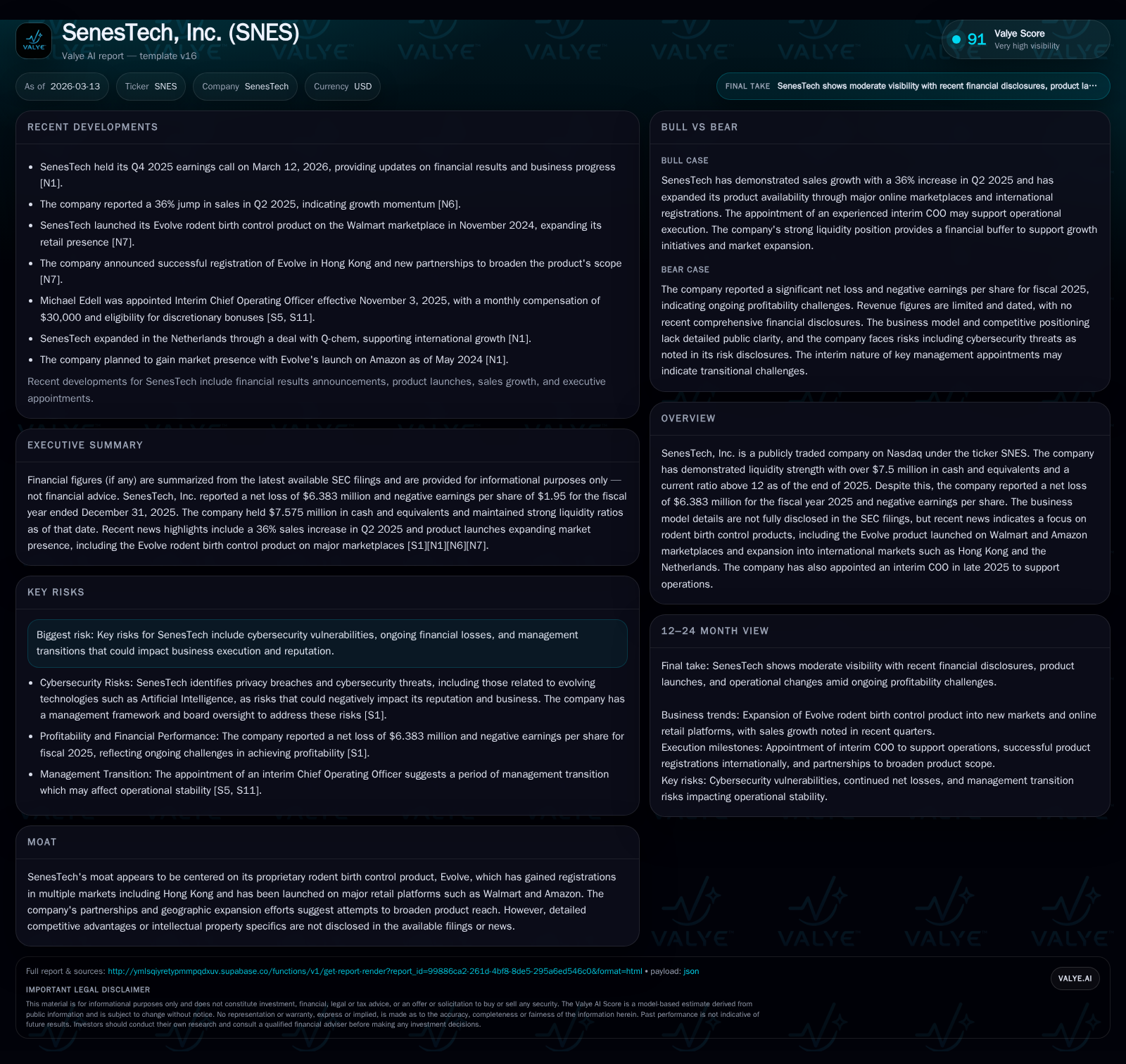

SenesTech’s Rodent Control Innovation Struggles to Offset Mounting Losses

SenesTech's proprietary rodent birth control product powers its market reach expansion but profitability remains elusive due to sustained operating losses.

SenesTech, Inc. has positioned its rodent reproductive control product, Evolve, as a strategic growth lever by entering major US retail channels such as Walmart and Amazon and expanding into international markets including Hong Kong and the Netherlands. Despite a more than doubling in revenue from 2019 to 2021, persistent net losses near $6.4 million in fiscal year 2025 illustrate an ongoing struggle to scale profitably. Operational changes like appointing an interim COO underscore efforts to stabilize execution amidst expansion ambitions. The company maintains strong liquidity buffers with a current ratio above 12 and over $7.5 million in cash, but continued negative free cash flow highlights the capital-intensive nature of commercializing innovative pest control solutions.

From Early Traction to Recent Revenue Growth: Historical Performance Highlights

SenesTech's financial trajectory demonstrates encouraging top-line momentum juxtaposed against persistent net losses that challenge scaling profitability. Revenue surged from $143,000 in FY2019 to $600,000 by FY2021, representing a more than fourfold increase within two years [F1]. This step-change aligns with commercial rollout activities for their proprietary rodent birth control product, Evolve. However, gains at the top have not translated into operating profits; the company reported operating income losses of approximately -$6.5 million in FY2025 with a modest year-over-year improvement relative to prior years’ deeper losses [F1]. Net income follows this trend, registering near -$6.38 million in 2025 with marginal reduction compared to previous years.

Operating cash flow (CFO) also shows heavy outflows though slight improvement is noted — negative $5.75 million in FY2025 versus higher negatives in earlier years [F1]. This reflects ongoing investment coupled with operational expenses outweighing revenue realization.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | -6 | -7 | 138000 | -3.2% |

| 2024 | -6 | -6 | -6 | 84000 | +19.8% |

| 2023 | -8 | -8 | -8 | 149000 | +20.5% |

| 2022 | -10 | -9 | -10 | 174000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -66.7 |

| 2024 | -6 | -246.3 |

| 2023 | -8 | -121.4 |

| 2022 | -9 | -183.7 |

Source: SEC companyfacts cache [F1].

Revenue data only available through FY2021; operating income and cash flows reported through FY2025; all figures USD.

This pattern illustrates typical operating leverage issues faced by companies innovating biotech-adjacent products where upfront R&D and market entry costs precede scalable revenues.

The Rodent Birth Control Niche: Assessing SenesTech’s Market Differentiators

At the core of SenesTech's moat lies Evolve’s proprietary reproductive control chemistry designed to curb rodent populations via fertility suppression rather than lethal toxicants [S1][S5][N1]. This approach signals a shift toward humane pest management solutions valued by regulators and environmentally conscious consumers alike.

The company’s progress securing regulatory registrations across diverse jurisdictions evidences barriers to entry that could reinforce competitive positioning. For instance, Evolve obtained registration approval in Hong Kong — a notable milestone given the stringent safety validation procedures endemic in Asian markets [S1][N1]. These registrations represent critical groundwork supporting geographic diversification efforts beyond North America.

Such non-lethal strategies contrast traditional rodenticides that face increasing scrutiny over environmental impact and resistance issues within urban pest populations — factors elevating SenesTech’s developmental premise of reproductive control chemistry as a sustainable alternative.

Innovation and Market Expansion: Evolve’s Launch on Walmart, Amazon, and International Registrations

Commercialization tactically leverages US retail giants Walmart and Amazon as primary sales channels for Evolve since late 2024/early 2025 periods [N1][S1]. Such retail presence can significantly amplify brand visibility and consumer access for a novel pest control product while facilitating data capture on adoption patterns.

In parallel with these domestic distribution initiatives are expansions into international territories including Hong Kong and the Netherlands as registered markets [N1][S1]. These moves aim at risk diversification across different regulatory regimes and consumer bases while building global footprint credibility.

While initial revenues remain modest relative to overall expenses — reflective of nascent penetration — these channel developments form the backbone of scaling efforts underway alongside new partnerships.

Financial Challenges Persist: Profitability Trends and Operating Cash Flow Analysis

Despite revenue momentum and broadened distribution outlets for Evolve, SenesTech continues experiencing material losses underscoring persistent operating leverage challenges [F1][N1]. Operating income stood at negative $6.5 million in fiscal year 2025 — a marginal improvement but still substantially negative relative to revenues capped below $1 million historically.

The sizable operating cash flow deficit ($-5.75M in FY2025) spotlights capital consumption exceeding earnings from commercialization activities [F1]. Given an approximate free cash flow position near negative $5.88 million (operating cash flow less capex), SenesTech faces typical early-stage scaling pressures balancing investment against returns.

These results underscore that while Evolve differentiates itself technologically and strategically via retail/international deployments, financial stability remains challenged absent substantial revenue scaling or cost containment breakthroughs.

Capital Structure Robustness: Liquidity Position and Capital Allocation Focus

SenesTech maintains a strong liquidity position that supports ongoing commercialization efforts despite sustained losses [F1][S13][S16]. As of December 31, 2025, cash and cash equivalents totaled approximately $7.58 million with current assets of about $10.06 million against current liabilities near $798 thousand resulting in an elevated current ratio around 12.61 — signaling robust short-term financial flexibility.

Equity increased significantly from about $2.51 million at end-2024 to nearly $9.57 million at end-2025 evidencing recent capital raises deployed to fund growth initiatives [F1].

No dividends or share repurchase programs have been declared or executed as per SEC filings; capital allocation priorities emphasize preserving liquidity over immediate shareholder returns during this development phase [S13][S16].

Leadership Transition: Interim COO Appointment Amid Executive Changes

Operational leadership saw changes with Michael Edell appointed interim Chief Operating Officer in late 2025 aimed at strengthening execution capabilities during expansion [N1][S19][S20][S23]. Edell’s background includes commercialization experience with consumer-facing technologies which may support operational stabilization.

Additionally early-2026 announcements flagged retirement plans for the CEO effective mid-2026 or upon successor appointment highlighting governance transitions that could affect near-term execution risk profiles [N1][S22].

Effectively managing leadership transitions will be critical given SenesTech’s relatively small organizational scale where executive shifts can impact operational continuity.

Cybersecurity Governance: Protecting Proprietary Technology Assets

SenesTech explicitly identifies cybersecurity risks related to its business model including vulnerabilities associated with evolving tools like Artificial Intelligence [S7]. Oversight is exercised by the Board supported by management teams led by CFO and Vice President of Manufacturing responsible for risk assessment and incident response frameworks.

Regular board reporting on cybersecurity threats and mitigation measures underscores commitment to safeguarding proprietary reproductive control technology—a key intangible asset underpinning competitive advantage.

Outlook: Key Metrics for Growth and Capital Efficiency Monitoring

Future performance hinges on successfully scaling revenue through expanded retail penetration domestically and internationally alongside improved operational efficiencies under new interim leadership [N1][S3].

Key metrics include revenue growth sufficient to narrow operating losses materially; reduction in negative free cash flow trends signaling better capital utilization; and smooth executive transitions maintaining strategic momentum.

SenesTech remains heavily invested in pioneering non-lethal rodent population management technologies poised at commercial inflection points but must navigate significant financial headwinds characteristic of early-stage innovation ventures.

Disclaimer: This analysis is based solely on publicly available filings and news disclosures as cited; it does not constitute investment advice nor a forecast of future performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments