Perfect Corp. Posts 14.9% Revenue Gain Fuelled by AI, Faces Enterprise Sales Cycle Delays

Strong liquidity and AI-driven subscription growth support Perfect Corp.’s innovation and luxury market expansion despite a net income dip and cautious enterprise spending.

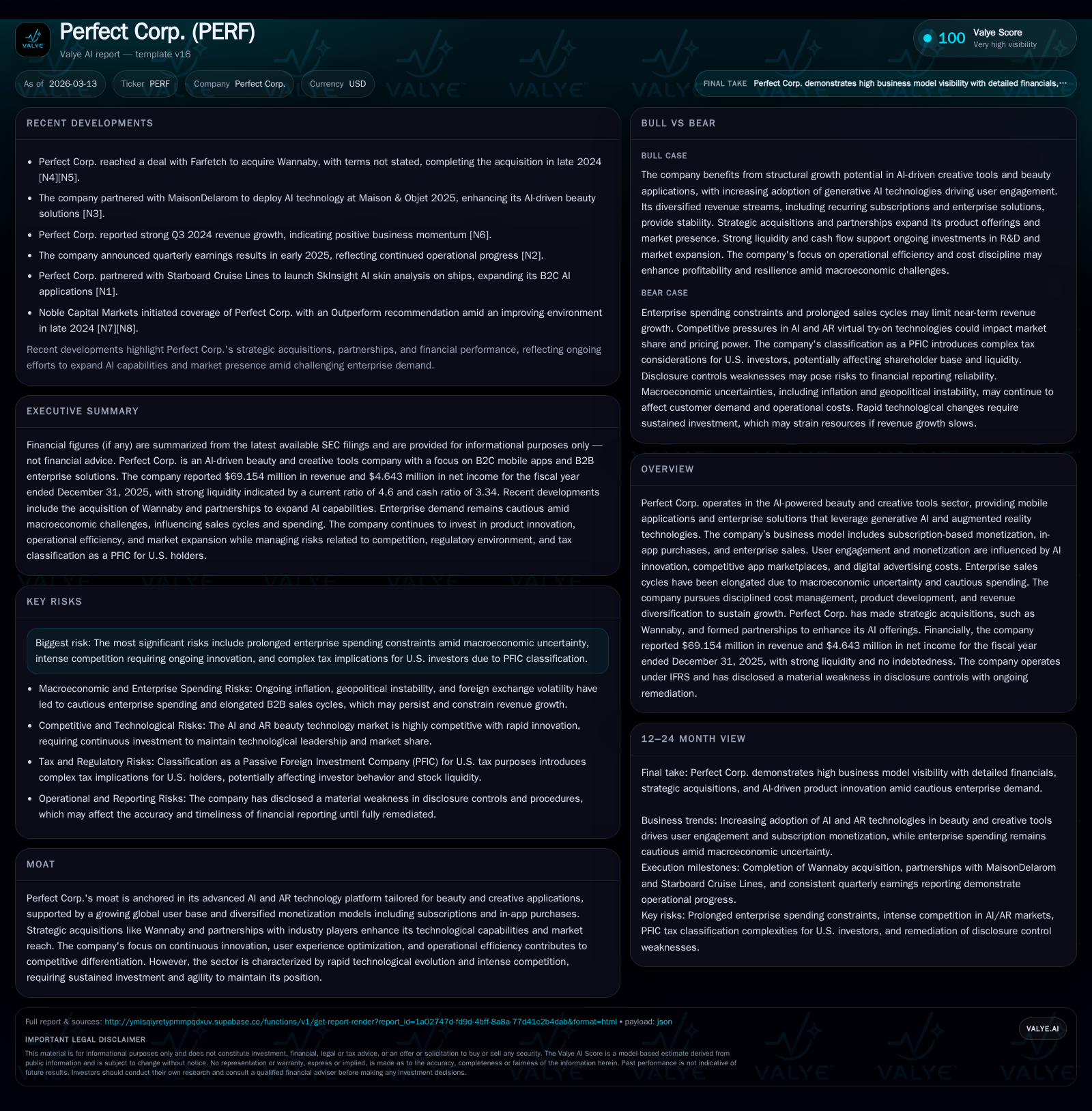

Perfect Corp., a leader in AI-powered beauty and creative tools, reported 14.9% revenue growth to $69.15 million in FY2025, supported by subscription and in-app monetization. Despite a slight net income decline to $4.64 million amid prolonged enterprise sales cycles, the company maintains strong liquidity with no debt and over $125 million in cash and equivalents, enabling sustained R&D investment and operational discipline. Key focus areas include expanding AI/AR features, premium offerings, and luxury sector penetration. Monitoring subscription metrics and enterprise spending recovery will be critical for future momentum.

Company Overview

Perfect Corp. is a prominent player in the AI-powered beauty and creative tools sector, offering mobile apps and enterprise solutions that integrate generative AI with augmented reality (AR) technologies. The company monetizes through subscriptions, in-app purchases utilizing virtual currency models such as Virtual Points, and direct enterprise sales. Its focus on cutting-edge AI/AR innovations combined with effective user engagement has established a strong global presence within the digital beauty ecosystem.

Historical Financial Performance

From FY2022 through FY2025, Perfect Corp.'s revenues grew consistently from $47.30 million to $69.15 million, representing a compound growth trajectory underpinned by rising adoption of its AI-enhanced products.[F1]

Net income demonstrated significant improvement from a substantial loss of $161.74 million in FY2022—likely attributable to one-time impairments or restructuring—to positive profitability in subsequent years with net income ranging from approximately $4.6 million to $5.4 million.[F1]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 69 | 5 | +14.9% | -7.5% |

| 2024 | 60 | 5 | +12.5% | -7.3% |

| 2023 | 54 | 5 | +13.1% | +103.3% |

| 2022 | 47 | -162 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 3.0 |

| 2024 | 3.4 |

| 2023 | 3.9 |

| 2022 | -88.9 |

Source: SEC companyfacts cache [F1].

The modest net income decline in FY2025 reflects extended B2B sales cycles amid cautious enterprise spending despite robust consumer-driven revenue growth.[F1][S8]

Growth Outlook

Perfect Corp.'s future growth hinges on advancing generative AI capabilities embedded within its consumer beauty apps and enterprise-grade AR solutions.

Continuous R&D investments aim to improve AI algorithms for facial recognition, makeup simulation realism, and creative tool integration.[S12][S13] Additionally, the company plans to diversify revenue by expanding premium feature sets and entering synergistic verticals such as the luxury brand sector.[S1]

Acquisitions like Wannaby enhance AR expertise critical for immersive experiences at both consumer and B2B levels.[F1]

However, macroeconomic uncertainty continues to constrain enterprise spending, elongating sales cycles since mid-2022—a trend expected to persist—thereby limiting visibility into near-term B2B revenue scaling.[S13]

Capital Allocation & Financial Position

As of December 31, 2025, Perfect Corp.'s liquidity position remains strong with cash and cash equivalents totaling approximately $126 million supplemented by $36.3 million in time deposits and $10.2 million in U.S Treasury securities; the company carries no debt or bank borrowings.[F1][S1][S3]

Operating cash flows were stable at around $13.3 million in FY2025 despite challenging enterprise conditions,[S8] while capital expenditures remained minimal (<$0.5 million), focused primarily on server purchases and ERP system upgrades reflecting efficient infrastructure management.[S6]

No dividends or share repurchases were reported post-2023 when buybacks aggregated about $51 million tied to program completions.[F1]

The company's current ratio stands near 4.6x indicating ample short-term liquidity relative to liabilities.[F1]

Approximate return on equity based on FY2025 net income over shareholders' equity (~$153 million) is around 3%, consistent with ongoing investment during growth phases.[F1]

Risks & Challenges

Key risks include persistent caution among enterprise clients impacting topline visibility,[S13] intense competition necessitating continuous innovation,[S19] and an identified material weakness in internal controls which management is actively addressing.[S15]

Additionally, U.S.-based investors should consider complex tax implications related to the company’s status under U.S federal tax law.

Conclusion & Monitoring Points

Perfect Corp.'s solid consumer demand fueled by AI-driven features contrasts with constrained but potentially recoverable corporate spending patterns. Key areas to monitor include:

- Normalization of elongated enterprise sales cycles which could unlock significant upside.

- Execution of product roadmap especially regarding luxury sector expansion.

- Subscription conversion rates and virtual currency monetization supporting recurring revenue stability.

- Progress on remediation of internal control weaknesses affecting financial reporting reliability.

Maintaining substantial liquidity reserves alongside disciplined R&D investment positions Perfect strategically amid evolving market dynamics.

This analysis incorporates data from Perfect Corp.’s latest SEC filings through March 2026 combined with Valye News insights; it is intended for informational purposes without constituting investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments