Chicago Atlantic REFI’s Financial Dynamics and Strategic Capital Moves in 2025

The company managed robust revenue growth and strategic liquidity enhancements while intensifying risk oversight in a challenging financial landscape.

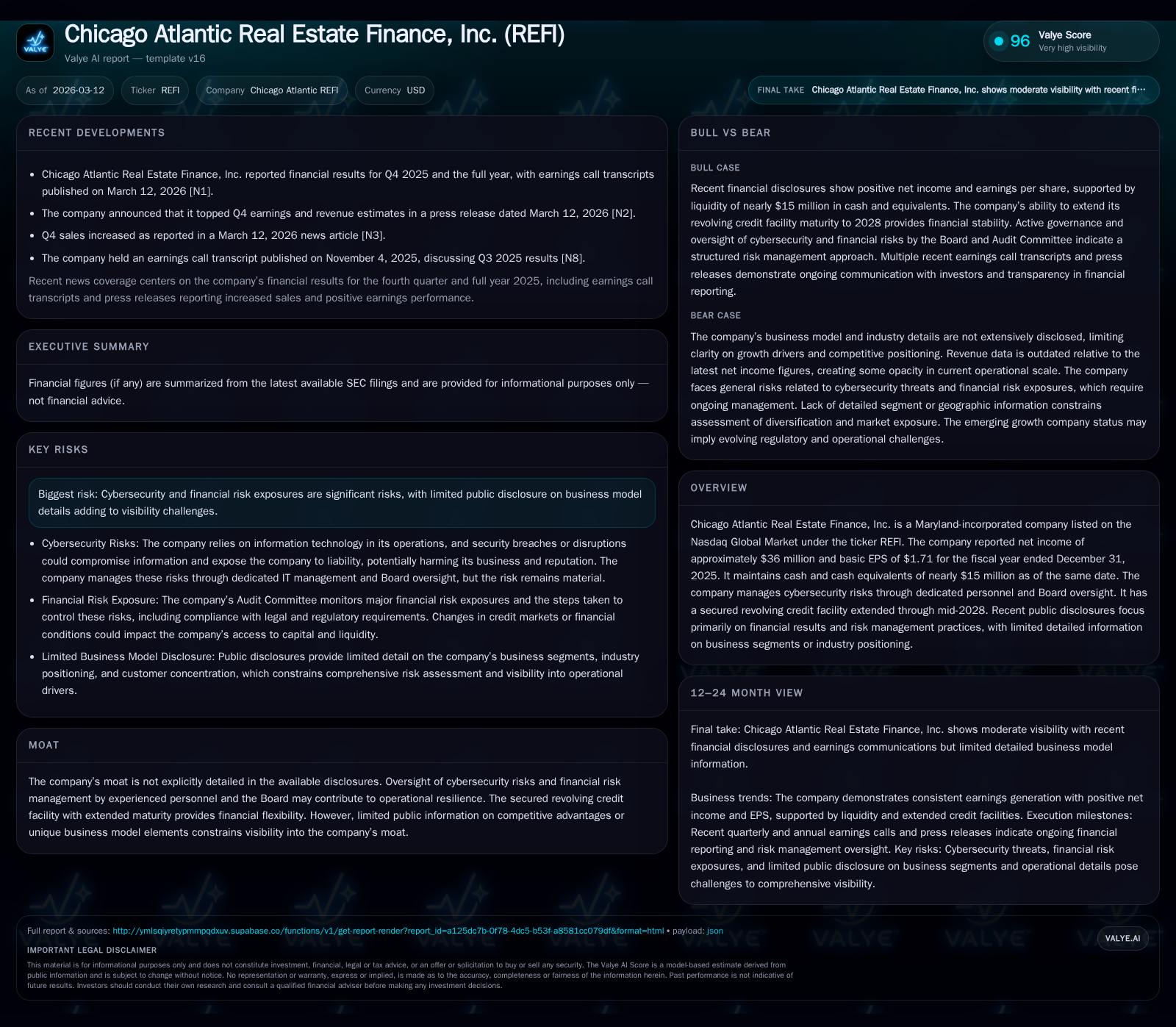

Chicago Atlantic Real Estate Finance, Inc. delivered significant revenue expansion in 2025, achieving net income of approximately $36 million with stable profitability metrics. The firm balanced capital allocation through dividends exceeding net income growth pace and sustained operational cash flows while extending its secured revolving credit facility to mid-2028. Enhanced governance protocols on cybersecurity and financial risks underpin operational resilience amid limited public disclosure on segment detail and competitive moat. Future monitoring should focus on credit utilization, liquidity events, and risk management execution.

Robust Revenue Surge Contrasted With Modest Net Income Variation

Between fiscal years 2021 and 2022, Chicago Atlantic REFI experienced an extraordinary surge in revenue from approximately $11 million to nearly $49 million—a more than fourfold increase representing a 341% year-over-year jump [F1]. This rearview glance underscores a transformative phase likely driven by portfolio expansion or increased finance activity though precise segment details remain undisclosed [S7]. Yet, this top-line acceleration saw net income exhibit restrained fluctuations: a rise from roughly $32 million in FY2022 to over $38 million in FY2023 before moderating to about $36 million in FY2025 [F1]. Such variance suggests controlled operational expenses or market pressures tempering profitability gains.

Operating cash flow mirrored this positive momentum with an uptick from $17 million in FY2022 to nearly $29 million in FY2025—a substantial annual improvement signaling healthy core earnings capacity supportive of reinvestment or distributions [F1]. Meanwhile, capital expenditures hovered near $11–14 million per annum without material upward drift, indicating measured reinvestment consistent with asset maintenance rather than aggressive expansion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 36 | 29 | 11 | -2.8% |

| 2024 | 37 | 23 | 14 | -4.3% |

| 2023 | 39 | 28 | 14 | +19.9% |

| 2022 | 32 | 17 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 44 | 18 | 11.7 |

| 2024 | 42 | 10 | 12.0 |

| 2023 | 39 | 15 | 14.2 |

| 2022 | 28 | 3 | 12.2 |

Source: SEC companyfacts cache [F1].

Data sourced from company filings spanning fiscal years ended December each year [F1].

Capital Allocation Strategy: Dividends, Cash Flows, and Credit Facilities

Chicago Atlantic REFI’s capital allocation reveals an assertive dividend policy that has grown from approximately $28 million paid out in FY2022 to nearly $44 million by FY2025 [F1][S25]. This payout trajectory outpaces the modest decline observed in net income during the last two years. The discrepancy highlights reliance on operating cash flow surpluses to bridge the gap: free cash flow—approximated as operating cash flow minus capex—totaled around $17.6 million in FY2025 supporting dividend distributions without eroding cash reserves excessively [F1].

Liquidity management is further bolstered by a secured revolving credit facility whose maturity was extended from June 30, 2026 to June 30, 2028 through an amendment executed in mid-2025 [S13][S17]. This extension provides strategic funding flexibility as the firm navigates evolving market conditions and potential capital needs while preserving balance sheet stability.

Cash and cash equivalents stood at nearly $15 million at end-2025—a comfortable buffer complementing the credit line availability [F1]. The lack of reported share buybacks suggests management prioritizes dividend returns and liquidity maintenance over repurchase programs under current circumstances.

Evolving Risk Management Focus: Cybersecurity and Financial Controls

Risk governance at Chicago Atlantic REFI includes dedicated enterprise-wide cybersecurity risk management steered by the company’s IT Manager alongside external consultants with extensive industry experience [S1][S9]. These personnel oversee strategy formulation covering policies around threat assessment methodologies and system architecture aimed at minimizing vulnerabilities.

Board-level oversight rests primarily with the Audit Committee which routinely reviews significant financial risk exposures—including those stemming from cybersecurity threats—to ensure adherence to regulatory compliance and implementation efficacy of security protocols. Annual briefings by internal teams focus on incident response effectiveness and proposed policy updates [S9].

This structure aligns with best practices typical within financially-oriented entities where layered controls mitigate operational disruption risks amidst increasing cyber threat landscape complexities.

Growth Catalysts and Constraints From Latest Public Statements

Recent earnings call transcripts highlight continued momentum on revenue fronts but refrain from granular segment commentary or geographic breakdowns limiting visibility into growth contributors or constraints beyond top-line indicators [N1][N2].

Company disclosures acknowledge material financial risks tied both to information technology systems integrity and market dynamics affecting loan portfolios but do not elaborate on mitigants beyond broad governance frameworks [S4][S9]. This conservative communication stance implies cautious outlooks amid uncertain sectoral headwinds.

Key Financial Metrics to Monitor Going Forward

Investors should track several metrics critical to appraising Chicago Atlantic REFI’s near-term trajectory: utilization rate changes on its revolving credit line will signal financing strategy shifts; free cash flow trends vis-à-vis dividends gauge sustainability of shareholder returns; any emerging cybersecurity risk incidents could impact operational continuity; regulatory developments may influence compliance costs or asset valuations [N1][S13]. Monitoring board disclosures regarding risk management adaptations will offer insights into evolving management priorities relative to external threats.

Equity Trends and ROE Insights Reflecting Operational Efficiency

As of fiscal year-end December 31, 2025 equity totaled approximately $308 million compared with net income around $36 million yielding a return on equity near 11.7%—a moderate figure within real estate finance peers suggesting steady albeit unspectacular profitability relative to capital base scale [F1].

Given the sizable asset footprint underlying this equity base typical of REIT-like structures or mortgage finance entities leveraging debt-to-equity ratios conservatively constrained by lending covenants this ROE indicates balanced leverage application without excessive risk layering.

Disclaimer: This analysis is based exclusively on publicly available information as of March 12, 2026. It reflects historical data points and disclosed management commentary without speculative forecasting or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments