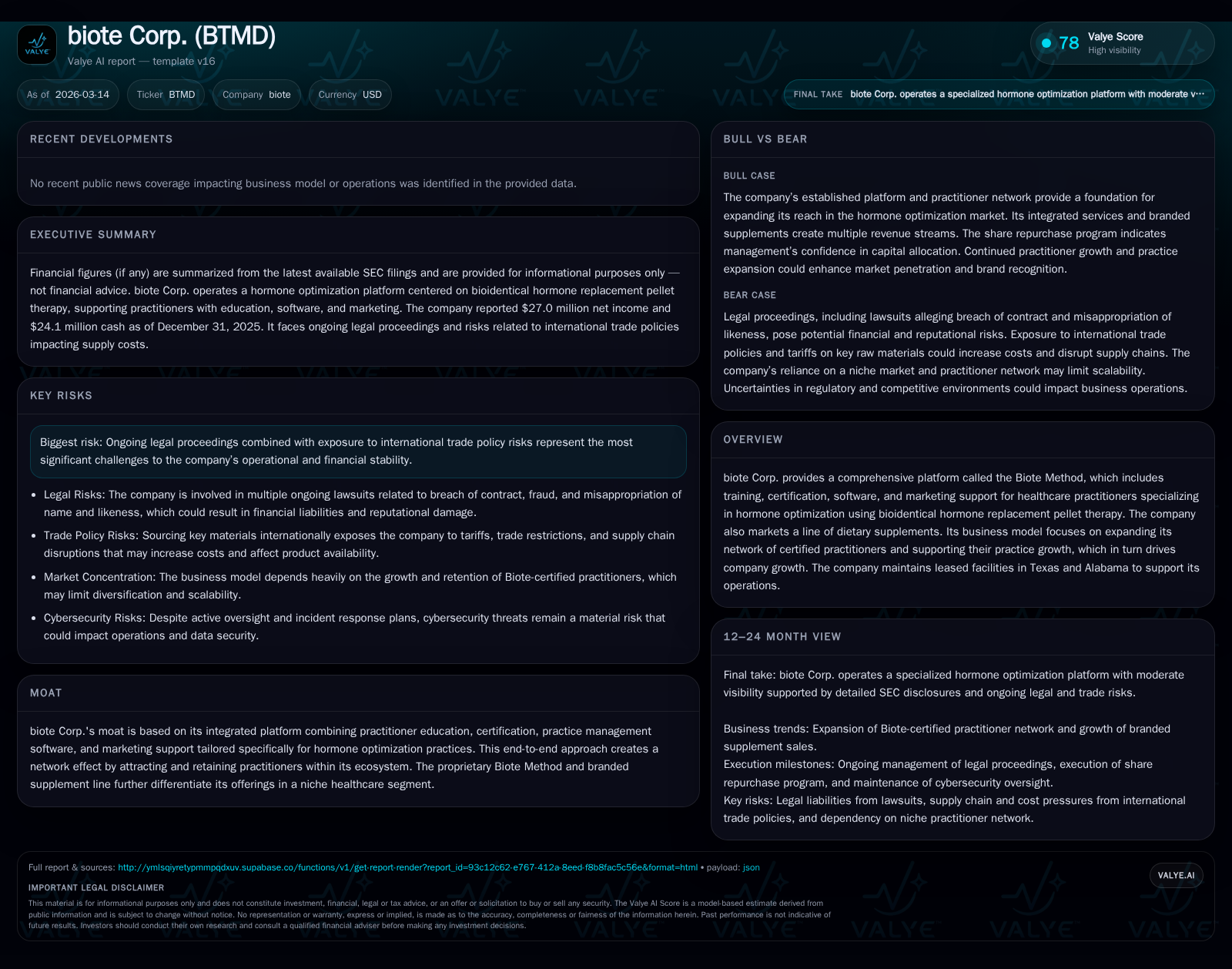

biote Corp.’s Turnaround Momentum and Financial Discipline in Hormone Optimization

biote Corp. progresses from significant operating losses to sustained profitability by leveraging its proprietary hormone therapy platform, while skillfully managing legal and trade-related headwinds alongside disciplined capital allocation.

After enduring operating losses in 2022, biote Corp. achieved a financial turnaround with 12.5% year-over-year operating income growth and over sevenfold net income increase in 2025, underpinned by its integrated Biote Method platform that combines practitioner certification, specialized software, and marketing support for hormone optimization. Despite ongoing legal disputes and tariff challenges increasing supply chain costs, the company maintains compliance with debt covenants and exhibits robust operating cash flow generation. Capital expenditures have been prudently scaled back following earlier investments, while dividends and share buybacks have been moderated to preserve liquidity amid operational uncertainties.

Tracking Growth: From Operating Losses to Sustainable Profitability

biote Corp.'s financial trajectory over recent years highlights a pronounced turnaround. In fiscal year (FY) 2022, the company endured a large operating loss of approximately -$60.7 million as it invested heavily in establishing its niche hormone optimization platform [F1]. However, by FY2023 and FY2024, operating income improved steadily to $28.7 million and $31.6 million respectively, culminating in a sizable jump to $35.6 million in FY2025—a 12.5% increment over the prior year [F1]. Net income exhibited even higher growth intensity; after recovering slightly to $3.3 million in 2023 and stabilizing near $3.15 million in 2024, it surged sevenfold to $27 million in 2025 [F1].

Operating cash flow followed a similar path of improvement though it saw some normalization after peak levels: from negative cash flow of about -$9.2 million in 2022, CFO improved sharply to roughly $26.9 million (FY23) and then jumped again to over $45 million (FY24), before retreating somewhat to approximately $35.2 million in FY25 [F1]. This reflects both higher profitability but also increased working capital deployment or timing variations.

Capital expenditures rose sharply during this period as well: from nominal levels around $333K (FY22) up slightly in 23 but ballooning sharply to $6.4 million (FY24) before moderated reduction back down to near $5 million (FY25), indicating initial heavy investment phases followed by more cautious spending [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 27 | 35 | 36 | 5 | +756.7% |

| 2024 | 3 | 45 | 32 | 6 | -4.8% |

| 2023 | 3 | 27 | 29 | 0 | +442.2% |

| 2022 | -1 | -9 | -61 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 2 | 3 | 30 |

| 2024 | 5 | 6 | 39 |

| 2023 | 9 | 27 | |

| 2022 | 13 | -9 |

Source: SEC companyfacts cache [F1].

This financial evolution underscores the company's shift from early-stage investment losses toward operational profitability driven by expanded adoption of its proprietary offerings.

Biote Method Platform: The Engine of Practitioner Network Expansion

At the core of biote Corp.’s value proposition lies the "Biote Method": a comprehensive package combining practitioner training, certification, proprietary practice management software tailored for hormone optimization clinics, and dedicated marketing support . This integrated ecosystem is focused specifically on bioidentical hormone replacement pellet therapy—a niche within hormone optimization recognized for its efficacy and growing patient demand.

This platform fosters a network effect moat by attracting new healthcare practitioners who benefit not only from clinical education but also practical tools for revenue cycle management and patient engagement—all underpinned by Biote's branded dietary supplements marketing.

Such bundling discourages attrition of certified practitioners due to switching costs embedded in training investments and software integration continuity demands common within healthcare IT systems . The seamless alignment across practitioner certification programs combined with digital tools for appointment scheduling, inventory tracking of pellets/supplements, billing workflows, plus co-branded marketing amplifies clinic success rates while reinforcing loyalty within the Biote ecosystem [S1].

Legal Proceedings and Trade Policy: Key Headwinds on the Horizon

Despite operational momentum, biote faces ongoing legal challenges that impose both direct expense burdens and reputational risks [S12][S13]. Notably, Right Value Drug Stores filed suit alleging breach of contract and fraud; litigation proceeded through hearings with preliminary injunction requests denied but was ultimately resolved via settlement requiring payments totaling $5 million completed over early 2025 into February 2026 [S12][S13][S14]. Parallel suits regarding use of image/likeness rights—the "Gary S Donovitz" case among others—remain active with temporary injunctions issued at times but subject to appeals; outcomes remain uncertain with trial dates scheduled mid-2026 [S21][S22][S23][S24].

On the trade front, tariffs imposed on critical raw materials have contributed cost pressures [S2]. Estradiol raw materials sourced principally from China face tariff-induced price increases while trocars imported from Pakistan have similarly encountered cost headwinds tied to geopolitical uncertainties causing elevated supply chain complexity [S2]. These tariff-driven input cost escalations create margin compression risk which could necessitate downstream pricing adjustments affecting customer demand dynamics amid competitive pressures.

Moreover, macroeconomic volatility stemming from international trade disputes influences broader market conditions—potentially elongating sales cycles among practitioners concerned about economic outlooks and supply stability [S2]. While no material adverse impact has manifested yet per disclosures , ongoing monitoring remains warranted given these variables’ potential operational disruptions.

Capital Structure and Debt Management: Balancing Leverage with Liquidity

biote Corp.’s capital structure centers on a senior secured credit agreement featuring a fully drawn $125 million term loan complemented by a revolving credit facility capped at $50 million [S4][S5][F1]. The term loan requires quarterly principal amortization payments of approximately $1.6 million with maturity due May 26, 2027 [S4]. As of December 31, 2025, outstanding term loan principal was about $103 million down from roughly $109 million year prior; revolving borrowings stood at approximately $5 million drawn against available capacity [S4][S6][F1].

Interest expense averaged roughly 6.32%, linked either to SOFR plus margin or base rate plus margin based on borrower election [S4]. Total net interest expense remained stable near $11 million annually despite lower principal balances due primarily to diminishing interest income on reduced cash balances combined with increases related to accretion on share repurchase liabilities [S13].

The Company adheres strictly to covenants enforcing maximum net leverage ratio of no more than 3.75:1 and minimum fixed charge coverage ratio no less than 1.25:1; all covenant tests were met as of end-FY25 with compliance maintained historically as well [S5][F1]. Lender fees capitalized at roughly $4 million are amortized over loan life contributing about $0.8 million per annum to finance costs [S4].

Cash reserves declined notably—from approximately $39 million at end-2024 down to about $24 million at end-2025—reflecting debt repayments alongside investments into operations however current liquidity coupled with revolver capacity supports near-term funding requirements per management statements [S6][S8][F1]. This balance showcases targeted prudent debt reduction while preserving operational agility.

Financial Returns and Cash Flow Trends: Analyzing ROE, CFO, Dividends, and Buybacks

Though achieving positive net income growth recently, biote continues to report negative shareholders’ equity nearing -$58.5 million driven largely by accumulated deficits incurred during early high-investment years plus recognized share repurchase liabilities (which are settled over time) impacting equity accounts adversely [F1]. This results in a negative return on equity approximated near -46%, illustrating structural capital challenges despite operating profitability gains.

Operating cash flows before capex remain robust: CFO maxima occurred FY24 near $45M yet saw decline back towards $35M FY25—still representing healthy conversion of earnings into real cash generation capacity fundamental for sustaining platform growth initiatives without excessive external financing reliance [F1]. Capital expenditures moderated after steep increases noting $($5M) spent FY25 versus $(~$6.4M) prior year showcasing selective asset investment discipline following foundational IT/software build outs alongside compounding equipment additions supporting clinic growth infrastructure [F1][S25][S26].

Dividend distributions exhibited downward adjustment consistent with liquidity preservation priorities: falling from ~$4.74M paid FY24 down sharply towards ~1.73M FY25 reflective of balancing shareholder returns with funding needs amidst cost uncertainties pertaining notably to legal expenditures reducing but still present along with trade policy effects impacting margin outlooks modestly [F1][S13]. Simultaneously buybacks decreased materially ($3.36M vs prior ~$5.59M), highlighting conservative capital deployment themes aligned with managing earnings variability risks including earnout liability fluctuations influenced by share price volatility over recent periods [F1][S13][S20].

What to Watch: Financial Covenants, Revenue Drivers, and Market Acceptance

With no explicit forward guidance publicly provided by management beyond broad confidence expressed around current liquidity sufficiency covering next twelve months’ needs inclusive of debt service obligations,[S8] attention turns towards several pivotal developments likely shaping near-to-medium term operational trajectory:

- Vigilance over quarterly covenant compliance underpinning borrowing availability remains critical given debt service schedules tied closely to free cash flow dynamics.[S5]

- Litigation outcomes expected through mid-2026 trials especially those involving name/image rights could reshape expenses or influence franchise reputation thus impacting practitioner enthusiasm or patient acquisition efforts.

- Growth momentum within dietary supplement lines marketed directly via e-commerce channels (e.g., Amazon sites) bears watching as these help broaden revenue diversification beyond pure services contracts driving Biote-certified practitioners’ practices.

- Trade policy evolutions including potential tariff adjustments or supply source diversification efforts will affect costs on hormone pellets components such as estradiol or ancillary device inputs like trocars; shifts here could affect pricing power or margins fundamentally.[S2]

- Market acceptance trends gauged via practitioner network expansion rates will continue defining revenue run-rate sustainability since recurring licensing fees for certification combined with software subscriptions create sticky revenue streams when clinic retention remains high.

In summary, biote Corp.'s steady financial progression coupled with an integrated service-plus-product platform establishes foundational resilience complemented by judicious capital stewardship amid notable external risks — legal uncertainties alongside tariff-imposed supply cost exposures warrant attentiveness but currently do not overshadow underlying business momentum backed by expanding practitioner ecosystem engagement.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding any securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments