Butler National's Dual Aerospace and Gaming Operations Sustain Modest Growth with Capital Investments

Butler National Corp balances aerospace product expansions and casino management to navigate regulatory and operational challenges.

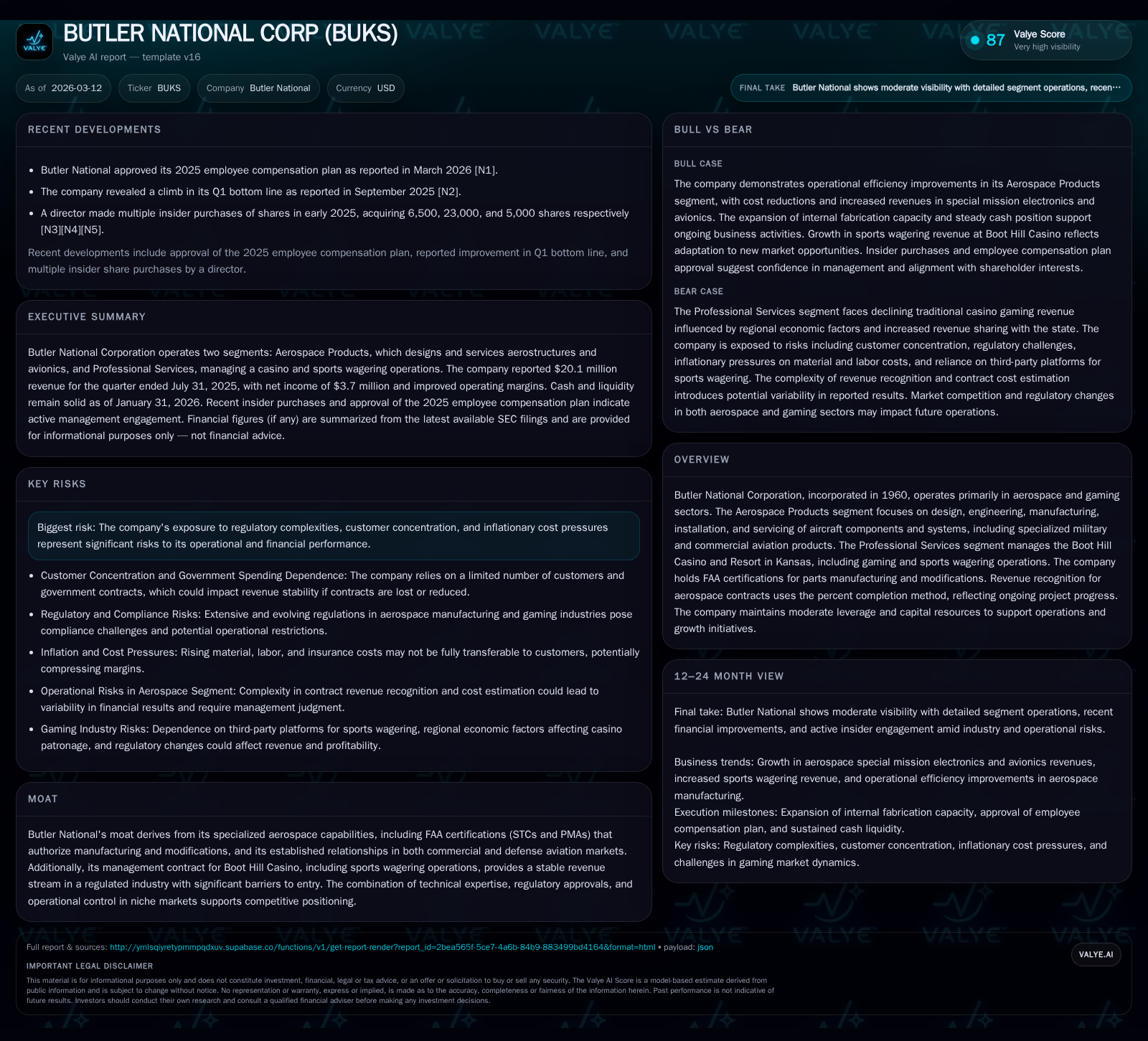

Butler National Corporation, established in 1960, operates through two core segments: Aerospace Products and Professional Services, the latter managing Boot Hill Casino in Kansas. The company delivered modest revenue growth led by the aerospace segment, supported by FAA certifications enabling specialized aircraft modifications. Despite a decline in traditional gaming revenue, sports wagering revenue increased, partially offsetting segment softness. Butler National manages inflationary pressures and customer concentration risks while investing significantly in capacity expansion and technology development. Operating income grew faster than revenue, driven by improved aerospace efficiencies, with stable cash flow supporting capital expenditures and share repurchases.

Company Overview

Butler National Corporation (ticker: BUKS), founded in 1960 and headquartered in Kansas, operates primarily in two distinct yet complementary sectors: Aerospace Products and Professional Services. The former focuses on design, engineering, manufacturing, installation, modification, repair, and servicing of aircraft components and systems that serve commercial aviation and defense markets. The latter manages Boot Hill Casino and Resort in Dodge City, Kansas—a regulated gaming operation including slot machines, table games, dining facilities, and sports wagering via an exclusive DraftKings platform.

The company's Aerospace Products hold significant competitive advantages through FAA certifications—the Supplemental Type Certificates (STCs) and Parts Manufacturer Approval (PMAs)—which authorize it to manufacture aircraft parts legally and perform modifications critical for aviation safety and performance enhancements [S10]. These certifications create high barriers to entry given stringent regulatory requirements.

Historical Performance

Financially, Butler National has exhibited steady top-line resilience combined with improving profitability metrics over the past several years. Based on SEC XBRL data [F1], total operating income increased from approximately $8.65 million in FY2023 to $16.83 million in FY2025—a compounded improvement driven mainly by the Aerospace segment’s margin efficiencies. Net income remained relatively flat at about $12.55 million from FY2024 to FY2025 after a notable jump from $4.52 million in FY2023 [F1].

The following table captures key annual financial metrics:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 13 | 18 | 17 | 8 | +0.3% |

| 2024 | 13 | 8 | 13 | 9 | +177.1% |

| 2023 | 5 | 21 | 9 | 7 | -56.4% |

| 2022 | 10 | 11 | 16 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | 10 | 19.3 |

| 2024 | 5 | -1 | |

| 2023 | 0 | 14 | |

| 2022 | 0 | 1 | 25.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not directly stated for recent years but segment data indicates modest low single-digit growth [S17]. Operating cash flow variability may relate to working capital changes.

Segment Analysis: Aerospace Products

The Aerospace segment represents the larger share of Butler’s business by revenue and is the source of growth momentum heading into recent periods [S12]. The segment recorded a solid revenue increase of roughly 7% year-over-year for the three months ended July 31, 2025 [S17]. This came on the back of:

- $1.2 million higher sales in special mission electronics attributable to improved production efficiencies through pre-building components and expanded inventories.

- $1 million rise in avionics business linked to multi-airplane upgrade contracts.

- A temporary decline of $1.5 million in aircraft modifications affected by timing shifts amid backlog reduction efforts [S9].

Cost efficiencies were notable with cost of sales falling by nearly 12%, from $7.47 million to $6.59 million for the most recent quarter reviewed [S8], driven largely by enhanced engineering execution reducing reliance on outsourced fabrication.

Additionally, Butler invested aggressively into expanding its internal fabrication capacity by acquiring an adjacent facility to its Newton airport campus—an essential move addressing shop capacity constraints from growing modification demand [S8]. This capex aligns with preserving long-term operational scalability as well as funding continued STC development vital for competitive differentiation.

Segment Analysis: Professional Services (Boot Hill Casino)

The casino management segment experienced a slight downturn with revenues declining approximately 5% year-over-year for the quarter ending July 31, 2025 [S12]. Traditional brick-and-mortar gaming revenue suffered from reduced patron visits likely due to regional economic headwinds including decreased wages/shifts at local meatpacking plants alongside inflationary effects impacting consumer discretionary spending locally [S16].

Offsetting this weakness was growth in newer sports wagering operations enabled after Kansas legalized sports betting in September 2022—the DraftKings platform generated $1.3 million compared to $1 million prior year [S12][S13]. Nevertheless, upward adjustments in state revenue sharing under the renewed fifteen-year contract further pressure net returns from this line [S16].

Costs held relatively steady despite the drop-off in patronage; however wage inflation contributed to cost pressures noted across both segments [S16][S8]. This mix contributed to a reduced professional services operating margin percentage from approximately 23% previously down to about 20% recently.

Financial Position & Capital Allocation

Liquidity remains healthy as demonstrated by a current ratio near 1.88 at January-end fiscal period reported [F1]. Cash and equivalents stood robust at nearly $36.5 million offering cushion against short-term obligations totaling roughly $35 million current liabilities also at January end.

Operating cash flow surged impressively by over 140% year-over-year reaching more than $18 million most recently compared with just over $7 million prior year driven partly by working capital management [F1] despite stable net income levels.

Capital expenditures totaled approximately $8.26 million most recently representing slight decline versus prior year but reflective of ongoing investment cycle focused on new STCs ($5M planned annually), equipment ($4–4.5M), plus facility upgrades such as building improvements ($3M planned) [S5][S13][F1].

Butler pursued disciplined capital allocation including share repurchases totaling around $2.3 million last fiscal year—a reduction compared with prior fiscal but signaling shareholder return activities continue where deemed appropriate [F1][S26]. No dividend payments are explicitly cited.

The company carries moderate leverage with prudent debt repayment actions visible ([S5]) thus maintaining manageable interest expenses slightly decreasing from previous periods (~$523k vs ~$565k) [S8]. Equity grew substantially evidencing retained earnings accumulation along with additional paid-in capital or asset revaluations raising total equity north of $65 million latest reported [F1].

Growth Outlook & Risks

While formal guidance is not disclosed ([S14]), management commentary emphasizes backlog expansion on aerospace contracts fueling optimistic future revenue recognition opportunities backed by continued STC innovations and aircraft modification programs targeting commercial turboprops such as King Airs alongside defense clients [S6][S9][N1]. Ongoing capital expenditures suggest confidence toward sustaining engineering advancements amid evolving aviation demands.

Conversely, risks remain embedded: customer concentration—particularly dependence on select government or defense programs—and exposure to regulatory changes pose upside/downside variability potential ([S19]). Inflationary pressures encompassing labor, materials and fuel costs could constrain margin leverage if not fully transferrable ([S19]).

In gaming operations, regional economic susceptibility directly impacts foot traffic while rising state tax/regulatory burdens challenge profit sustainability ([S16]). Competitive threats include third-party platform dependencies for sports wagering with evolving political dynamics adding complexity ([S19]).

Cybersecurity risks affecting both technology integration in aerospace products as well as data integrity at casino platforms also warrant attention given industry trends towards increased digitization.

Conclusion

Butler National Corp stands out for combining niche FAA-certified aerospace capabilities with regulated gaming operations—two very different but stable income sources diversified across growth profiles and risk vectors. Strong operating income growth powered mainly by aerospace efficiency gains alongside a resilient cash flow profile provides financial flexibility supporting sustained investment programs critical for future competitiveness. However, watch for developments around backlog fulfillment pace, inflation cost pass-through success, evolving state taxation on gaming revenues, as well as potential supply chain or labor limitations affecting manufacturing lead times. Investor focus should track quarterly updates post new contract awards or casino visitation trends especially within the post-pandemic recovery landscape impacting discretionary spending regions surrounding Dodge City.

This report is prepared solely for informational purposes based on publicly available data without endorsement or recommendation regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments