El Pollo Loco Holdings Balances Brand Strength with Capital Allocation and Expansion Plans

El Pollo Loco leverages its regional dominance and franchise growth while managing liquidity constraints and evolving consumer patterns.

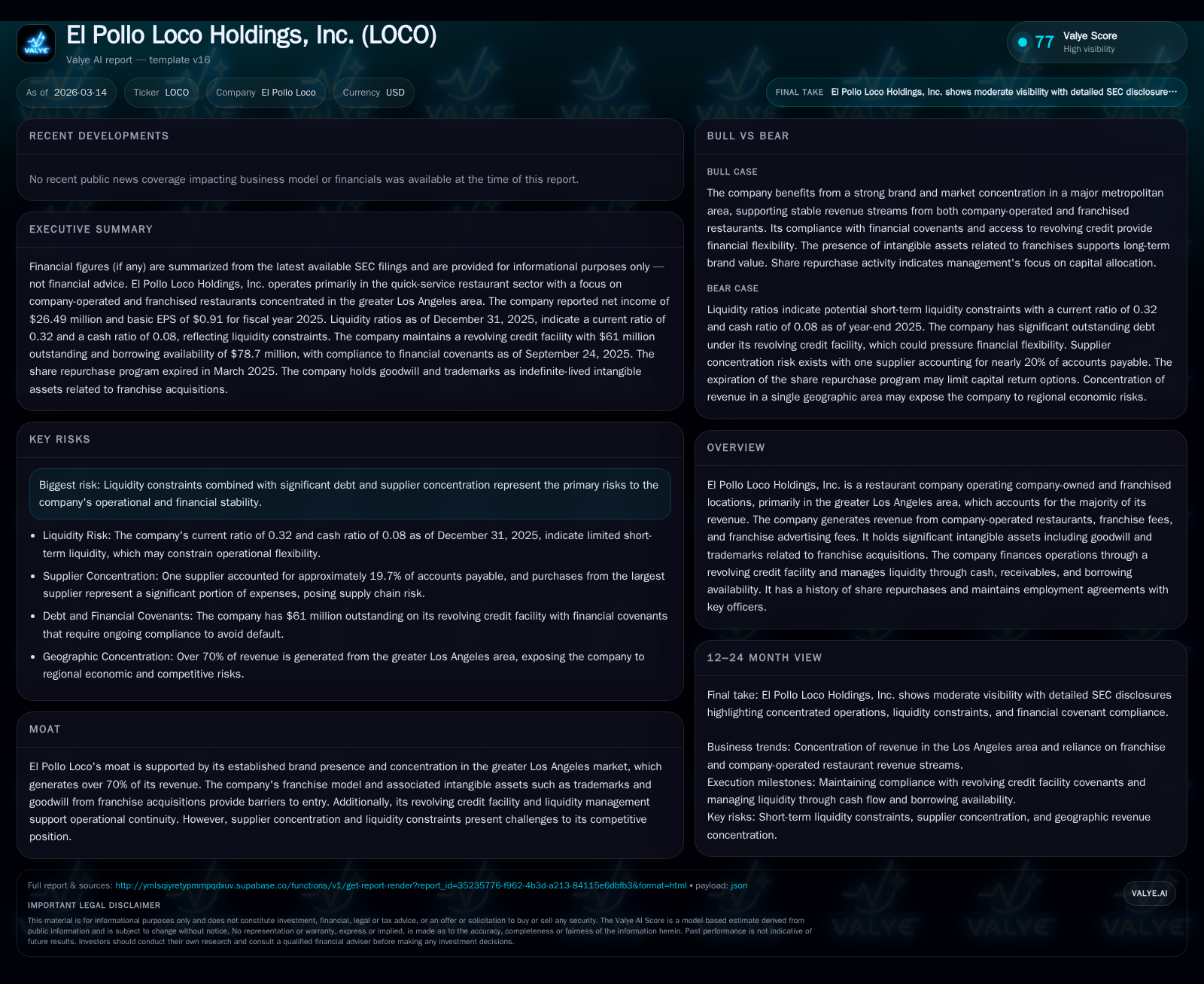

El Pollo Loco Holdings, Inc. continues modest revenue growth primarily through concentrated operations in the Greater Los Angeles area and a cautiously expanding franchise network. Fiscal 2025 results reflect stabilized comparable restaurant sales driven by pricing strategies offsetting softer transaction counts, alongside deliberate unit expansion favoring franchised restaurants. The company's capital allocation shows a shift from heavy share repurchases toward increased investment in new stores and remodels, amid liquidity-tight debt facilities with restrictive covenants. Going forward, monitoring comparable sales momentum, unit economics, and debt management will be critical to sustaining growth amid supplier concentration risks.

Steady Revenue Growth Supported by Regional Focus and Pricing Power

El Pollo Loco's revenue increased approximately 2.9% year-over-year in fiscal 2025, supported by pricing strategies and stable company-operated unit performance [F1][S1]. The brand’s significant presence in the Greater Los Angeles area contributes to more than 70% of total revenues , enabling targeted pricing that raised average check sizes by about 2.1% at company-operated restaurants despite a decline in transaction volumes of approximately 1.8% during fiscal 2025 [S1].

This dynamic led to relatively stable comparable restaurant sales: company-operated units grew slightly by 0.3%, while franchise-operated locations recorded flat performance year-over-year [S1]. These figures highlight resilience amid evolving consumer preferences.

### Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

| --- | :---: | :---: | :---: | :---: | :---: |

| 2025 | 26 | 48 | 42 | 23 | +3.1% |

| 2024 | 26 | 47 | 41 | 19 | +0.5% |

| 2023 | 26 | 41 | 40 | 21 | +22.8% |

| 2022 | 21 | 39 | 30 | 20 | |

*Source: SEC companyfacts cache [F1].*

### Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

| --- | :---: | :---: | :---: |

| 2025 | | 2 | 25 |

| 2024 | 56 | 21 | 28 |

| 2023 | 56 | 59 | 19 |

| 2022 | 56 | | 19 |

*Source: SEC companyfacts cache [F1].*

*Revenue values for recent years are not fully available from public datasets; operating income, net income, cash flow from operations (CFO), and capital expenditures (Capex) are reported in millions USD per SEC filings [F1].

Restaurant Development: Franchise-Led Growth Strategy

As of December 31, 2025, El Pollo Loco operated approximately 503 restaurants across nine states [S1]. In fiscal 2025, the company opened one new company-operated location in California while franchisees opened eight new restaurants across several states including California, Arizona, Colorado, Texas, New Mexico, and Washington [S1]. No company-operated closures occurred during this period; however, franchisees closed four locations.

The company’s strategy focuses on expanding its footprint primarily through franchising to leverage "Winning Unit Economics" and reduce capital intensity associated with direct operations [S1]. For fiscal 2026, management plans to open three to four new company-operated restaurants mainly in California and Texas alongside an anticipated fifteen to sixteen new franchised restaurants nationwide [S1][N2].

Comparable Sales Dynamics Reflect Consumer Behavior Shifts

System-wide comparable restaurant sales rose slightly by 0.1% in fiscal 2025 with divergent trends between segments: a modest increase of 0.3% at company-operated units driven by a higher average check size (+2.1%) partially offset by lower transactions (-1.8%), while franchise-operated units showed flat comparable sales balancing a slight increase in transactions (+0.1%) against a small decrease in average check size (-0.1%) [S1].

These patterns indicate pricing power helped sustain revenue per visit but also reveal softness in customer frequency or traffic particularly within company-owned stores.

Liquidity Profile and Debt Structure Limit Financial Flexibility

At September 24, 2025, the Company had $61 million drawn under its $150 million senior secured revolving credit facility established July 27, 2022 [S4][F1]. Interest rates vary based on SOFR or base rate plus leverage-based margins ranging approximately from mid-5% to near-7%, depending on loan type and prevailing rates [S4][S9]. The Company remained compliant with all financial covenants including a lease-adjusted consolidated leverage ratio capped at about 4.25x as of mid-2025 [S4].

The current ratio stood at a low level of approximately 0.32 at December 31, 2025 reflecting current liabilities ($79 million) exceeding current assets ($25 million) which indicates tight working capital conditions [F1]. Despite this constraint, operating cash flow totaled roughly $48 million for fiscal 2025 supporting capital expenditures of $22.6 million focused on new restaurant development and remodeling initiatives [F1][S11].

Capital Allocation: Reduced Buybacks Amid Strategic Investments

Capital allocation shifted notably as share repurchases declined sharply to about $1.8 million during fiscal 2025 compared to $20+ million in prior years despite positive free cash flow estimated near $25 million (operating cash flow minus capex) [F1][S7][S10]. This reduction reflects liquidity management priorities amid debt service obligations.

Investments emphasized new restaurant openings—particularly franchised units—and store refresh projects aligned with evolving customer expectations and competitive positioning [F1][N2]. Dividend payments continue but are subject to restrictions under the revolving credit agreement limiting distributions when leverage thresholds are breached [S14]. Stock-based compensation programs remain active incentivizing executives via performance-based restricted stock units linked to revenue growth and contribution margin targets over multi-year vesting periods [S10][S14].

Brand Equity Supports Competitive Moat Amid Regional Concentration

Intangible assets related to franchise goodwill and trademarks represent significant components of El Pollo Loco’s asset base deriving from both acquisitions and organic growth within its core markets predominantly Southern California [F1][S16].

This brand equity underpins pricing power evidenced by average check increases despite competitive pressures while digital ordering platforms bolster customer engagement consistent with the Company’s "Digital First" strategic pillar described in regulatory filings [S1]. However, geographic concentration presents limits on rapid scale outside established regions.

Supplier Concentration Risk Remains Relevant Though Moderating

Historically dependent on one primary supplier accounting for nearly one-fifth of accounts payable balances, recent disclosures indicate diversification efforts have reduced supplier concentration below critical thresholds (<10%) as of late fiscal 2025 though vigilance remains warranted given potential supply chain disruptions or cost volatility impacts on margins [S16][S17][S21].

Outlook for Fiscal Year 2026: Focused Expansion and Sales Growth Initiatives

Management expects continued expansion primarily driven by franchising with three to four additional company-operated units planned mainly in California and Texas alongside fifteen to sixteen franchised openings nationwide [S1][N2]. Initiatives target increasing customer visit frequency, attracting new customers, and lifting per-person spending supported by marketing investments including enhanced loyalty programs leveraging digital platforms [N6][N2].

Recent analyst activity includes Benchmark’s upgrade citing improved operational execution while DA Davidson initiated coverage with a neutral stance reflecting cautious optimism balanced against macroeconomic uncertainties impacting discretionary spending trends [N6][N7]. Monitoring quarterly comparable sales trends alongside leverage metrics will be key indicators of sustained progress.

Disclaimer: This analysis is based solely on information available from cited SEC filings and public disclosures up to March 14, 2026 without extrapolations beyond those sources; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments