan) tranches carrying elevated all-in interest rates starting near ~12.8%, reflecting heightened credit risk perceptions but providing covenant relief improving liquidity runway post prior financial covenant breaches mid-2025 . This larger debt package replaced former credit agreements facilitating capital structure stability albeit with increased servicing costs evidenced by rising interest expense totaling about $4.9M last year (+39% YOY) adding pressure on free cash flow generation capacity [F1,S15,S17].

Research & Development investment stood at approximately $8.8M for calendar year-end December ’25 down from circa $10.4M previously indicating prioritization against tightening expense controls but underscoring vital role of innovation pipelines underpinning new product launches crucial for differentiation especially within emerging organoid/3D biology niches targeted by SoHo™, MeshMEA technologies among others [S17,S26].

Harvard Bioscience management commentary emphasizes pathway transitioning into higher recurring revenue streams dominated by consumables/software accompanied by selective discontinuations of mature low-growth product lines signaling portfolio streamlining complementing manufacturing footprint optimization efforts mentioned above—critical given gross margin expansion imperatives under competitive conditions consistent with NAMs adoption trajectory accelerating drug discovery modernization industry-wide [N2,S16,S26].

Returns & Capital Allocation

The company did not declare dividends nor repurchase shares during recent periods reflective of preservation focus amidst structural deficits exacerbated by impairment charges that skew traditional ROE calculations deeply negative (-413% approximated using latest net income against equity) indicating capital erosion rather than generation last fiscal year ending December ’25 [F1].

Reported cash balance improved by over double relative prior year to roughly $8.6M while maintaining conservative working capital management producing positive operating cash flow nearing seven million dollars supporting capex outlay just above one million dollars — conservative investment profile designed maintain asset base whilst funding necessary growth initiatives without excessive leverage increments or dilutive capital raises observed recently via convertible notes/warrants issuance accompanying refinancing transactions executed late last year offering optionality albeit shareholder dilution potential remains an ongoing consideration depending on equity price trajectories

Industry Context (Analysis)

Life sciences R&D instrumentation is marked by fragmentation but driven heavily by shifts toward sophisticated cell models such as organoids requiring advanced measurement platforms merging electrical signals recording (multi-electrode arrays) with telemetry enabling wireless data capture—fields where Harvard’s novel MeshMEA system and SoHo telemetry may yield competitive advantages if coupled with effective commercialization execution.

Furthermore, global regulatory pressure encouraging NAMs adoption aligns with Harvard’s strategic transformational emphasis facilitating their positioning bridging traditional animal models (in vivo) and cell-based assays (in vitro). Yet persistent challenges include rapid technology obsolescence rates demanding constant R&D investments balanced against manageable operating expenses amidst tightening pharma R&D budgets evolving under macroeconomic uncertainties.

Consolidation within instrument manufacturers sector also exerts pricing pressures concurrent with distributors increasingly pushing for endpoint consumables supply chain efficiencies creating margin compression risks unless mitigated through scale advantages or proprietary platform lock-ins bolstered by recurring consumable sales contracts—a dynamic Harvard explicitly targets through its evolving value proposition shift.

Key Risks & Considerations

The primary risks stem from execution uncertainties related to substantial Project Viking restructuring including operational disruptions or failure realizing targeted cost savings that could exacerbate margin pressures already reflected in enlarged operating losses recently recorded [S16]. Moreover, intensifying competitive landscape fueled by well-funded incumbents pursuing alternative technology modalities could erode market share absent sustained innovation velocity given that Harvard operates within niche specialized instrumentation disciplines vulnerable to substitutes.

Financial risk remains notable due to significant indebtedness incurred following December quarter refinancing bearing high fixed interest burdens which compress available cash flow despite covenant compliance verified at year-end ’25 measurement dates necessitating vigilant liquidity management especially if economic headwinds worsen or sizeable acquisition-led strategic moves materialize adding leverage layers abruptly without commensurate earnings enhancement immediately realized.

Legal contingencies exist including ongoing defense against claims though currently assessed as immaterial possibly ranging up to $0.8M addressable through provisions without threatening enterprise viability directly according to latest disclosures although any material adverse outcomes would need reevaluation impacting operational forecasts [S21].

Conclusion & What To Watch (Analysis)

Monitoring Harvard Bioscience involves tracking execution progress on Project Viking manufacturing consolidation milestones delivering promised cost synergies beginning calendar ’27 along with innovation pipeline effectiveness notably commercialization traction of differentiated platforms like SoHo™, MeshMEA targeting translational medicine market niches increasingly prioritized by pharmaceutical clients would be critical indicators gauging strategic transformation success.

Concurrently assessing financial health stability post-refinancing is vital given sizable leverage deployed; watch quarterly liquidity ratios alongside interest coverage metrics given elevated coupon structures dictating tight margin maintenance necessities until turnaround evidence emerges reflected perhaps initially through stabilization or growth resumption within top-line revenues shifting toward higher-margin consumables dominance over time.

The company’s capacity to capitalize on its extensive global customer relationships spanning academia and industry remains an important advantage but requires operational discipline balancing cost controls with selective reinvestment sustaining competitiveness within fast-evolving life sciences tools landscape increasingly emphasizing automated organoid electrophysiology measurements powered via integrated hardware-software ecosystems.

This analysis is based solely on publicly available information sourced from company filings, transcripts, news releases, and standardized data repositories without any forward-looking investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments