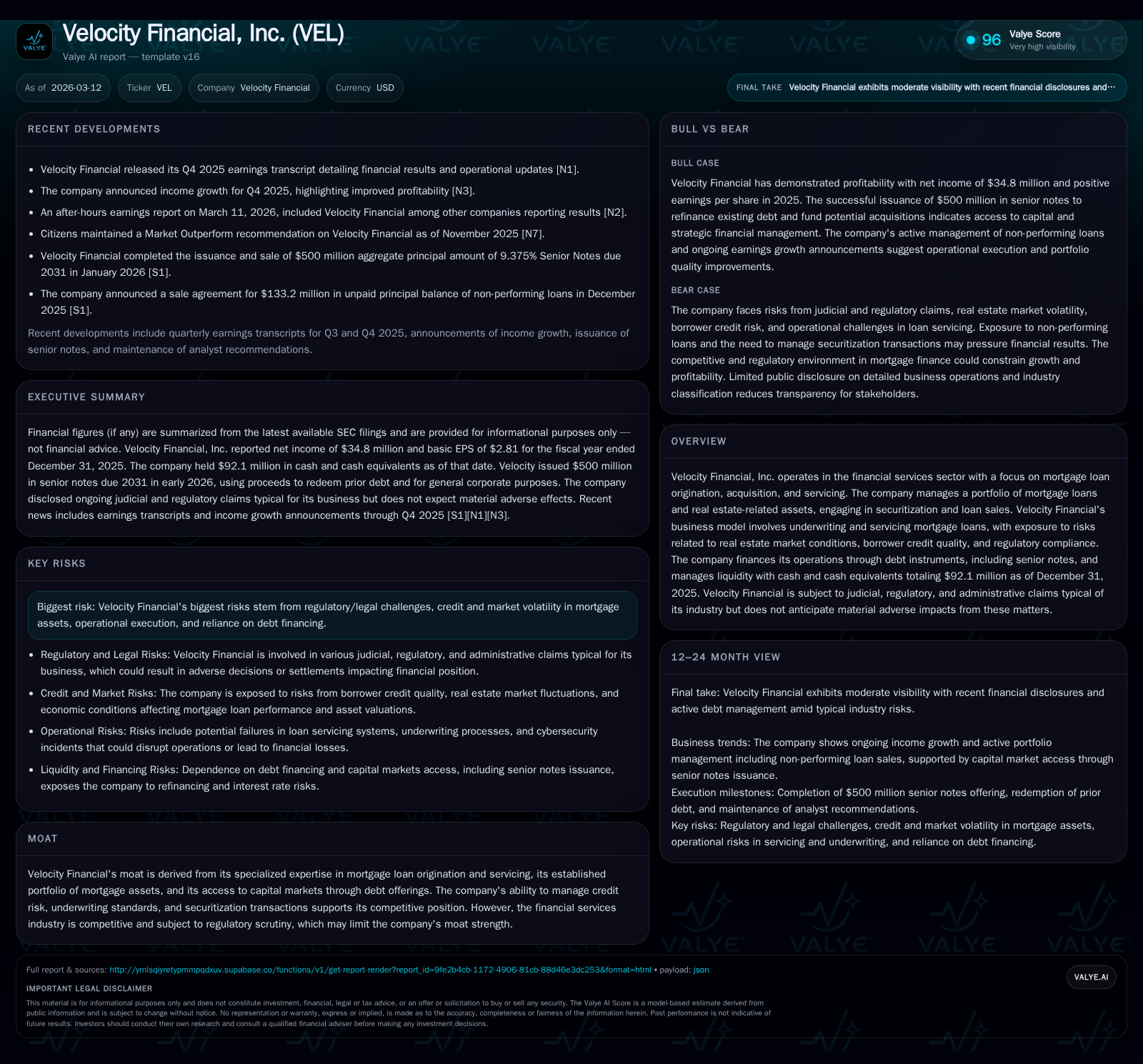

Velocity Financial Demonstrates Strong Earnings Growth Amid Capital Structure Shift

Velocity Financial’s fiscal 2025 results highlight robust profitability gains alongside liquidity and capital allocation dynamics shaped by recent debt issuance.

Velocity Financial, Inc. reported a 69% increase in net income for fiscal 2025, reaching $34.8 million, driven by mortgage loan origination, servicing, and underwriting efficiency. Despite this, operating cash flow declined by nearly 52%, reflecting timing differences in cash collections and loan securitization proceeds. The company completed a $500 million issuance of 9.375% senior unsecured notes due 2031, refinancing higher-cost secured debt and providing capital for potential acquisitions. The bond indenture imposes restrictive covenants affecting dividends, additional indebtedness, and capital allocation flexibility. Share repurchases rose notably to $7.3 million in FY2025, underscoring a shareholder return focus within debt constraints. Legal and regulatory risks typical to mortgage finance remain monitored but are not expected to materially impact operations currently. Key performance indicators to watch include loan origination volumes, delinquency trends, interest margins, and compliance with covenant terms.

Strong Net Income Growth Offset by Operating Cash Flow Decline

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 35 | 18 | 281000 | +69.0% |

| 2024 | 21 | 38 | 289000 | +18.6% |

| 2023 | 17 | 49 | 180000 | +105.1% |

| 2022 | 8 | 49 | 326000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | 18 | 5.2 |

| 2024 | 37 | 4.0 | |

| 2023 | 1 | 49 | 4.0 |

| 2022 | 0 | 48 | 2.2 |

Source: SEC companyfacts cache [F1].

Velocity Financial delivered strong profitability growth with net income rising from $20.6 million in fiscal year 2024 to $34.8 million in fiscal year 2025 — a robust increase of 69% year-over-year [F1]. This performance was supported by the company's focused mortgage loan origination, acquisition, servicing capabilities, and effective underwriting practices that maintained credit quality while enhancing operational efficiencies [N3].

However, operating cash flow declined materially from $37.8 million in FY2024 to $18.2 million in FY2025 — a near 52% decrease [F1]. This divergence likely reflects timing differences related to loan servicing cash collections and securitization tranche settlements impacting cash flow conversion.

Despite this volatility, Velocity maintains a strong liquidity position with approximately $92.1 million in cash and equivalents at the end of 2025 providing a buffer against short-term fluctuations [F1].

Mortgage Market Exposure and Risk Management Considerations

The company operates during real estate market dynamics that influence asset valuations and credit risk profiles. Its portfolio includes loans secured by transitional properties and small business borrowers that present vintage credit risks requiring ongoing underwriting adjustments [S4][S7].

Potential liabilities include repurchase obligations embedded within securitizations if credit deterioration occurs, necessitating vigilant portfolio risk management [S5]. Additionally, delays in foreclosure processes can extend loss mitigation timelines on distressed collateral [S7].

Current judicial and regulatory proceedings are viewed by management as unlikely to materially affect financial position or operations at this time; however, these remain monitored given their potential impact if unfavorable outcomes arise [S1][S4].

Capital Structure Realignment via Senior Notes Issuance

In January 2026, Velocity issued $500 million aggregate principal amount of senior unsecured notes due February 2031 bearing interest at 9.375% per annum [S6][S9][S10]. This issuance refinanced the company's outstanding 7.125% senior secured notes maturing in 2027 while also funding general corporate purposes including up to $75 million for contemplated acquisitions.

The new indenture imposes customary but significant covenants that restrict dividend payments; incurrence of additional indebtedness or preferred stock; granting liens on assets; making certain restricted payments including investments; asset sales exceeding thresholds; and transactions with affiliates [S11][S18]. These limitations constrain capital allocation flexibility until financial metrics stabilize.

Redemption options for the notes commence after February 15, 2028 with premiums declining over time adding considerations for future refinancing strategies.

Capital Allocation: Share Repurchases Amid Debt Covenants

Despite covenant restrictions on dividends and distributions under the bond indenture, Velocity increased share repurchases substantially during FY2025 to nearly $7.3 million compared with under $1 million in prior years [F1][S28][S29]. This indicates a prioritization of shareholder returns balanced against liquidity preservation needs.

Explicit dividend policies were not disclosed recently; however, the company's capital allocation appears calibrated between buybacks enhancing equity value and maintaining sufficient liquidity given market uncertainties.

Outlook: Monitoring Growth Drivers and Covenant Compliance

Key milestones include redeeming legacy senior secured notes using bond proceeds and evaluating acquisition opportunities that could alter scale and margin structure [S9][S10].

Performance indicators warranting close observation encompass loan origination volumes reflecting growth prospects; delinquency rates as early credit stress signals; interest margin trends amid rate environment shifts; and strict adherence to bond covenant requirements critical for maintaining financial flexibility [N1][N2].

In sum, Velocity Financial is positioned with strong earnings momentum but must navigate operating cash flow variability alongside a transformed capital structure featuring higher-cost unsecured debt imposing operational constraints.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments