Rhinebeck Bancorp’s Path to Sustainable Profitability with Focus on Community Lending

Rhinebeck Bancorp has reversed recent losses by leveraging community banking strengths, commercial lending growth, and disciplined capital management.

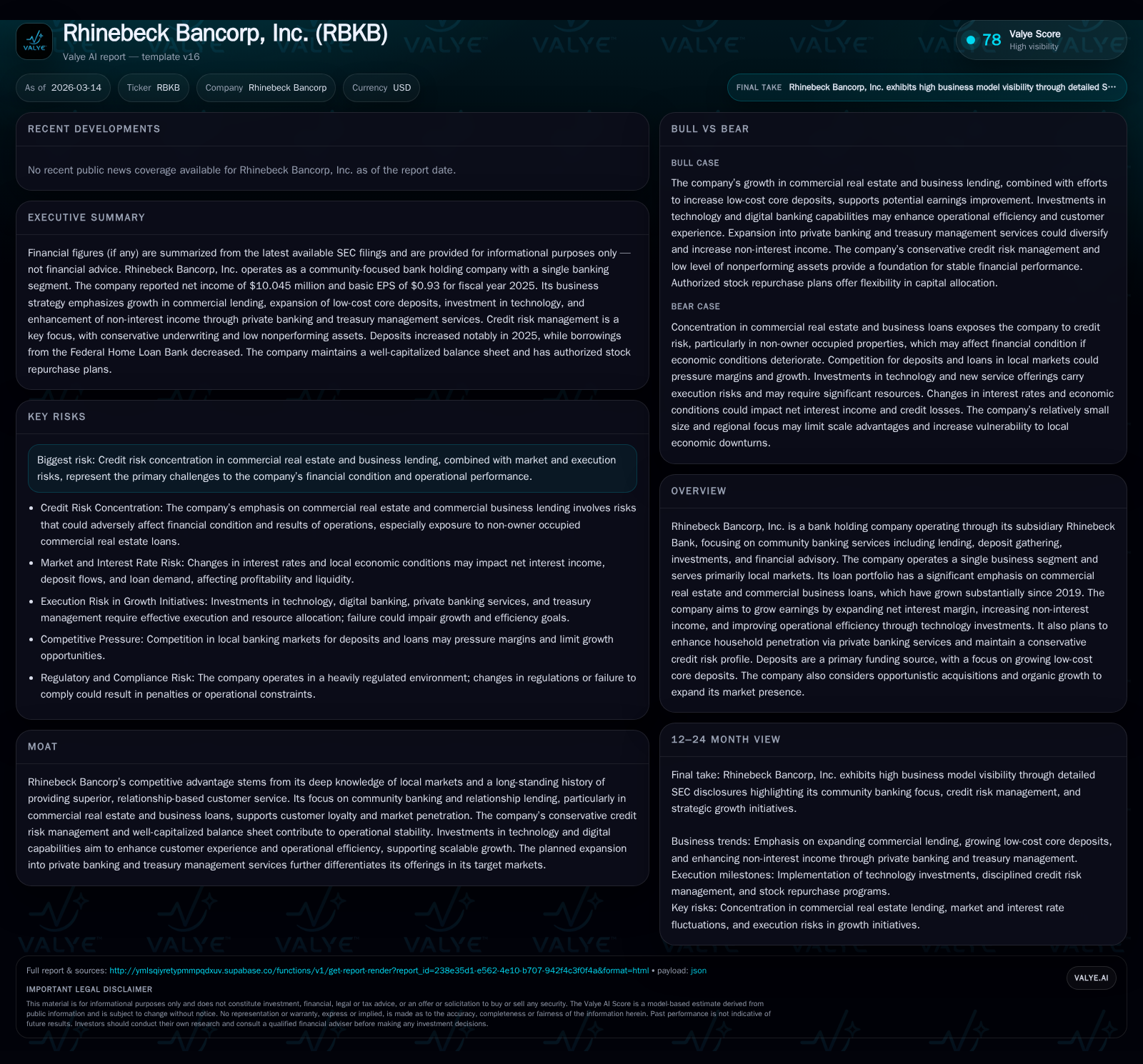

After a profound net loss in 2024, Rhinebeck Bancorp staged a significant financial recovery in 2025, posting $10 million in net income driven by expanded net interest income, reduced credit costs, and strategic balance sheet restructuring. The company’s core profitability stems from its concentration in commercial real estate and business loans, supported by a conservative underwriting framework that curtails credit risk amid loan portfolio concentration. Growth prospects are grounded in expanding low-cost core deposits, launching treasury management services, investing in technology for efficiency gains, and opportunistically pursuing market expansion alongside private banking development. Capital allocation remains disciplined with ongoing share repurchase authorization underpinned by solid capital ratios and controlled leverage.

From Loss to Profit: Rhinebeck Bancorp’s Recent Financial Performance

Rhinebeck Bancorp experienced a striking financial reversal between FY2024 and FY2025. After reporting a net loss of $8.62 million in 2024, the company returned to profitability in 2025 with net income of approximately $10.05 million—a dramatic swing representing a 216.5% improvement year-over-year [F1]. This improvement followed balance sheet restructuring during late 2024 that enhanced asset quality and repriced interest-bearing assets.

Operating cash flow similarly advanced nearly 38.6% from $8.47 million in 2024 to $11.74 million in 2025 [F1], providing liquidity to fund operations and modest capital expenditures totaling $850,000 while still generating healthy free cash flow near $10.9 million [F1]. Shareholders' equity increased about 12.3% to approximately $136.9 million at year-end 2025 (from $121.8 million the prior year), resulting in an ROE estimate around 7.3%, reflecting improved profit generation without aggressive leverage growth [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 10 | 12 | 850000 | +216.5% |

| 2024 | -9 | 8 | 791000 | -296.1% |

| 2023 | 4 | 7 | 578000 | -37.2% |

| 2022 | 7 | 15 | 1132000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 11 | 7.3 |

| 2024 | 8 | -7.1 |

| 2023 | 6 | 3.9 |

| 2022 | 14 | 6.5 |

Source: SEC companyfacts cache [F1].

Table summarizes Rhinebeck Bancorp’s key financial metrics illustrating turnaround from loss to profit.

Driving Profitability: Core Businesses Behind the Turnaround

Central to Rhinebeck's earnings recovery is its focus on community banking operations with significant exposure to commercial real estate (CRE) and commercial business lending segments [S4,S29]. These areas have seen strong loan book growth since the reorganization period starting around late-2019.

Net interest income increased sharply by more than $8 million (+23%), reaching approximately $46.4 million in FY2025—driven by higher yields on assets due to increased CRE loan concentrations with superior pricing compared to legacy portfolios as well as favorable deposit cost dynamics that lowered interest expense by nearly twelve percent [S29,S4]. This reflects effective asset-liability management via adjustable rate loans complemented by stable core deposits.

Non-interest income also contributed positively through service charges on deposit accounts and investment advisory fees supported by Rhinebeck Asset Management ("RAM") [S15], with ongoing efforts to broaden fee-generating services aimed at deeper customer wallet share.

Conservative Credit Risk Amid Concentration in Commercial Loans

While CRE lending concentrates risk due to market cyclicality and property valuations within the Hudson Valley region served by Rhinebeck Bank [S15], the bank employs rigorous underwriting criteria designed to mitigate downside scenarios [S17,S18]. Loans are classified into risk categories such as Watch or Special Mention for heightened monitoring when performance deteriorates temporarily.

Non-performing assets declined ten percent year-over-year ending at about $3.7 million or roughly 0.28% of total assets as of December 31, 2025 indicating strong credit discipline even amid loan book expansion [S7,S12]. Provision for credit losses fell more than forty percent to $1.7 million reflecting lower net charge-offs especially within indirect automobile and commercial portfolios despite some upticks in CRE charge-offs [S12,S7]. The allowance for credit losses was about 0.87% of total loans providing substantial coverage above non-performing balances.

Independent third-party reviews combined with internal delinquency reporting enhance early risk identification—reflecting best practices among community lenders focused on long-term relationship viability rather than volume alone.

Expanding Core Deposits and Treasury Management to Strengthen Funding

Deposits are Rhinebeck’s primary funding base with strategic emphasis on growing low-cost core deposits distinguished from time deposits which tend to be pricier and more volatile amid rising rates cycles [S4]. At December 31st 2025 core deposits totaled approximately $720 million representing about two-thirds (65.6%) of total deposits—a fortification against interest rate stress owing to inherent stability and lower pricing versus brokered or wholesale deposits.

To bolster deposit stickiness particularly among commercial borrowers who represent concentrated loan demand sectors currently serviced by Rhinebeck’s commercial teams the company is launching comprehensive treasury management solutions including cash management products such as ACH origination and remote deposit capture upgrades alongside fee-bearing services encouraging usage of checking accounts thereby enhancing profitability via recurring fee income streams [S4]. These actions align with community bank best practices where treasury management bridges lending-client relationships creating cross-selling synergies.

The bank also contemplates partnerships including Banking-as-a-Service models facilitating digital account acquisition resulting ultimately in more efficient onboarding pipelines for lower cost deposits while controlling operational expenses.

Technology Investments Aimed at Scaling Efficiency and Customer Experience

Rhinebeck is actively investing in upgraded technology infrastructure tailored for community bank scale but designed for operational efficiency improvements and elevated digital customer experiences consistent with peer benchmarks [S4,S16]. Current fintech offerings include mobile deposit capture tools along with bill pay enhancements and card valet programs allowing customers better control over card usage.

Additional planned initiatives involve automating routine manual workflows—such as loan documentation processing—and selective uses of AI-enabled analytics improving front-line decision-making capabilities especially within credit risk assessment and marketing personalization functions [S16]. Digital account opening enhancements aim to reduce client acquisition friction thus shortening time-to-fund periods critical for loan production team success.

These investments are expected not only to improve efficiency ratios relative to similar-sized banks but also future-proof customer engagement strategies differentiating Rhinebeck from older tech-dependent competitors.

Capital Allocation: Share Repurchases and Maintaining Strong Capital Ratios

Prudence governs Rhinebeck’s capital deployment philosophy highlighted by disciplined share repurchasing accompanied by solid capitalization maintenance consistent with regulatory expectations [S19]. Two active stock repurchase authorizations exist: one initiated September 2022 allowing up to ~247k shares (with ~39k left unexecuted), followed by a larger July 2025 plan authorizing repurchase up to ~540k shares all still available at December quarter-end except for an actual purchase of just over eight thousand shares at an average price near $11.76 per share reported within Q4 calendar quarter activity demonstrating measured pace reflective of cautious capital management amid evolving market conditions [S19].

Capital ratios benefit from inclusion of subordinated debt instruments utilized in Tier-1 capital calculations through trust preferred securities issued via RSB Capital Trust I—an established strategy enabling cushion against earnings volatility while preserving flexibility toward strategic growth moves without dilutive equity issuance [S9]. No dividends were declared during the period indicating preference toward reinvestment and buybacks enhancing book value per share accretion given rebound phase aims.

Growth Outlook: Organic Expansion and Private Banking Initiatives

Looking beyond financial stabilization Rhinebeck intends deliberate organic deposit base expansion—with particular attention toward penetrating contiguous New York counties mirroring historical footprints—and selectively exploring de novo branch openings where market economics justify extending brand footprint complemented by enhanced technology reach principles reducing physical dependency over time [S7].

A pronounced new strategic initiative is development of private banking services designed specifically for mass-affluent clientele including professionals and business owners underserved by large regional banks that impose high minimums or rigid product structures inconvenient for this subsector's needs; leveraging existing wealth management resources enables synergy aimed at increasing household penetration while deepening average customer lifetime value offering comprehensive advisory-led relationship banking models distinct from commoditized retail banking approaches prevalent among national players at scale [S16].

Acquisition considerations remain opportunistic—targeting institutions or units aligning culturally or geographically adding tangible value—but no pending transactions are currently disclosed underscoring patient capital deployment philosophy centered on internal growth execution first while keeping external options open depending on deal economics aligning with franchise enhancement objectives over time horizons consistent with shareholder value creation mandates [S7].

Disclosure: This analysis synthesizes publicly filed documents without offering investment advice or recommendations regarding Rhinebeck Bancorp securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments