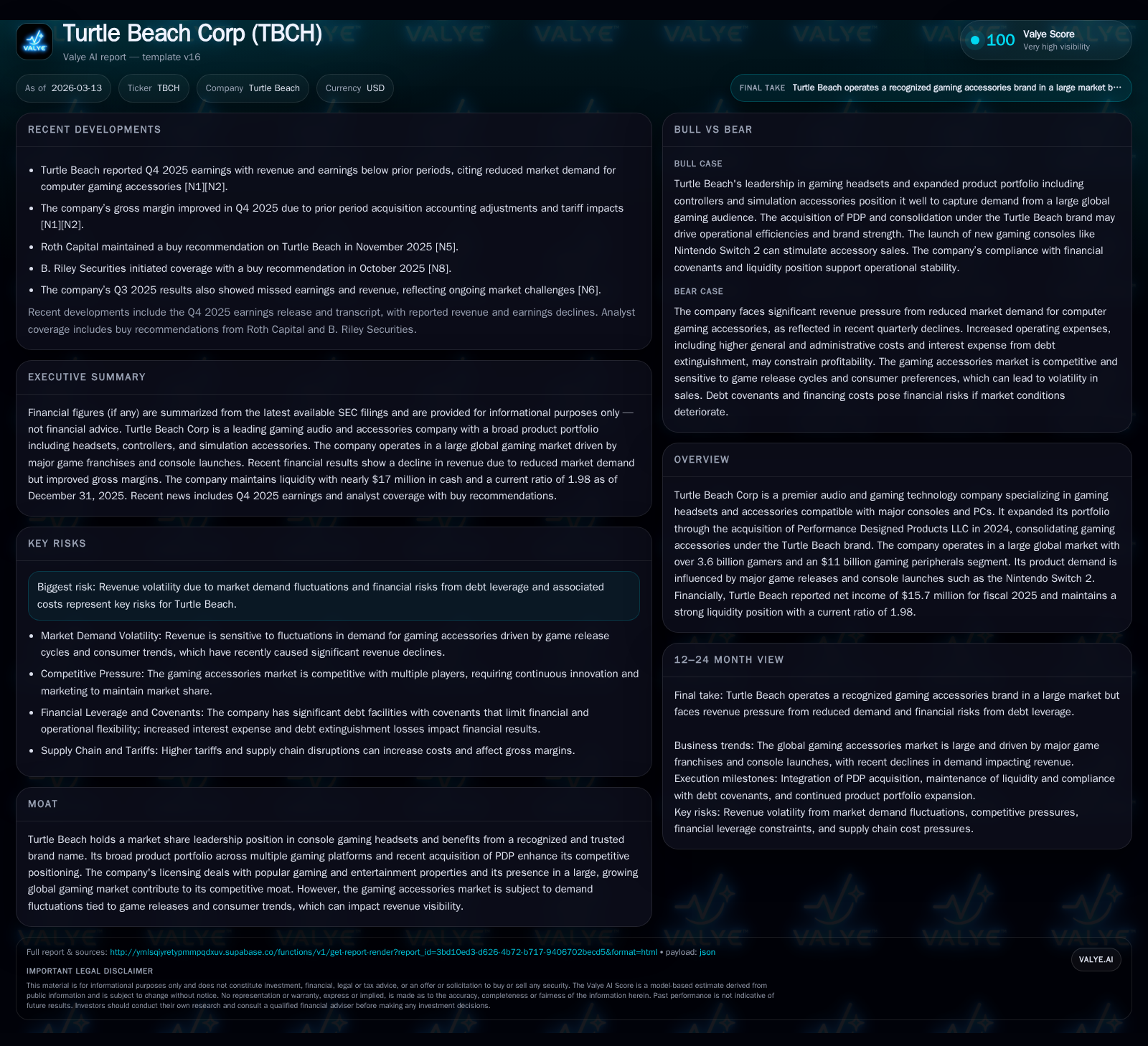

Turtle Beach’s Turnaround: Revenues Spike and Strategic Brand Consolidation Underpin Market Leads

Turtle Beach leverages its 2024 PDP acquisition and gaming market dynamics to reverse prior losses and solidify leadership in console headsets.

After years of volatility marked by steep losses, Turtle Beach has posted a decisive financial turnaround, driven largely by the strategic acquisition of Performance Designed Products LLC (PDP) in 2024. This move expanded its product portfolio across multiplatform gaming accessories, helping the company capitalize on a robust global gaming peripherals market valued at $11 billion. Despite revenue pressures from variable consumer demand, Turtle Beach's improved operating income and net income, supported by strong cash flow generation and solid liquidity, underscore a reinforced competitive position centered on console headset market share leadership.

Historic Performance: From Losses to Operating Profitability

Turtle Beach Corp has exhibited a remarkable financial transformation over recent years. In fiscal 2022, the company recorded a severe operating loss of -$51.5 million compounded by a net loss of approximately -$23.2 million, reflecting significant challenges before the PDP acquisition [F1]. However, subsequent periods demonstrated steady recovery; operating income swung positive to over $20 million in 2024 and further rose to $27.5 million by the end of fiscal 2025, corresponding with an almost stable net income around $15.7 million that year [F1].

This substantial rebound aligns with improved operational management and revenue scaling through expanded product offerings post-acquisition. Operating cash flow also reflected this improvement, surging from negative $41.8 million in 2022 to positive $35.5 million by fiscal 2025—a fivefold gain underpinning cash conversion strength.

Capital expenditures declined sharply by over 70% between 2024 and 2025 from around $4.9 million down to just under $1.42 million, signaling tighter capex discipline in line with maturity post-integration phases [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 16 | 35 | 28 | 1 | -2.8% |

| 2024 | 16 | 6 | 20 | 5 | +89.2% |

| 2023 | 9 | 27 | -16 | 2 | +136.8% |

| 2022 | -23 | -42 | -51 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 19 | 34 | 12.2 |

| 2024 | 28 | 1 | 13.4 |

| 2023 | 1 | 25 | 10.1 |

| 2022 | 5 | -45 | -26.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue values for these years were not explicitly provided in detailed YoY terms; focus remained on profitability and cash flows.

Acquisition of PDP: Strategic Consolidation and Portfolio Expansion

March 2024 marked a pivotal inflection for Turtle Beach through its acquisition of Performance Designed Products LLC (PDP), another prominent name in gaming accessories bearing licensing deals with major entertainment IPs [N1][S2][S14]. This transaction infused Turtle Beach’s portfolio with controllers/gamepads across all platforms along with a broader slate of accessories—from microphones to flight and racing simulation gear—thus diversifying away from their core headset lineup.

Post-acquisition integration led to the consolidation of all gaming accessory products under Turtle Beach's flagship brand rather than maintaining multiple separate banners—streamlining market recognition and leveraging their trusted brand name [N1]. PDP’s contribution expanded the product ecosystem notably on multiplatform compatibility spanning Xbox, PlayStation, Nintendo Switch, PC, tablets, and mobile devices.

This bolstered Turtle Beach’s moat by increasing peripheral SKU expansions relative to platform compatibility requirements while capitalizing on leveraged licensing relationships within influential gaming franchises.

Revenue Drivers and Market Position in Console Gaming Headsets

Console gaming headsets underpin Turtle Beach’s revenue dominance as the recognized market leader leveraging franchise licensing power combined with effective platform compatibility coverage [F1][N1][S1]. The global gaming peripherals segment is sizable—about an $11 billion market—and highly influenced by attach rates tied directly to high-profile game releases such as Call of Duty titles or online multiplayer titles requiring reliable voice communication.

The launch of Nintendo Switch 2 in June 2025 triggered a notable uplift; it emerged as the fastest-selling new game console launch ever in the U.S., promising potential for increased peripheral demand during early lifecycle phases considering gamers’ propensity to upgrade headsets or controllers contemporaneously [N1][S26]. This type of hardware debut interacts synergistically with major game launches which naturally prompt consumers towards premium accessories enabling immersive audio experiences or competitive advantages.

While headsets remain central revenue engines for Turtle Beach, their broadened lineup post-PDP introduces incremental growth opportunities via cross-platform controllers and specialized niche products like racing simulation hardware that cater to dedicated sub-segments within PC/console enthusiasts.

Future Growth Outlook: Risks and Opportunities in Gaming Accessories Demand

Looking ahead, Turtle Beach's future growth will oscillate primarily according to market demand cycles typically shaped by blockbuster game releases alongside console generation refresh events—both seasonally clustered stimuli for accessory attach rate spikes [N1][S11][S16]. The company’s management cautions regarding inherent revenue volatility stemming from these cyclic dependencies.

Additionally, shifts in consumer preferences toward integrated wireless audio solutions or competition with alternative peripheral manufacturers could moderate expansion prospects or intensify pricing pressure—factors that underscore operational vulnerability despite brand strength.

Debt leverage introduces further constraints; amid recent financings Turtle Beach entered into agreements restricting excess leverage ratios and covenants governing dividend payouts or additional borrowings [S11][S16]. Although amended credit arrangements now afford some leeway on restricted payments through mid-2026 [S23], potential financial rigidity due to interest burdens impacts strategic investment flexibility.

Forecast Indicators and Milestones from Recent Earnings Commentary

Explicit formal guidance remains sparse; however, management signals several key milestones investors should monitor:

- Depth of PDP integration across sales channels and SKU rationalization efficiencies.

- Quarterly attach rates coinciding with arrivals of new game editions or console platform expansions such as supplemental Switch model sales or next-gen updates.

- Effectiveness of marketing spend calibrations amidst fluctuating demand levels impacting selling expenses.

- Progress on deleveraging initiatives targeting leverage ratio improvements per Credit Agreement stipulations. These indicators emanate primarily from Q4 earnings commentary and company filings through early March 2026 [N1][N2][S3].

Balance Sheet Strength and Capital Allocation Strategy

As of December 31, 2025, Turtle Beach maintained a solid liquidity profile highlighted by a current ratio near two (1.98), signifying balanced short-term asset coverage relative to liabilities [F1]. Available revolving credit approximated $34.5 million at September-end after incorporating PDP assets into borrowing base calculations under the Bank of America facility amendments executed March 2024 [S4][S5].

The company retired its Blue Torch term loan facility early in August 2025 using new bank financing structured under a Credit Agreement maturing August 2028 encompassing both revolving ($90M capacity) and term loans ($60M capacity) facilities subject to financial covenants including fixed charge coverage ratios near one-to-one minimums [S6][S8][S9].

Notably, late December amendments relaxed fixed charge coverage ratio calculations regarding restricted payments up to $10 million within consecutive quarters ending March and June 2026—potentially facilitating capital returns or reinvestment flexibility depending on operational cash flows [S23][S24].

Cash Generation, Return on Equity, and Shareholder Returns

Operating cash flow dynamics demonstrate dramatic improvement: from a negative -$41.8 million mark during fiscal year ending in December 2022 moving sharply into positive territory at nearly $35.5 million at fiscal year-end December 31, 2025—a more than fivefold increase year-over-year when comparing fiscal ’24 to ’25 performance per SEC filings [F1]. After accounting for reduced capital expenditures (~$1.42 million in FY25), free cash flow emerges close to $34 million indicating healthy internal funding capacity.

Return on equity (ROE), calculated as net income against average shareholders’ equity base (~$128 million at FY25 end), stands at an approximate level of 12%, illustrating enhanced capital deployment efficiency following the transformational acquisition period [F1].

Capital allocation priorities have balanced reinvestment needs against shareholder distributions: buybacks totaled approximately $19 million during FY25 while dividend payments persisted consistently per periodic disclosures providing signal on management’s confidence levels when balanced against debt servicing demands [F1][S28][S29].

This report is based solely on information provided through March 13, 2026 including SEC filings and company-released statements without extrapolation beyond stated facts or predictive investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments