Copper Property CTL Trust’s Transition From Asset Stewardship to Liquidation

CPPTL’s journey from a restructured retail property holder to an imminent liquidation vehicle highlights concentrated risks and legal entanglements amid evolving market dynamics.

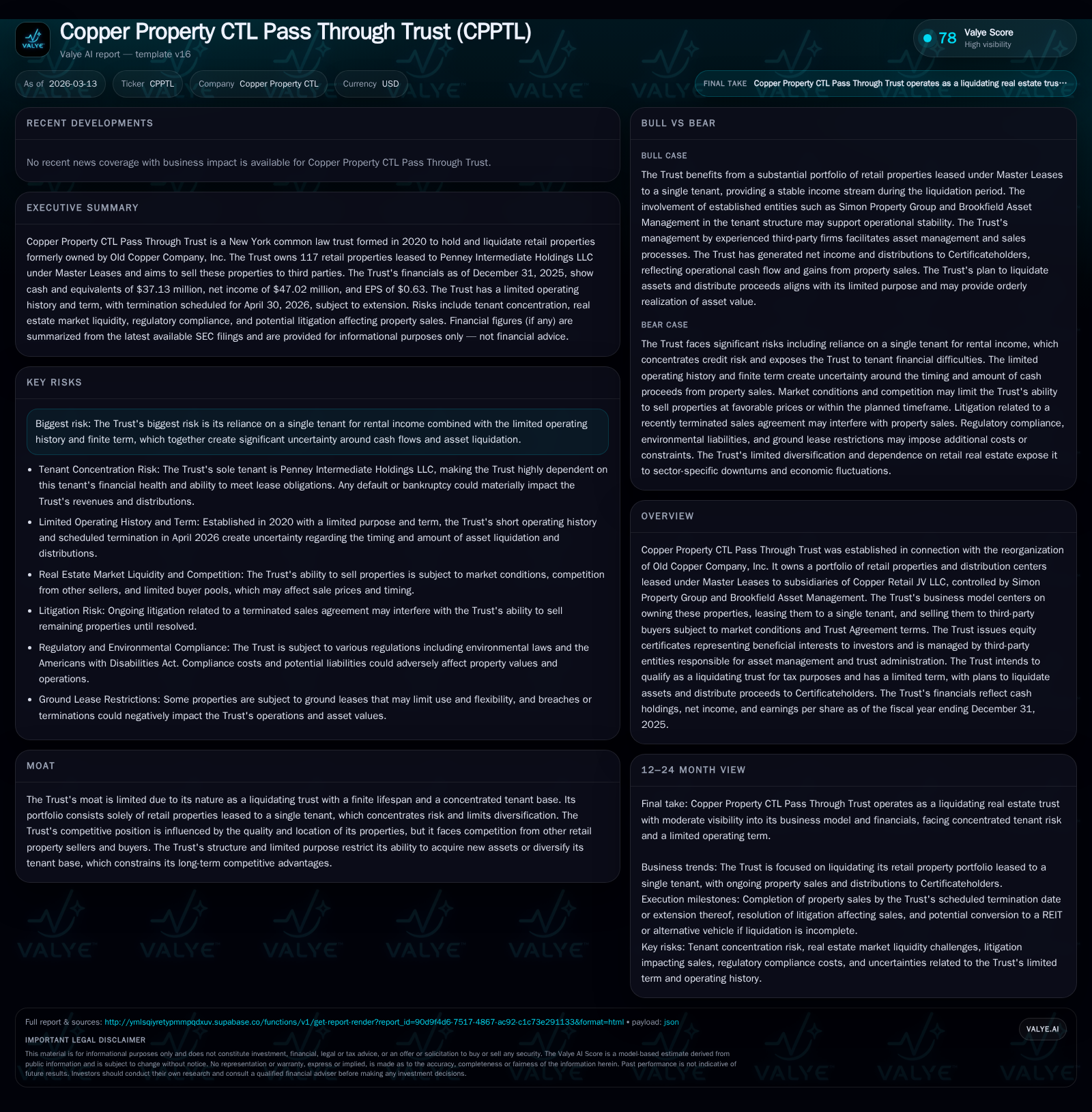

Established in 2021 from the Old Copper Company reorganization, Copper Property CTL Pass Through Trust holds a concentrated portfolio of retail properties leased solely to subsidiaries of Copper Retail JV LLC. The Trust’s limited-life mandate confines operations to asset stewardship and liquidation, navigating substantial single tenant concentration risk and ongoing litigation that materially influence asset sale timing and distribution flows. Financials reveal declining net income and equity amid steady cash flows, with distributions reliant on property sales proceeds. The Trust faces headwinds from restricted governance under its Trust Agreement and strained market conditions for retail assets, complicating its path to orderly wind-down.

Formation Origins and Portfolio Composition of CPPTL

Copper Property CTL Pass Through Trust (the "Trust") was established on December 12, 2020, in connection with Old Copper Company, Inc.'s Chapter 11 reorganization finalized in January 2021 [S1][S12]. The Trust acquired from Old Copper a portfolio composed of approximately 160 retail properties plus six distribution centers across the United States—including Puerto Rico—with about 15.5 million square feet under lease. These real estate assets are held via separate wholly-owned property holding companies known as PropCos.

All properties are leased exclusively under two Master Leases to subsidiaries of Copper Retail JV LLC ("OpCo Purchaser" or "Penney Intermediate Holdings LLC"), a joint venture controlled by Simon Property Group and Brookfield Asset Management [S1][S9]. The Trust's operations are strictly limited: it collects rent under these Master Leases, administers the properties through third-party service providers (GLAS Trust Company as Trustee; Hilco JCP LLC as Manager), and disposes of assets subject to market conditions per the Trust Agreement [S8][S12]. This structure precludes acquisition of new assets or tenant diversification [S1], inherently concentrating operational risk.

Financial Performance Trends: Earnings Volatility and Cash Flow Analysis

The Trust has a short operating history starting in fiscal year 2021 with financials available through FY2025 showing notable earnings volatility reflective of its liquidating nature and sale-dependent revenue component [F1]. Net income dropped from USD 73.8 million in FY2024 to USD 47.0 million in FY2025—a sharp decline of approximately 36.3%. Operating cash flow also contracted by roughly 14% during this period but remained comparatively stable relative to net income fluctuations (USD 79.3 million CFO in FY2025) [F1]. Equity declined steadily each year from USD 1.15 billion in FY2022 to USD 933 million by FY2025 as asset sales and distributions reduced net assets.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 47 | 79 | -36.3% |

| 2024 | 74 | 92 | +6.7% |

| 2023 | 69 | 92 | -21.0% |

| 2022 | 88 | 89 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 5.0 |

| 2024 | 7.3 |

| 2023 | 6.3 |

| 2022 | 7.6 |

Source: SEC companyfacts cache [F1].

All figures in USD millions except ROE (%) [F1]

Decreased net income partly reflects gain recognition timing on property sales; during FY2025 four Retail Properties were sold garnering proceeds of about USD 32 million with recognized gains near USD 4.27 million [S12]. Distributions paid to Certificateholders totaled approximately USD 128 million for FY2025 inclusive of proceeds from prior sales but excluding post-year-end sales proceeds distributed subsequently [S12]. Despite earnings declines, robust operating cash flows support continued distributions albeit declining as remaining asset base shrinks.

Tenant Concentration Risk: Implications of Master Lease Structure

The entire revenue stream emanates from leasing all the Properties exclusively to Penney Intermediate Holdings LLC subsidiaries under two unified Master Leases [S9]. This "single tenant concentration" creates pronounced operational risk because all rental payments hinge upon one entity's financial health and retail performance.

Moreover, these Master Leases are triple-net leases requiring the Tenant not only to pay rent but also all costs related to insurance, taxes, utilities, maintenance, indemnifications etc., effectively minimizing the Trust's direct operating expenses while shifting considerable risk onto the Tenant [S13][S20].

From an exit perspective, buyer interest is hindered because properties are encumbered by "leasehold rights" limiting purchaser appeal relative to free-and-clear ownership options [S23]. Such leasehold encumbrances restrict buyers’ flexibility with these assets compared to other commercial retail real estate offerings absent similar restrictions.

Additionally, should the Tenant or Lease Guarantors become insolvent or bankrupt—a credible scenario given economic pressures on physical retail—the entire Master Lease could be rejected en bloc under bankruptcy law statutes leaving the Trust exposed both to rental income losses and costly re-leasing challenges at potentially lower rates with significant break-even remediation expenses [S9][S13][S20].

Litigation and Contractual Challenges Impacting Asset Sales Timing

Throughout late fiscal year 2025 into early calendar year 2026, litigation disruptions materially affected planned asset dispositions [S4][S5]. The Trust terminated a sale agreement on December 26, 2025; prior thereto, the prospective buyer sued for specific performance alleging breach of contract [S5]. The Trust maintains these suits lack merit but acknowledges ongoing legal proceedings divert management focus and incur substantial legal expenses.

A persistent pro se plaintiff Eric L. Moore has initiated multiple lawsuits related tangentially or directly stemming from legacy J.C. Penney bankruptcy issues; while most claims against the Trust were dismissed with prejudice, Moore continues active litigation seeking receivership over sale proceeds tied to pending transactions [S5]. These entanglements add procedural complexities that may delay further property sales until judicial resolutions are attained.

Management opines that current pending litigation will not impose material adverse effects on long-term business continuity but concedes that unforeseen outcomes remain possible with attendant financial impacts [S4][S5]. Legal costs are expensed immediately thus reducing distributable earnings.

Trust Agreement Constraints and Impacts on Certificateholders’ Rights

The structural framework underpinning CPPTL is unique due to its status as a liquidating trust formed post-bankruptcy with finite duration objectives [S1][S15]. Certificateholders own undivided beneficial interests via issued trust certificates but possess very limited control or approval rights over day-to-day management or strategic decisions beyond specified majority votes.

Critically, the Trust Agreement limits Certificateholder actions such as instituting lawsuits absent consent thresholds; pre-dispute jury trial waivers constrain legal recourse modalities potentially diminishing plaintiff leverage in disputes arising under federal securities laws [S6][S15].

Indemnification clauses protect the Trustee and Manager barring gross negligence or willful misconduct yet shift potential liability costs onto the Trust itself which can erode trust certificate values if invoked excessively [S7]. Overall governance rights tilt substantially toward Trusteeship entities rather than Certificateholder empowerment creating risk asymmetry that participants must accept given the setup’s liquidation-oriented purpose.

Capital Allocation: Distribution Policies, Cash Reserves, and ROE Insights

Capital returned largely stems from monetization proceeds following disposal of Properties subject to contractual approval mechanics mandated by certificateholder votes per the Trust Agreement [S12][F1]. In FY2025 alone distributions aggregated USD ~128 million supported mainly by realized sale gains alongside ongoing rental revenues underwriting operating expenses and residual cash generation.

Cash & equivalents at fiscal year-end equaled roughly USD 37 million providing liquidity buffer for administrative costs including trustee/manager fees and impending legal costs which have been non-trivial amid active litigation challenges [F1][S23].

Approximate trailing return on equity declined progressively reaching near five percent for FY2025 reflective of shrinkage in equity base combined with net income volatility linked directly to transactional timing effects rather than recurring operating profits [F1]. Given fixed life mandate focused on wind-down versus growth this pattern aligns logically with expected capital attrition trajectory.

Forecasting Liquidation Outcomes: Market Conditions and Strategic Considerations (Analysis)

Retail commercial real estate currently faces persistent headwinds including illiquidity exacerbated by niche buyer pools constrained by master lease terms that reduce speculative acquisition incentives [S23]. Elevated cap rates driven by sustained interest rates following multi-year monetary tightening have depressed valuation multiples for such assets versus historic norms.

Although Federal Reserve has lowered policy rates recently with potential additional cuts anticipated in near term [S20], uncertainty looms whether market confidence will restore quickly enough before mandated termination date April 30, 2026 forcing potentially suboptimal pricing or delayed disposition schedules.

If asset sales cannot be executed expediently within approved sale periods—even if extended per certificateholder vote—the Manager envisions transferring remaining assets into a Real Estate Investment Trust (REIT) structure or functional equivalent as an alternative means for value extraction albeit sacrificing timing certainty due to additional regulatory compliance and governance overheads negatively impacting distributions post-transfer [S14][S26].

What Investors Should Monitor Moving Forward (Forward-looking analysis)

Certificateholders should prioritize tracking developments including:

- Resolution status of ongoing litigation particularly regarding terminated sales agreements which materially affect liquidity event timelines.

- Negotiation progress on substitute sale arrangements mitigating recent deal breakdown effects.

- Operational health indicators for sole tenant Penney Intermediate Holdings LLC affecting rent collection reliability amidst retail sector challenges.

- Updated announcements concerning distribution amounts/timing reflecting new asset sale receipts or unexpected expenses.

- Regulatory filings disclosing material changes pertaining to trust extension decisions beyond April 30, 2026 or plans for conversion into REIT/alternative vehicles affecting financial forecasts materially.

The finite life nature alongside concentrated counterparty exposure demands vigilance given risks amplified relative to diversified real estate investment vehicles.

This analysis synthesizes publicly filed information through March 13, 2026 without extrapolating beyond documented facts or issuing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments