Waldencast’s Strategic Struggles and Growth Initiatives Reshape Skincare Ambitions

Waldencast plc’s expanding brand portfolio and innovation efforts collide with mounting financial losses and governance flaws, challenging its future trajectory.

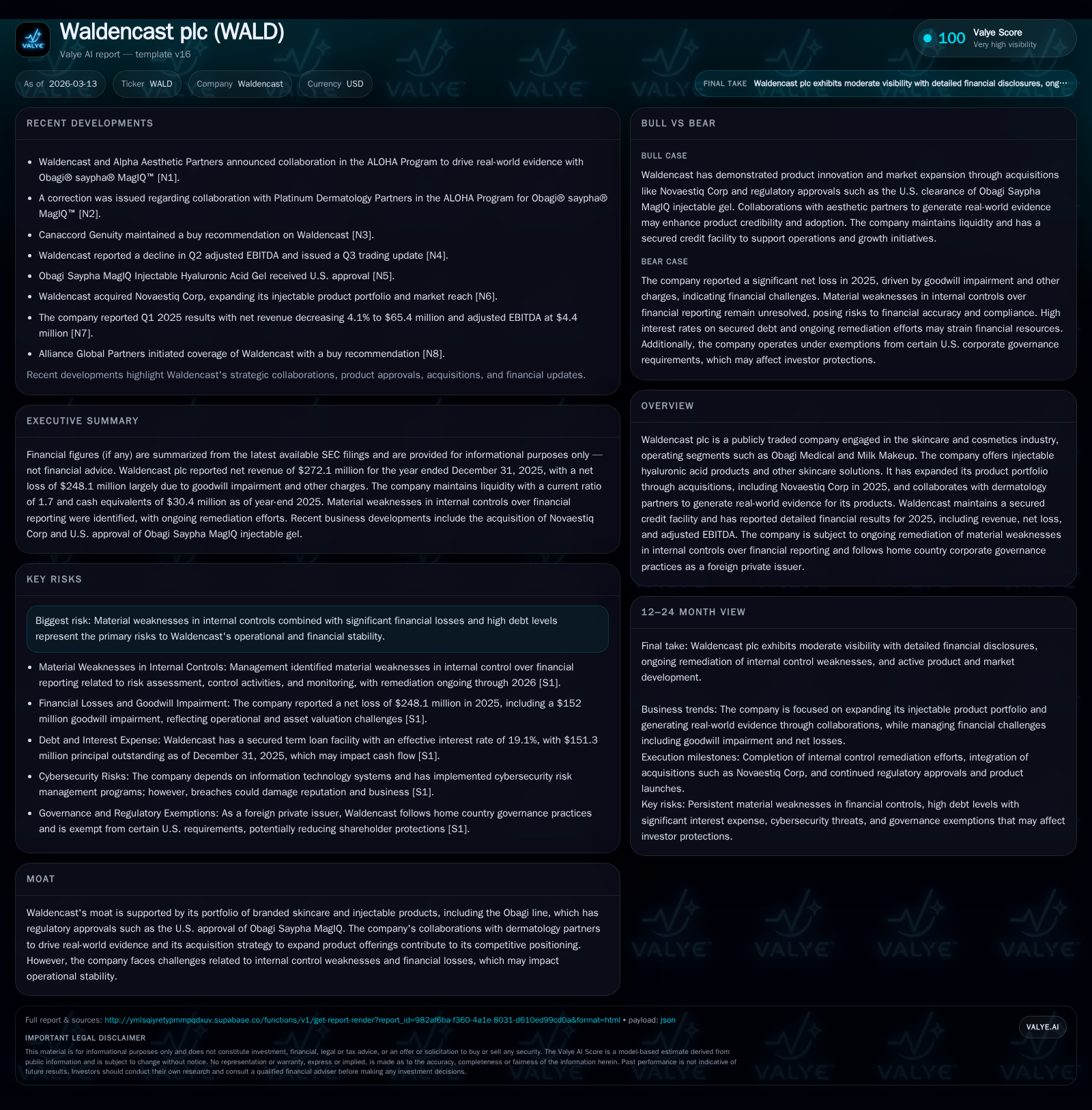

Waldencast plc continues to grow its presence in skincare and beauty through acquisitions like Obagi Medical, Milk Makeup, and Novaestiq Corp, leveraging strategic collaborations and product innovation. However, its financial performance has deteriorated sharply with soaring goodwill impairment charges and escalating losses that more than quadrupled year-over-year. Internal control deficiencies compound risks amid high debt costs and constrained liquidity. Future growth hinges on integrating acquisitions effectively while stabilizing operations and addressing governance weaknesses.

Brand Portfolio Expansion: Building Scale Through Acquisitions

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -230 | -13 | -218 | 3 | -441.3% |

| 2024 | -42 | -9 | -59 | 3 | +52.8% |

| 2023 | -90 | -30 | -82 | 2 | +5.8% |

| 2022 | -96 | -75 | -128 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -16 | -49.7 | |

| 2024 | -12 | -6.4 | |

| 2023 | 0 | -31 | -14.4 |

| 2022 | 0 | -76 | -15.0 |

Source: SEC companyfacts cache [F1].

Waldencast’s corporate blueprint centers on growing a multi-brand platform blending established prestige with emerging skin wellness innovators. The company’s acquisition spree prominently features the Obagi Medical and Milk Makeup brands—both foundational pillars completed via a business combination—and was extended further by the July 2025 purchase of Novaestiq Corp [S1][S3]. This asset acquisition broadened Waldencast's footprint into injectable hyaluronic acid products and complementary skincare solutions.

This strategy enables Waldencast to diversify revenue streams across product categories and channels while benefiting from operational scale intrinsic to managing global beauty brands [N1]. However, acquisitions bring inherent complexity as disparate brand cultures unify under one umbrella; these challenges surfaced partially in subsequent performance shortfalls prompting impairment reviews [S1]. The company's brand-led model emphasizes maintaining distinct DNAs alongside shared operational infrastructure.

Financial Performance Analysis: From Stable Revenues to Soaring Losses

From a top-line perspective, Waldencast achieved relatively flat revenue of $272.1 million in fiscal 2025, down only slightly by 0.7% relative to the prior year $273.9 million [F1][S1]. Importantly, U.S.-focused channels witnessed growth with direct-to-consumer (DTC) sales rising by $12.6 million complemented by a $3.9 million increase in U.S. retail revenues, mitigating declines internationally where Milk Makeup’s revenues suffered due to soft consumption patterns [S1].

Despite revenue resilience, earnings collapsed dramatically; operating loss swelled from approximately $58.6 million in 2024 to a disproportional $217.5 million in 2025—a staggering increase of 271% year-over-year [F1][S1]. This deterioration was predominantly driven by a substantial goodwill impairment charge totaling $152 million related principally to the Obagi Medical ($132 million) and Milk Makeup ($20 million) units following underperformance against original acquisition forecasts [S1][F1]. Net income followed suit deteriorating from -$42.4 million to a pronounced -$229.7 million showing severe profitability contraction [F1].

Key Drivers Behind Revenue Shifts and Operating Expenses

The Cost of Goods Sold (COGS) increased 8.4% year-over-year amounting to $89.1 million vs $82.1 million in the prior period [F1][S1]. Notably this rise incorporated discrete inventory write-offs stemming from product-quality issues as well as shifts toward less favorable product and channel mixes accentuating inflationary pressures within supply chains [S6][S16].

Selling, General & Administrative expenses (SG&A) demonstrated a controlled increase of approximately 1.1%, totaling near $248 million despite intensifying marketing outlays tied to channel expansion efforts including Milk Makeup’s debut at Ulta Beauty early in the year [S1][S16]. The company reported higher logistic costs primarily due to consolidation of U.S. logistics under a single provider servicing Obagi Medical products [S16]. Further investments aimed at organizational scaling contributed coupled with reduced SEC investigation-related non-recurring expenses thanks to insurance coverage offsets [S16].

Impairment of Goodwill: Assessing the Impact on Asset Valuation

Goodwill impairment testing formed a significant focal point as poor post-acquisition performance triggered qualitative reviews that culminated in quantitative assessments flagging asset overvaluation concerns for Waldencast’s two largest reporting units: Obagi Medical and Milk Makeup [S1][F1]. This led to recognition of an unprecedented $152 million impairment charge during six months ending mid-2025 representing over 60% increase relative to the previous year’s minor impairment [$5M] [S1].

These charges are non-cash but crucially erode shareholder equity and cast doubt on the sustainability of prior acquisition assumptions about growth trajectories and synergies realized [F1]. Management noted only a marginal cushion remained between book values and fair values even post-charge, signaling vulnerability to further impairments should business forecasts worsen or external market conditions deteriorate including inflationary impacts or benchmark changes among peer valuations [S1].

Growth Prospects Supported by Product Innovation and Collaborations

On the innovation front, Waldencast’s newly launched "ALOHA Program" represents an ambitious collaboration between Obagi Medical and Alpha Aesthetic Partners designed to generate real-world evidence underpinning clinical efficacy claims for flagship products such as Obagi® saypha® MagIQ™ which recently received U.S regulatory approval bolstering its competitive moat [N1][S1]. Such partnerships enhance credibility among health professionals and consumers alike.

Additionally, Waldencast continues seeking expansion via growing its U.S DTC reach alongside selective international distribution improvements especially for Obagi-branded products offsetting weaker Milk Makeup performance abroad [S1][N1]. The acquisition of Novaestiq aims at extending the portfolio into injectables with differentiated formulas intending to capture market share within aesthetic dermatology channels [S3]. Operational focus on omni-channel penetration alongside community building is central to future topline momentum.

Constraints from Internal Controls and Financial Governance Issues

Debt-laden Waldencast faces pronounced risks stemming from identified material weaknesses in internal control over financial reporting flagged by management through 2025 assessments [S1][S10][S15]. Disclosure controls procedures were deemed ineffective at December-end thus raising concerns about potential misstatements or reporting delays adversely affecting investor trust.

Audit committee oversight is active but ongoing remediation of these deficiencies is essential both for regulatory compliance and accurate transparency during a volatile restructuring phase [S15][S23]. Persisting control gaps may elevate audit risk profiles complicating capital market access.

Capital Structure, Liquidity, and Debt Profile Analysis

Waldencast’s capital structure features substantial leverage concentrated in a secured credit facility entered mid-November 2025 known as the Lumina Credit Agreement which provides up to $225 million split between two term loan tranches with approximately $151.3 million unpaid principal outstanding end-2025 subject to steep interest around 14.8%-19% effective rates reflecting risk premiums given credit profile deterioration [S4][S5][F1].

Interest expenses surged accordingly by nearly 46% year-over-year rising above $25 million annualized burden exacerbated further by significant non-recurring debt extinguishment charges near $24.4 million linked chiefly to refinancing maneuvers closing out previous credit lines earlier in the year [S14][F1].

Liquidity exhibits adequacy reflected by a current ratio approximating 1.7x supported by cash balances near $30 million yet operating outflows remain negative causing free cash flow deficits nearing $16.25 million as capital expenditures grew modestly yet remain comparatively low at around $3.4 million indicating restrained reinvestment appetite under duress [F1][S7][S8].

Capital Allocation Discipline: ROE, Cash Flows, Dividends, and Buybacks

Return on equity (ROE) plummeted into negative territory estimated close to -49.7% correlating directly with sustained net losses deepening shareholder value erosion through continuing impairments combined with operational inefficiencies revealed across multiple fiscal years ending 2025 inclusive [F1]. Operating cash flow remained negative over recent annual periods highlighting ongoing challenges generating internal funds from core operations sufficient for sustaining growth initiatives without incremental financing risk exposure [F1].

In terms of direct shareholder returns policy, Waldencast has consistently withheld dividends since at least fiscal year 2022 emphasizing preservation of liquidity amid strategic restructuring efforts; likewise no share repurchase programs have been conducted restricting capital return flexibility given financial constraints documented throughout disclosures [F1][S13][S18][S23].

Outlook: What Investors Should Monitor Next

The path forward for Waldencast demands close scrutiny on multiple fronts:

- Post-acquisition integration effectiveness particularly melding Novaestiq into existing operational frameworks without exacerbating cost structures or dilution effects.

- Stabilization or reversal of goodwill-related impairments hinging on attainment of revised revenue goals amidst competitive pressure.

- Progress reports on remediation plans resolving long-standing material weaknesses in internal financial controls vital for auditing confidence.

- Monitoring covenant compliance related to highly leveraged credit facilities that carry elevated default risks if EBITDA or cash flow recovery falter.

- Revenue dynamics across core strategic channels especially domestic DTC expansion success versus international channel retrenchment trends.

- Execution against strategic marketing programs targeting enhanced brand awareness within targeted consumer segments. The coming quarters will reveal how effectively management can align growth ambitions with disciplined operational practices while navigating financial headwinds intrinsic to their current phase.

Disclaimer: This document presents factual analysis grounded solely on data cited from Waldencast plc's publicly available SEC filings ([F1], [S#]) and verified news releases ([N#]). It does not constitute investment advice or recommendations regarding buying or selling securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments