COCA-COLA EUROPACIFIC PARTNERS Posts Moderate Revenue Growth and Strong Profit Increase Supported by EUR 1 Billion Buyback

CCEP’s FY2025 results highlight steady top-line expansion alongside significant capital returned through an active share repurchase program.

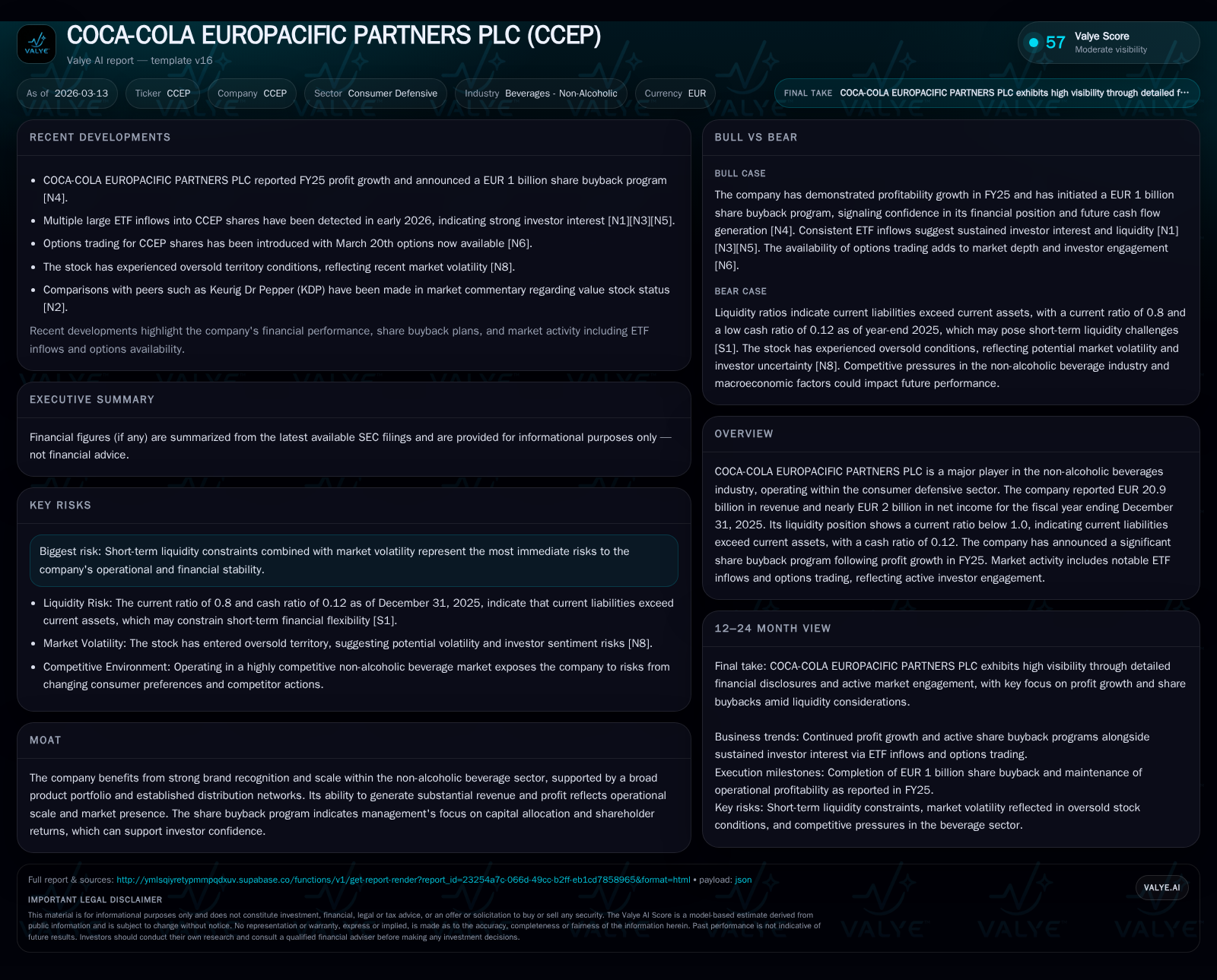

Coca-Cola Europacific Partners PLC delivered €20.9 billion in revenue for fiscal year 2025, a 2.3% increase from 2024, driven by volume gains and pricing strategies in Europe and Asia Pacific. Net income rose sharply by 37% to €1.98 billion, reflecting operational efficiencies and margin management amidst cost pressures. The company’s liquidity shows a current ratio below 1, underlining short-term obligations slightly exceeding current assets. Notably, CCEP launched a substantial EUR 1 billion share buyback to enhance shareholder returns while maintaining investment in growth initiatives across its 31-country footprint.

Historical Performance

Coca-Cola Europacific Partners PLC (CCEP) has demonstrated consistent growth over the past four years with revenues increasing from €17.32 billion in FY2022 to €20.9 billion in FY2025, representing a compound annual growth trajectory of roughly 4% when adjusting for currency fluctuations and acquisitions [F1]. Net income showed more variability but ultimately surged 37% from €1.44 billion in FY2024 to nearly €1.98 billion in FY2025, underscoring improved profitability despite rising cost environments [F1]. Equity levels have remained robust at approximately €8.3 billion by end-2025.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 20.9 | 1979 | +2.3% | +37.0% |

| 2024 | 20.4 | 1444 | +11.7% | -13.5% |

| 2023 | 18.3 | 1669 | +5.7% | +9.7% |

| 2022 | 17.3 | 1521 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 23.8 |

| 2024 | 16.1 |

| 2023 | 20.9 |

| 2022 | 20.4 |

Source: SEC companyfacts cache [F1].

The company’s Europe segment continues as the dominant contributor with €15.4 billion revenue while Asia Pacific represents nearly €5.5 billion [S19]. Both regions experienced modest volume growth tempered by inflationary input costs.

Drivers Behind Past Growth

Several factors underpinning this trajectory include:

- Expansion of product portfolio focusing on health-conscious variants fueling consumer demand.

- Strengthened route-to-market systems leveraging local customer relationships amid global scale.

- Strategic pricing adjustments aligned with raw material cost increases supported top-line without significant volume declines.

- Efficiency initiatives reducing operating expenses on a comparable basis despite inflation [S23].

Future Growth Prospects

Growth catalysts for CCEP remain tied to:

- Continued penetration in emerging Asia Pacific markets including integration gains following recent acquisitions [S19].

- Innovation in packaging sustainability responding to regulatory pressures and consumer preferences.

- Digitally-enabled sales channels enhancing customer engagement and data analytics driven marketing effectiveness.

- Geographic diversification cushioning against region-specific economic headwinds.

Potential constraints include rising commodity prices impacting concentrate costs (increased by ~2.7% per unit case) [S21], regulatory challenges related to anti-corruption laws and environmental compliance [S18], alongside macroeconomic uncertainties like currency volatility affecting reported earnings.

Forecasts and Milestones

Though explicit guidance beyond FY25 is not publicly provided, the company expects ongoing profit growth into FY26 grounded on current momentum [N4]. Monitoring milestones should focus on quarterly volume trends across segments, margin developments amid cost headwinds, execution pace of efficiency programs targeting substantial supply chain upgrades through 2028 [S23], and progression of the large share repurchase plan.

Returns and Capital Allocation

CCEP has prioritized returning capital via dividends complemented by an aggressive share buyback strategy announced early 2026 aiming to repurchase up to EUR 1 billion worth of shares [N4]. This demonstrates a commitment to enhancing shareholder value as net income expanded robustly in FY25.

Financial liquidity reveals some constraints; current assets stood at approximately €6.08 billion versus current liabilities of about €7.59 billion resulting in a current ratio near 0.8 — signaling working capital demands exceed readily available short-term resources [F1]. Cash equivalents totaled about €918 million producing a low cash ratio of roughly 0.12 which necessitates prudent financial management especially under volatile market conditions [F1][S12].

Operating cash flow generation remains healthy although precise figures were not discretely reported; however efficiency savings have partially offset inflation driven operating expense upticks [S23]. Return on equity for FY25 approximates nearly 24%, reflecting effective profit conversion relative to equity base [F1].

Share Buyback Execution Details

Since the announcement dated February 17, 2026 [N4], CCEP has been actively executing its buyback via both US trading venues (including Nasdaq) and London Stock Exchange platforms . The transactions involve incremental purchases totaling several hundred thousands ordinary shares at prices ranging between ~$104–$111 USD per share or £76–£82 GBP per share depending on dates and venues.

Repurchased shares are cancelled immediately supporting EPS enhancements through reduced share count dynamics rather than only returning cash by dividends alone.

Industry Context Analysis (Non-company Specific)

The non-alcoholic beverages sector continues evolving with increasing consumer preference for healthier ingredients pushing companies like CCEP toward reformulation initiatives and portfolio diversification beyond core carbonated soft drinks (CSD). Regulatory scrutiny around sustainability places additional demands on packaging innovation that also affects cost structures globally.

Evolving trade policies and heightened geopolitical risks affect supply chains requiring nimble sourcing strategies paired with advanced risk mitigation protocols including hedging currency exposures extensively—evident from derivative adjustments noted in official filings indicating active currency risk management [S12].

All major players battle against an inflationary backdrop impacting raw materials like sugar, aluminum, PET resin for packaging logistics fuel surcharges—all requiring careful balancing between price increases passed through consumers without significant volume loss.

Within this environment, brand equity remains paramount; CCEP’s extensive proprietary bottling arrangements combined with Coca-Cola Company’s global marketing muscle provide critical competitive insulation allowing premium pricing power.

Leadership Changes Impacting Strategy

Recent board-level changes including the retirement of Independent Non-executive Director Guillaume Bacuvier effective May 28, 2026, replaced by Uvashni Raman—a seasoned CFO with multi-sector experience—signal strengthening of financial oversight aligned with CCEP’s expanding complexity across technology-driven transformation agendas [S3].

Risks Summary

Principal risks identified involve:

- Short-term liquidity tightness given higher current liabilities versus assets potentially limiting agility if unexpected shocks appear.

- Regulatory compliance risks including anti-bribery enforcement actions that could harm brand reputation or result in penalties [S18].

- Raw material cost volatility adding uncertainty to margin profiles despite hedging efforts.

- Macroeconomic factors such as interest rate shifts or geopolitical instability influencing consumer spending patterns within the served territories.

Conclusion

COCA-COLA EUROPACIFIC PARTNERS PLC enters FY26 from a position of solid revenue growth complemented by strong profitability gains fueled by operational excellence and disciplined capital deployment including an ambitious EUR 1 billion share repurchase program underway thus far executed steadily across multiple trading venues.

Liquidity challenges denote close working capital monitoring needs but do not currently jeopardize financial stability given healthy equity ratios and ongoing cash generation capacity.

Execution quality on efficiency roadmaps alongside innovation responsiveness will determine ability to sustain margin expansion amid inflationary pressures within competitive beverage markets worldwide.

Disclaimer: This report is for informational purposes only summarizing publicly available data as of March 13, 2026, without any investment recommendation or endorsement of securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments