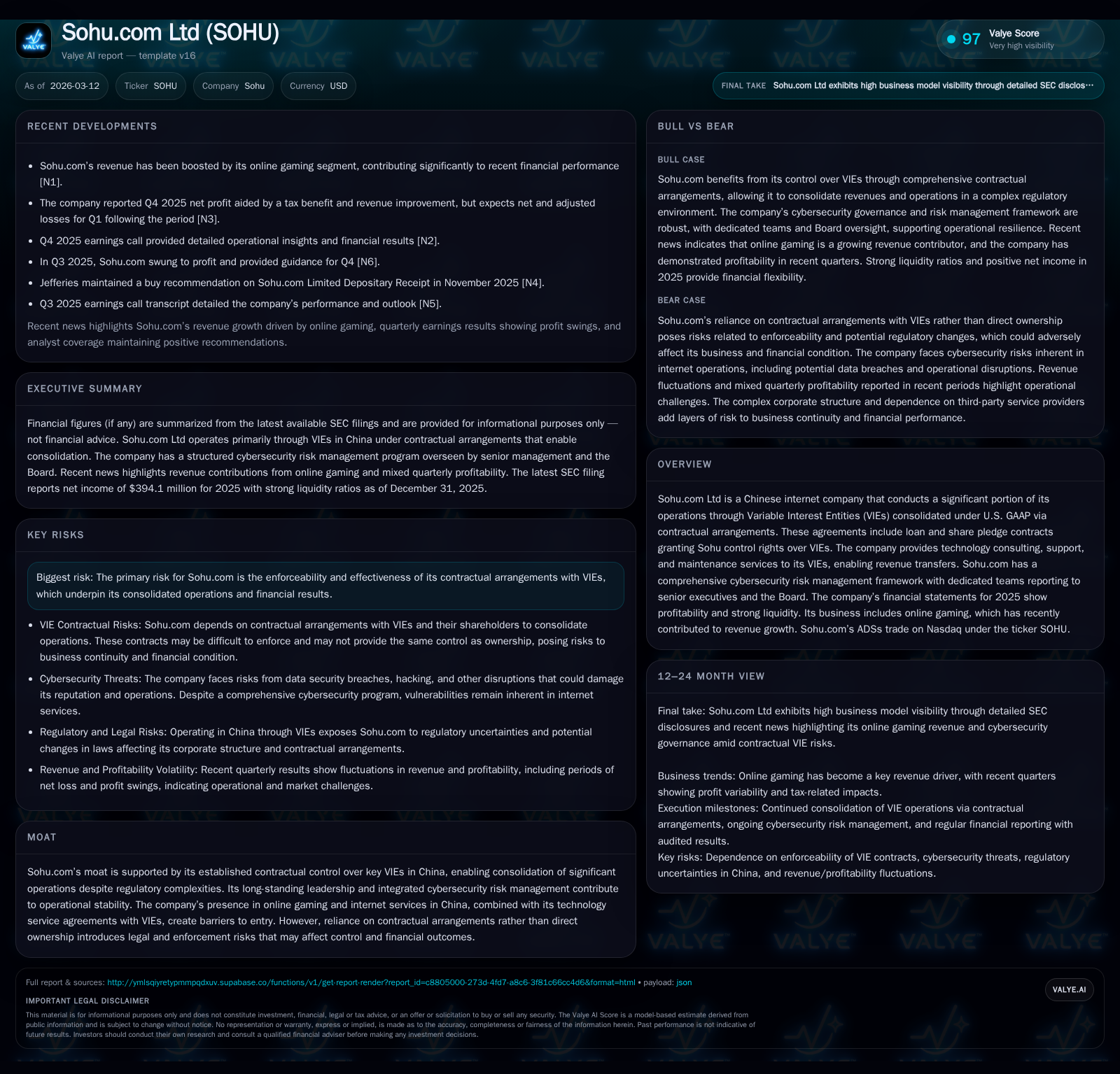

Sohu.com Ltd’s VIE-Driven Growth and Risk in Online Gaming Expansion

Sohu.com leverages contractual control over VIEs to consolidate operations, with recent profitability driven by growth in online gaming amid regulatory and cybersecurity risks.

Sohu.com Ltd operates primarily through a Variable Interest Entity (VIE) structure under U.S. GAAP, controlling its Chinese subsidiaries via complex contractual arrangements. Historically challenged by operating losses, the company returned to net profitability in 2025, largely supported by its growing online gaming segment. Liquidity remains strong with a robust current ratio and capital allocation includes significant share repurchases, while operating cash flow remains negative, reflecting ongoing investments and operational challenges. The enforceability of VIE contracts and cybersecurity threats remain prominent risk factors that could impact future results.

Company Overview and Organizational Structure

Sohu.com Ltd conducts a significant portion of its business through Variable Interest Entities (VIEs) consolidated under U.S. GAAP via exclusive contractual arrangements rather than direct equity ownership [S1][S3]. These contracts include technology consulting, service, support, maintenance agreements, as well as loan and share pledge agreements that grant Sohu.com control rights over these VIEs [S1][S12]. The company’s revenues are primarily derived from online gaming and other internet services within China.

The VIE structure introduces inherent risks related to contract enforceability under PRC law, which is a key concern for the company’s consolidated financial position [S5][S6][S13]. To manage these risks, Sohu.com holds powers of attorney from VIE shareholders allowing nominee appointments and blank transfers of equity pledges, with renewal rights for critical agreements generally at the subsidiaries' discretion [S1][S12].

Historical Performance Trends

Key annual financial metrics from fiscal years 2022 through 2025 illustrate an improving profitability trajectory despite persistent operating challenges [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 394 | -5 | -94 | 1 | +493.0% |

| 2024 | -100 | -48 | -109 | 1 | -230.1% |

| 2023 | -30 | -26 | -87 | 3 | -75.2% |

| 2022 | -17 | 32 | -1 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 54 | -5 | 30.8 |

| 2024 | 41 | -49 | -10.9 |

| 2023 | 7 | -29 | -2.9 |

| 2022 | 82 | 24 | -1.6 |

Source: SEC companyfacts cache [F1].

Highlights include:

- Operating losses have narrowed from -$109.4 million in FY24 to -$93.8 million in FY25.

- Net income turned positive sharply in FY25 to $394 million after previous losses [N3].

- Operating cash flow remains negative but improved approximately tenfold compared to FY24.

- Capital expenditures decreased significantly reflecting lower fixed asset investments.

- Equity increased notably due to retained earnings and share repurchase impacts.

- The current ratio of about 2.9 indicates strong liquidity.

Growth Drivers and Outlook

The online gaming segment is a primary driver of recent revenue improvements as noted in Q4 earnings commentary [N1][N2]. This segment benefits from Sohu.com's technology service agreements with gaming-related VIEs such as AmazGame and Changyou [S3]. While Q1 guidance anticipates adjusted net losses due to seasonal factors [N3], management remains focused on the gaming business expansion.

Renewal of exclusive technology consulting contracts underpinning consolidated revenues is critical; these agreements typically specify fees as percentages of the gross revenues of respective VIE operations and are renewable at management's discretion [S1][S3]. However regulatory scrutiny over such arrangements continues amid evolving PRC internet governance policies.

Cybersecurity risk management is embedded across business units with senior executives including CEO Charles Zhang overseeing programs supported by dedicated working groups for data security and personal information protection. The Board receives regular updates reflecting the importance placed on mitigating cyber threats [S6][S10][S15].

Capital Allocation

The company’s capital structure reflects stable resources supplemented by prudent leverage consistent with software-driven internet companies [F1][S12]. No cash dividends are planned; instead capital returns are delivered through sizable ADS repurchase programs initiated since late 2023.

Originally authorized for $80 million covering November 2023–November 2025 periods and later increased to $150 million extended through November 2026; approximately $107 million was spent repurchasing over eight million ADS shares by February 20th this year [S4]. In FY25 alone $54 million was allocated toward buybacks demonstrating continued emphasis on shareholder value alongside operational investments.

Free cash flow was negative (~-$5.34 million), reflecting marginally negative operating cash flow partly offset by reduced capital spending [F1]. This pattern is consistent with cautious reinvestment amid regulatory uncertainties impacting Chinese tech firms.

Risks and Regulatory Considerations

Primary risk centers on enforceability of VIE contractual arrangements rather than direct ownership—any failure in shareholder compliance or contract renewal could disrupt consolidated control leading to adverse financial impacts [S5][S13].

Data security breaches represent another material risk given potential reputational damage or regulatory penalties within China’s tightening cybersecurity framework [S6][S15][S18]. The company maintains comprehensive governance structures but residual risks remain.

Foreign exchange exposure also affects reported results since most revenues and assets are RMB-denominated while reporting currency is USD; RMB depreciation against USD could reduce translated revenue values despite operational stability [S16].

Monitoring Points

Key areas to watch include:

- Updates on renewal status of exclusive technology service agreements securing revenue streams from principal VIEs.

- Quarterly sequential revenue trends in online gaming reflecting competitive dynamics.

- Operating cash flow developments aligned with investment patterns.

- Any material regulatory developments affecting VIE structures or foreign listings.

- Effectiveness of cybersecurity policies amid evolving threat environments.

In summary: Sohu.com leverages contractual structures unique among Chinese internet firms with improving profitability fueled by online gaming growth. Nonetheless structural risks related to VIE enforceability alongside regulatory and cybersecurity challenges warrant close investor attention.

This report synthesizes publicly available SEC filing data alongside verified news sources without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments