Deutsche Bank’s Revenue Plateau and Emerging Market Push

After nearly flat revenue in 2025, Deutsche Bank intensifies its private banking expansion in emerging markets to drive future growth.

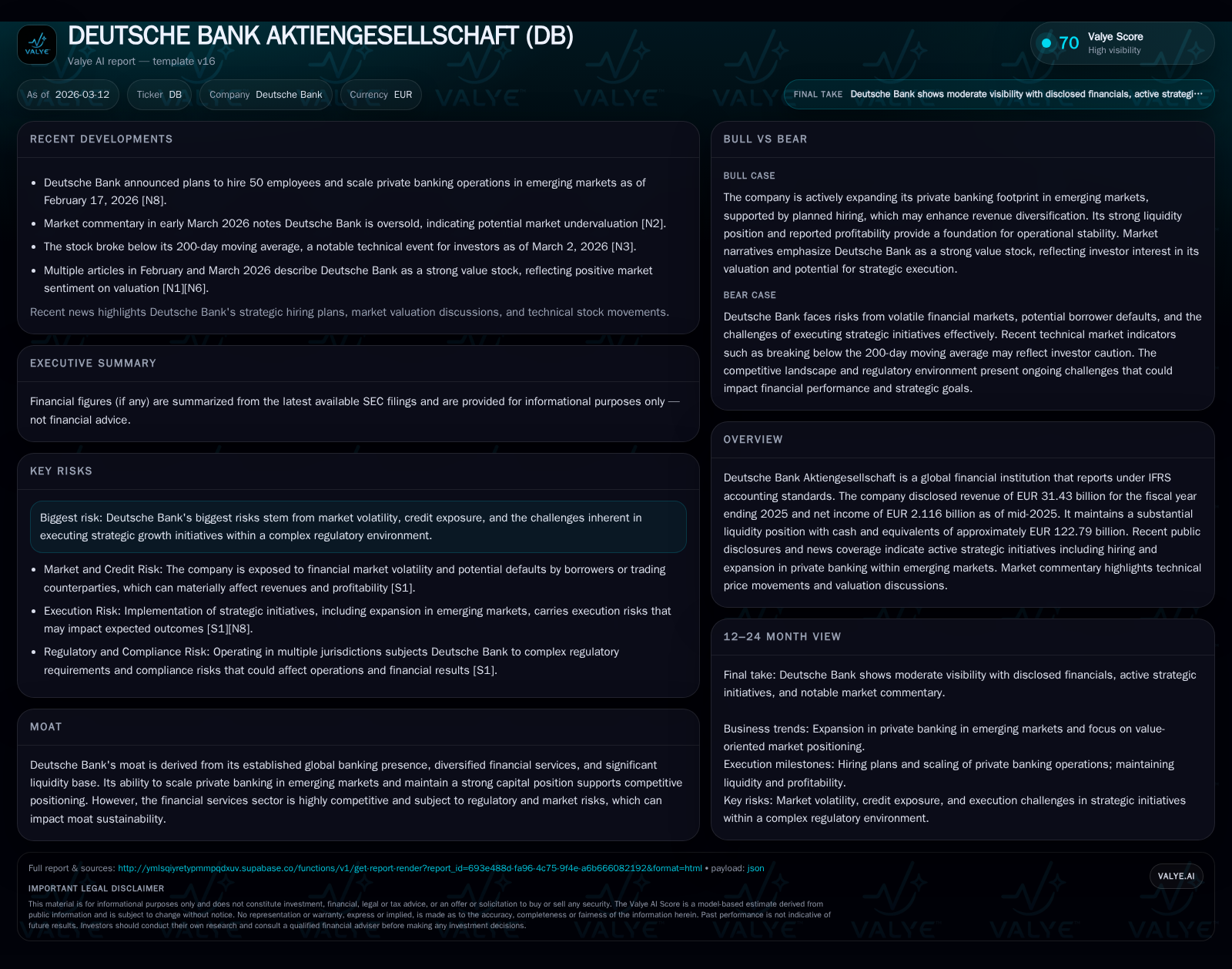

Deutsche Bank reported a marginal 0.2% decline in revenue for fiscal year 2025, contrasting with a robust 16.2% increase in net income, reflecting enhanced operational efficiency and risk-weighted asset management. Leveraging a substantial liquidity position of approximately EUR 123 billion, the bank is scaling private banking through strategic hires focused on emerging markets, aiming to capitalize on higher-growth geographies. Despite a strong capital base sustaining competitive positioning, regulatory complexities and market volatility remain key challenges.

Revenue and Profit Trends: A Mixed 2025 Performance

For the fiscal year ending December 31, 2025, Deutsche Bank's reported revenue was EUR 31.43 billion, marking a slight decrease of approximately -0.2% compared with EUR 31.50 billion in the prior year [F1]. This top-line plateau reflects challenging revenue environments across its diversified financial services portfolio amid lingering geopolitical uncertainties and moderating global trade dynamics as detailed in the company's MD&A [S1]. Contrasting the stagnant revenue trend, net income showed a strong historical increase of about 16.2%, reaching EUR 6.45 billion in the prior full year ending December 31, 2023 [F1]. This improvement underscores enhanced operational leverage and disciplined cost containment efforts articulated during analyst presentations [S3]. The bank employs treasury management practices including fair value hedge accounting under the EU carve-out to reduce earnings volatility related to interest rate fluctuations [S3].

Private Banking Expansion: Scaling in Emerging Markets

Strategically, Deutsche Bank is directing growth initiatives towards expanding its private banking segment within emerging markets by recruiting around 50 new specialists focused on these geographies [N10][N2]. Given that emerging market economies grew an estimated 4.4% in 2025 despite external trade shocks [S1], this approach aims to capture expanding high-net-worth client bases supported by improving macroeconomic conditions and lower inflation-driven rate cuts allowing more discretionary wealth allocation [S1]. The bank's sizable liquidity provides critical firepower to fund this expansion organically while competing effectively amid complex client segmentation and regulatory requirements specific to cross-border wealth management [N10][S1]. Competitive forces within private banking are intensifying; success hinges on localizing service offerings while maintaining compliance robustness especially given shifting U.S.-Europe capital rules governing foreign banking operations (FBOs) [S4].

Liquidity Fortitude and Capital Management

Deutsche Bank maintains one of the industry’s largest liquidity cushions, reporting cash and cash equivalents approximating EUR 122.79 billion as of June 30, 2025 [F1], which supports resilience against market stress episodes and strategic flexibility for organic initiatives or M&A [S5][S6]. This ample liquidity underpins compliance with Basel III/IV capital ratios and leverage ratio requirements particularly relevant given the bank’s dual structure with U.S.-based intermediate holding companies (IHCs) like DB USA Corporation mandated by Federal Reserve regulations [S1][S5]. Such frameworks impose strict buffers that influence capital preservation priorities sometimes at the expense of aggressive risk asset expansion, shaping Deutsche Bank's strategy to balance growth aspirations with regulatory discipline.

Competitive Environment and Regulatory Risks

Externally Deutsche Bank operates amid persistent geopolitical headwinds including tensions from Ukraine conflict spillovers and Middle Eastern uncertainties that affect market volatility and macroeconomic forecasts [S1][S4]. Additionally, specific U.S. trade policies contribute to intermittently volatile trading revenues derived from key markets [S1]. Regulatory scrutiny especially over U.S. subsidiaries via intermediate holding company mandates poses complexities that press the bank toward conservative capital strategies limiting aggressive profit growth attempts [S4][N10]. Credit exposure concerns remain material risks given potential defaults especially in stressed sectors of Germany’s largely stagnant economic environment where GDP barely grew by +0.2% in 2025 [S1]. Accordingly, Deutsche Bank’s risk management posture integrates these factors into conservative provisioning while navigating competitive moves by global peers.

Analyzing Return on Equity and Capital Allocation Patterns

With net income of EUR 6.45 billion for FY2023 against total shareholders' equity reported at approximately EUR 82.29 billion for FY2025 [F1], Deutsche Bank’s post-tax return on equity stands near a moderate yet improving figure at roughly 7.8%. This suggests measured profitability gains without excessive leverage or risk-taking [F1][S23]. Dividend distributions remain aligned with regulatory constraints ensuring sustainable payout ratios; meanwhile share repurchase data post-2025 is less clearly defined though past filings imply cautious buyback activity supportive of shareholder returns without compromising capital buffers [S12][S17][S23]. Such patterns reflect a strategic stance prioritizing capital preservation amid ongoing transformation rather than rapid payout escalation.

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 31.4 | -0.2% | ||

| 2024 | 31.5 | +1.1% | ||

| 2023 | 31.2 | 6.5 | +15.1% | +16.2% |

| 2022 | 27.1 | 5.6 | +114.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | |

| 2024 | |

| 2023 | 8.5 |

| 2022 | 7.7 |

Source: SEC companyfacts cache [F1].

What to Watch: Strategic Milestones and Market Sentiment

Looking ahead, critical indicators include quarterly revenue trends which could signal successful accrual of emerging market private banking clients following the initial hiring surge reported early in 2026 [N10]. Additionally, close monitoring of Deutsche Bank stock technical levels is warranted as recent price dips below the crucial 200-day moving average have intensified valuation discussions within investment circles highlighting divergence between underlying fundamentals versus market perception [N4][N5][N2]. Market sentiment will likely be shaped also by evolving trade policies impacting global banking flows alongside regulatory developments affecting U.S.-Europe cross-border banking operations that may alter risk appetites further.

This analysis synthesizes Deutsche Bank's latest publicly available financial data alongside strategic disclosures up to March 2026 without extrapolating beyond documented facts or guidance provided by official filings or news reports. It emphasizes contextual clarity over speculation respecting the complexity inherent in international banking operations subject to multi-jurisdictional oversight.

Disclaimer: This report provides an analytical overview for informational purposes only based on selected data sources without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments