Pixelworks' Strategic Pivot to Cinematic Visualization Highlights Growth Challenges and Resource Constraints

Following the divestiture of its semiconductor business, Pixelworks now concentrates solely on its TrueCut Motion cinematic platform amid revenue contraction and operational losses.

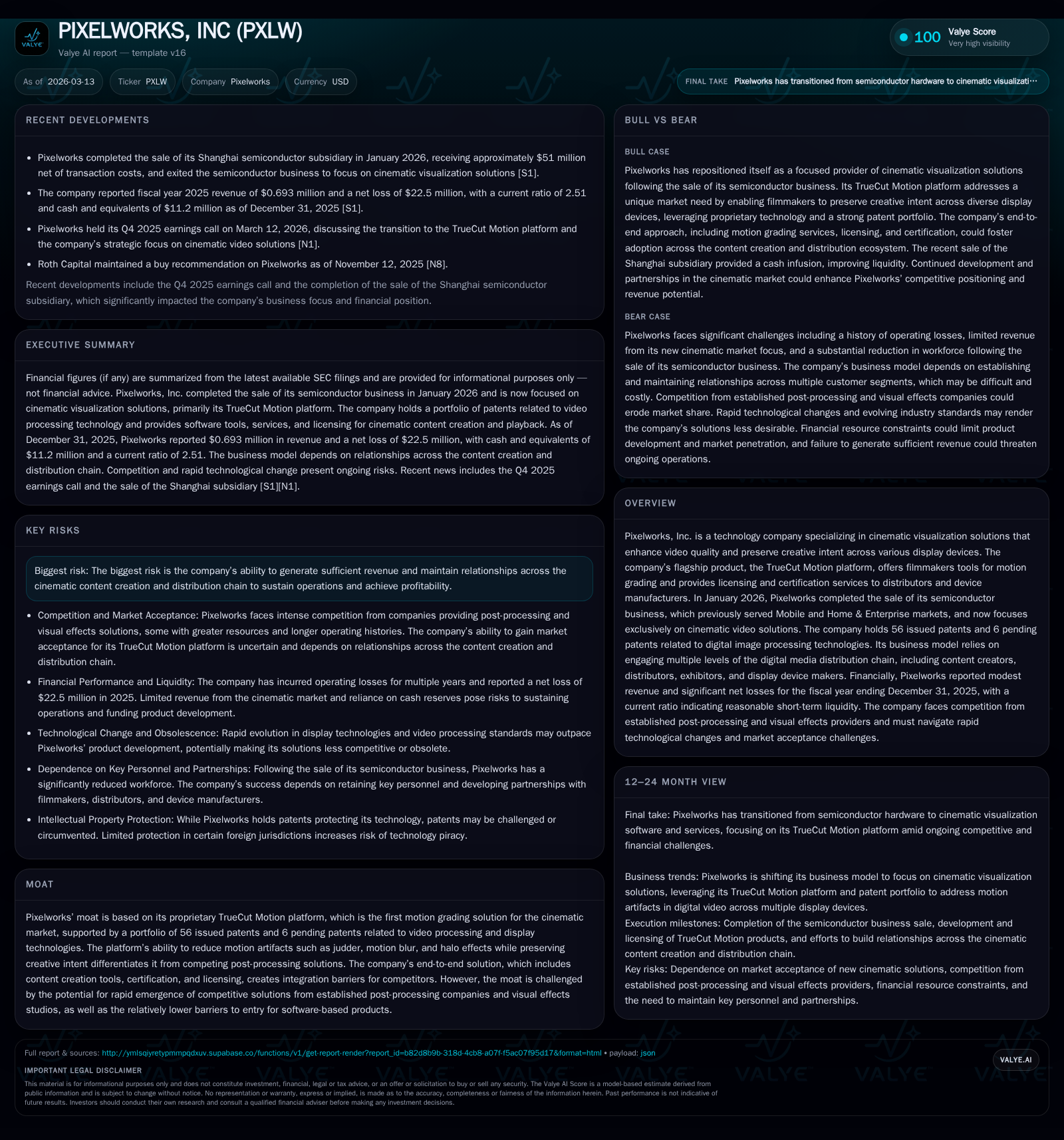

Pixelworks, Inc. completed a significant corporate transition in early 2026, selling its semiconductor segment to focus exclusively on cinematic visualization solutions embodied by its patented TrueCut Motion platform. This strategic pivot has precipitated a sharp decline in reported revenues—from $43.2 million in 2024 to $0.7 million in 2025—reflecting the shift away from legacy businesses rather than organic core growth contraction. Despite advances in proprietary motion grading technology and a well-defined IP moat with 56 patents, the company faces substantial challenges including intense competition, market adoption risks, and persistent operating losses that have exceeded $11 million in 2025 alone. Capital allocation remains tight with negative free cash flow exceeding $21 million annually post-sale, and shareholder equity turning negative by the end of 2025. The future trajectory of Pixelworks hinges on successfully expanding licensing and service engagements across the cinematic content chain, navigating evolving technology trends, and managing resource limitations inherent to its smaller scale.

Company Background and Recent Structural Shift

Founded in 1997 and headquartered in Oregon, Pixelworks has historically delivered innovations in video processing across consumer electronics and professional display sectors. The company developed extensive IP and products spanning semiconductor chips for mobile devices and home entertainment applications as well as software-based visualization technologies.

On January 6, 2026, Pixelworks completed the sale of all shares of its semiconductor subsidiary Pixelworks Semiconductor Technology (Shanghai) Co., Ltd., transitioning fully into cinematic visualization solutions with its flagship TrueCut Motion platform [S1][S18][S27]. This marked a decisive strategic pivot away from hardware manufacturing toward software-enabled content creation tools, certification services, licensing agreements for distributors (studios/exhibitors/streaming platforms), and device manufacturers.

Historical Financial Performance

Pixelworks' financials exhibited pronounced flux due to this transition:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1 | -22 | -21 | -12 | -98.4% | +21.7% |

| 2024 | 43 | -29 | -20 | -31 | -27.6% | -9.7% |

| 2023 | 60 | -26 | -19 | -29 | +253.4% | -1253.5% |

| 2022 | 17 | -2 | -13 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | 106.7 |

| 2024 | -24 | 271.8 |

| 2023 | -23 | -208.7 |

| 2022 | -14 | -6.0 |

Source: SEC companyfacts cache [F1].

The stark revenue decline in FY2025 primarily reflects the discontinuation of semiconductor product lines post-sale; minimal revenues remain from TrueCut Motion which registered as non-material previously [F1][S14][S27]. Operating income improved fractionally from large prior-period losses but continues at a substantial deficit.

Business Model: Focus on TrueCut Motion Platform

The TrueCut Motion platform is centered on proprietary MotionEngine® algorithms enhancing cinematic video presentation through motion grading — enabling filmmakers to assert creative control over motion blur, judder, frame rate appearance — solved via patented techniques that reduce visual artifacts like halos which plague conventional MEMC implementations [S9][S14].

The technology extends across a pipeline involving:

- Content creators (filmmakers licensing or using Pixelworks’ tools)

- Distributors (studios and streaming services licensing certified content delivery technologies)

- Exhibitors including theaters and home device manufacturers (participating via certification programs ensuring playback fidelity)

This end-to-end engagement model creates integration barriers yet requires maintaining robust relationships at each level for steady revenue flows [S9][S14][S28].

Competitive Positioning and Risks

Pixelworks claims first-mover advantage with TrueCut Motion in the cinematic motion grading niche supported by an intellectual property portfolio of 56 issued patents with remaining terms ranging from one to sixteen years plus six pending applications covering motion estimation/motion compensation techniques crucial to its product differentiation [S5][S17].

However, competition intensifies from large incumbents such as Dolby Laboratories as well as software developers like Epic Games, Adobe, Unity Technologies, and visual effects studios including ILM and Pixar which employ pre-emptive artifact reduction methods during production rather than post-processing after-the-fact [S8][S16]. The lower barrier for software-centric solutions heightens vulnerability to rapid competitive innovation.

Additional risks highlighted include:

- Ongoing operating losses since FY2022 culminating in recurring deficits impacting shareholder equity negatively [F1]

- Reduced workforce concentration (~23 employees post-sale vs nearly 200 before), constraining development capacity [S17]

- Dependence on successfully monetizing across multiple ecosystem tiers simultaneously; failure at any point threatens revenue sustainability [S9][S14]

- Limited financial resources relative to competing firms which may impede rapid product rollout or marketing investment needed for broader adoption [S15]

- Potential intellectual property infringement litigation exposing Pixelworks to costly disputes or costly licensing arrangements adversely impacting margins or business continuity [S10][S11]

- Exposure to cybersecurity risks affecting operational systems mentioned among broader regulatory concerns [S4][S20]

Capital Allocation and Liquidity Position

Post-divestiture cash balance stood at approximately $11 million by end-2025 while current assets totaled about $50 million against current liabilities near $20 million yielding a healthy current ratio around 2.5x indicating short-term liquidity cushion exists despite negative equity reflecting accumulated losses [F1].

Nevertheless, free cash flow remains structurally negative around minus $21 million after subtracting capex which itself dropped sharply owing to transition away from manufacturing towards IP-driven services [F1].

No dividends were declared nor share repurchases disclosed during this period signaling reinvestment priority given ongoing loss-making operations; future capital raises or partnerships may be required to sustain R&D and sales rollout efforts absent near-term profitability improvements or sustained licensing revenues [F1][S24].

Future Growth Prospects and Key Milestones To Watch

Explicit forward guidance appears absent from filings or recent disclosures pointing instead toward milestones such as:

- Broadening filmmaker adoption of TrueCut Motion content creation licenses or services,

- Securing distribution agreements embedding certified technology,

- Expansion of device certification contracts with consumer electronics manufacturers,

- Development partnerships targeting improved algorithmic capabilities particularly aligned with emerging industry trends such as AI-enhanced visual processing,

- Execution efficiency achieving scalable content grading throughput balancing cost controls,

- Ongoing patent filings reinforcing technological moat,

- Monitoring competitive entrants’ moves especially concerning integrated VFX workflows.

The trajectory will be heavily influenced by whether Pixelworks can leverage their IP portfolio into meaningful recurring licensing streams across these segments while controlling overheads amidst limited scale [N1]; otherwise operational discontinuities or shareholder dilution pressures could accelerate [F1][S26].

Conclusion

Pixelworks stands at a crossroads following a major business model transformation culminating in the sale of its semiconductor business early this year. The reoriented focus on its proprietary TrueCut Motion cinematic visualization platform places it squarely within a niche yet dynamic video content ecosystem where technological innovation is critical but financial endurance remains uncertain.

The company’s key challenges rest on scaling revenue in a fragmented multi-stakeholder market while contending with financially stronger competitors bringing alternative technology approaches that may erode pricing power or market share over time.

Capital structure indicates constrained resources requiring prudent spending prioritizing product innovation alongside strategic customer engagements that must demonstrate revenue viability soon if Pixelworks is to sustain independent operations without reliance on further capital infusions.

Stakeholders should monitor upcoming partnership announcements, technological milestones surrounding new licenses or certifications gained, patent developments, and changes in operating cash flows as key barometers summarizing whether Pixelworks’ promising IP can translate into stable commercial returns amidst challenging market realities.

This analysis is based solely on documented facts and public disclosures available as of March 13, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments