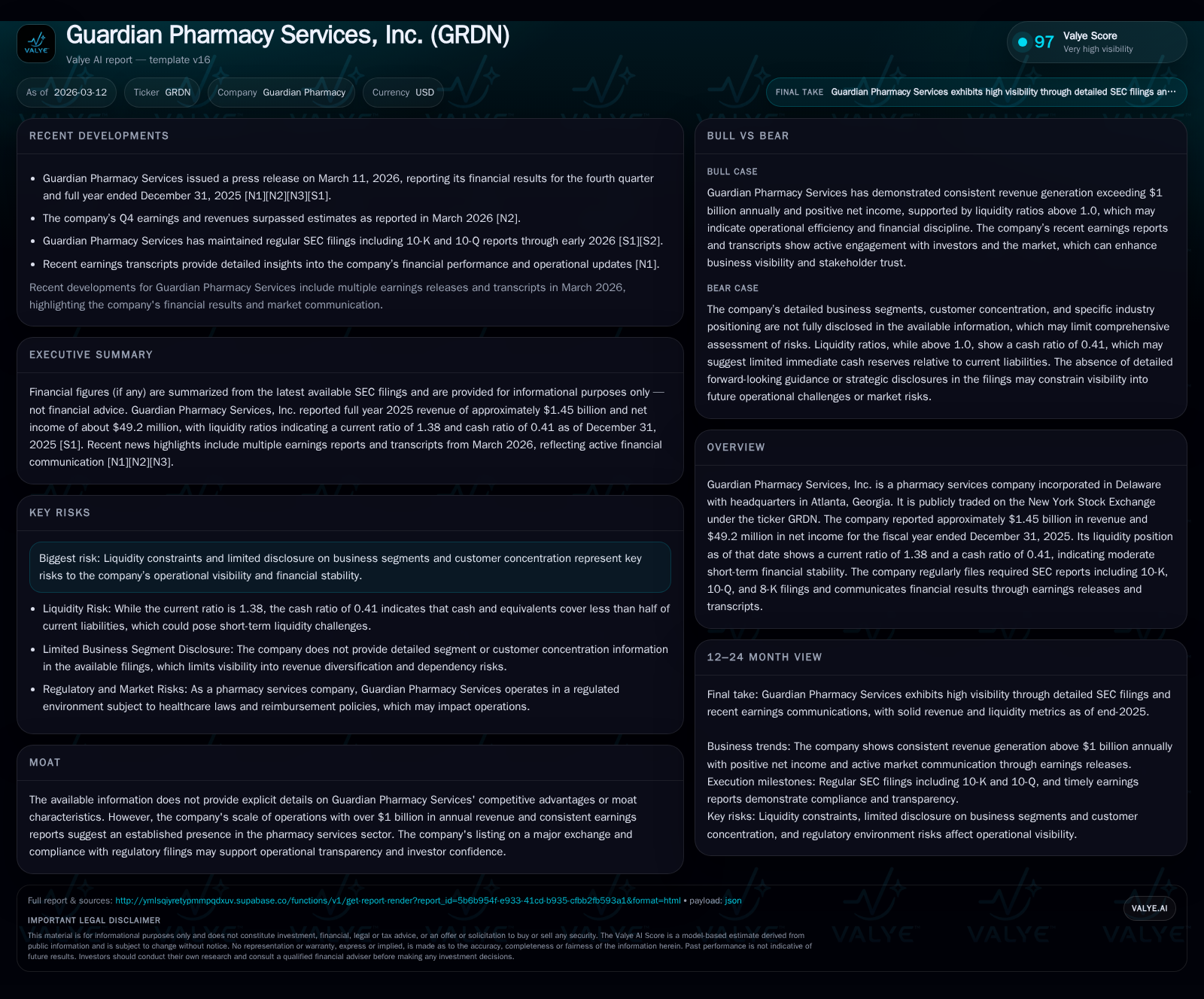

Guardian Pharmacy Services Reports Robust Profitability Despite Moderate Liquidity

Guardian Pharmacy Services posted solid profit growth in 2025, navigating moderate liquidity and operational risks within the pharmacy services sector.

Guardian Pharmacy Services, Inc. achieved $1.45 billion in revenue and $49.2 million in net income for the fiscal year ending December 31, 2025, reflecting a profitable trajectory supported by scale and operational efficiency. Despite moderate liquidity metrics—current ratio of 1.38—the company maintains financial stability amid working capital demands typical in pharmacy services. Capital allocation decisions emphasize shareholder returns via buybacks, while regulatory and disclosure risks underline the need for cautious monitoring of earnings visibility going forward.

History of Financial Growth and Operational Drivers

Guardian Pharmacy Services, Inc. demonstrated strong top-line momentum in fiscal year 2025, generating $1.45 billion in revenue as reported for the year ended December 31, 2025 [F1]. Operating income reached $72.7 million, underpinning a healthy operating margin indicative of cost discipline alongside revenue growth [F1]. Net income stood at $49.2 million, evidencing sustained profitability amid sector pressures.

While specific segment disclosures remain limited [S8], the steady upward trajectory in profits implies favorable operational leverage consistent with pharmacy services industry dynamics.

Historical performance (annual)

| FY |

|---|

| 2025 |

| 2024 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) |

|---|---|

| 2025 | 29 |

| 2024 | 55 |

Source: SEC companyfacts cache [F1].

Note: Year-over-year growth percentages are not computed due to lack of comparable prior year data.

Liquidity and Balance Sheet Strength

As of December 31, 2025, Guardian Pharmacy's current assets totaled $221.6 million against current liabilities of $160.7 million, resulting in a current ratio of 1.38 [F1]. Cash and equivalents stood at approximately $65.6 million [F1], supporting operational liquidity but indicating moderate cash buffer relative to liabilities.

Recent filings confirm manageable debt levels without excessive leverage that could constrain operational flexibility [S9],[S10],[S19]. This financial positioning supports ongoing capital expenditures alongside shareholder return initiatives.

Regulatory and Disclosure Risks

SEC filings highlight exposure to regulatory compliance complexities and limited granularity in segment-level disclosures and customer concentration data [S4],[S5],[S6],[S7],[S8]. While legal proceedings appear routine without material impact for FY2025 [S4], the partial opacity in reporting may affect investor visibility into earnings quality.

Continued vigilance is warranted given evolving reimbursement policies and industry regulation inherent to pharmacy services.

Capital Allocation: Buybacks Over Dividends

The company has prioritized capital returns through share repurchases rather than dividend payments [F1],[S14],[S15]. Buybacks totaled approximately $29 million through mid-2025 compared to $55 million observed during Q3 2024 [F1].

Return on equity is estimated at about 22.6%, reflecting effective deployment of equity capital enhancing shareholder value via retained earnings and buyback programs.

Forward-Looking Growth Outlook

Recent earnings communications emphasize opportunities for revenue expansion driven by incremental volume gains and service line diversification [N1],[N2],[S1]. Management also acknowledges potential headwinds from regulatory scrutiny and pricing pressures that may temper growth acceleration.

Pipeline visibility remains limited due to partial disclosure; however, contract expansions suggest sustainable medium-term top-line growth if effectively executed amid sector consolidation trends.

Milestones and Market Expectations Ahead

Investor focus includes the lock-up agreement expiring June 30, 2026 that restricts transfer of approximately 93% of insider-held shares—over 17 million Class A shares plus convertible Class B equivalents [S15]. This restriction currently limits share supply but may lead to stock availability fluctuations post-expiration.

Additional milestones involve updates on legal or regulatory risk resolutions and potential capital structure adjustments noted across recent quarterly filings [N3],[S3],[S14].

Summary for Investors

Guardian Pharmacy Services presents robust profitability supported by disciplined cost management and solid revenue scale alongside moderate liquidity measures. The company’s capital allocation strategy favors buybacks contributing to shareholder value with an estimated ROE near 22.6%.

Nevertheless, limited segment disclosure and regulatory complexities introduce an element of caution for investors assessing earnings quality and risk exposures. The expiration of significant insider lock-ups in mid-2026 adds a dynamic factor for stock liquidity and market sentiment.

This analysis is based solely on publicly available information as referenced herein and does not constitute investment advice or endorsement of any securities discussed.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments