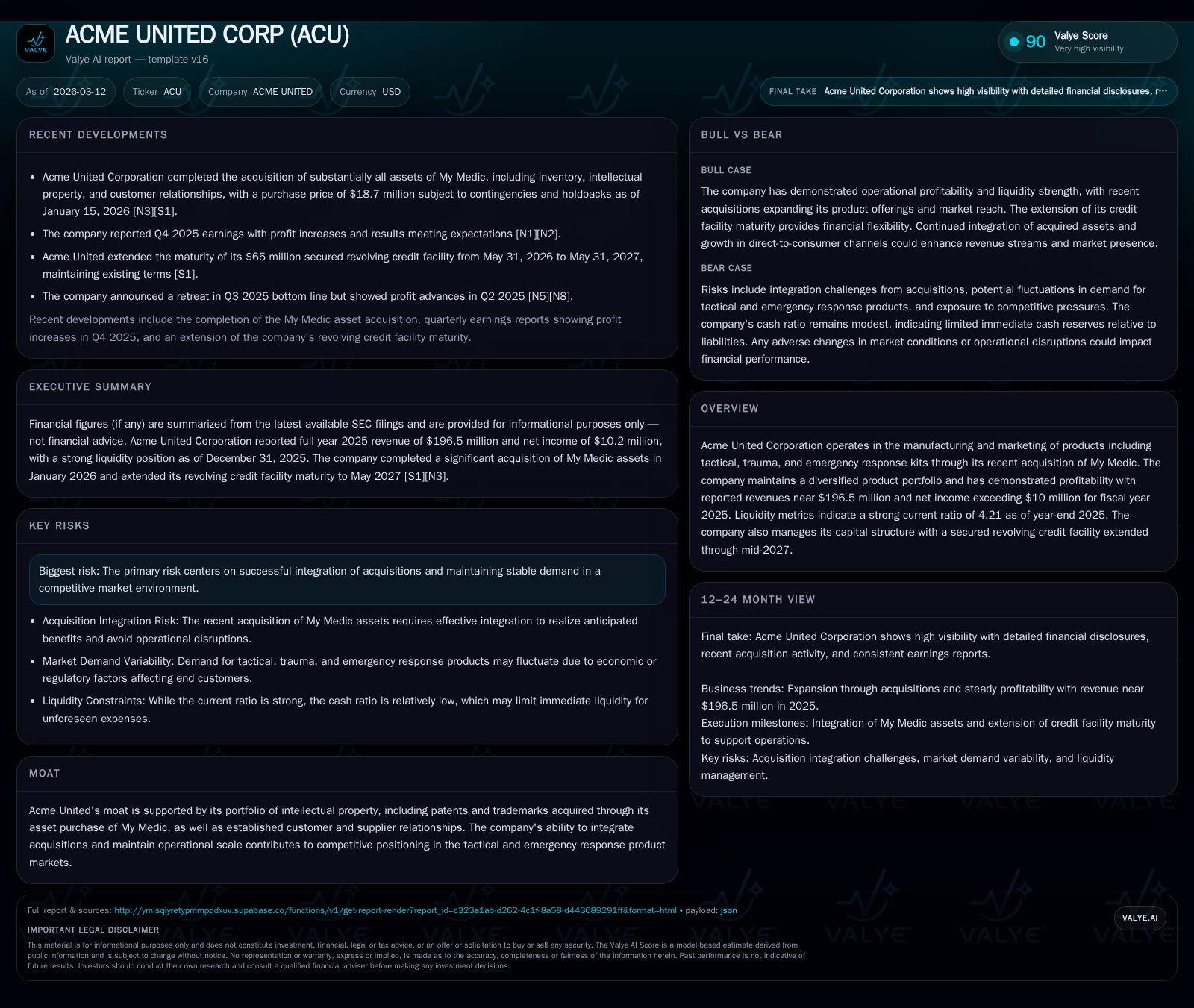

Acme United Corp's Measured Growth and Acquisition Impact Through 2025

An analysis of how Acme United’s stable financial performance and strategic acquisition of My Medic have shaped its operational and capital dynamics entering 2026.

Acme United Corporation demonstrated steady revenue growth from fiscal year 2023 through 2025, reaching $196.5 million in revenue in FY2025 with improving operating income margins. The recent acquisition of My Medic in January 2026 marks a significant expansion into tactical and emergency response products, bringing new intellectual property and direct-to-consumer channels, albeit with integration risks. Operational cash flow remains robust despite a marked increase in capital expenditures linked to growth initiatives. The company maintains strong liquidity and has extended its revolving credit facility through mid-2027, supporting both acquisitions and working capital needs. Dividends have steadily increased while share repurchases are subdued, pointing to prudent cash allocation amid expansion.

Historical Revenue Stability and Profitability Trends

Between fiscal years 2023 and 2025, Acme United recorded consistent but modest top-line growth, reaching $196.5 million in revenue by December 31, 2025 [F1]. The compound trajectory shows year-over-year gains of approximately 1.1% from FY24 to FY25, signaling a stable demand environment across its core manufacturing and marketing operations.

Operating income improved notably over this period, climbing from about $13.2 million in FY23 to roughly $14.7 million in FY25—a rise of roughly 4.1%—reflecting measured gains in operational efficiency and possibly margin enhancement within existing product lines [F1]. Net income trajectory was less linear; although net income rose slightly between FY24 ($10.0 million) and FY25 ($10.2 million), it dipped sharply in FY23 compared to adjacent years—likely attributable to discrete charges or one-off impacts noted around that period [F1].

This pattern underscores a historically resilient financial profile anchored by established product offerings and controlled cost structures in a mature sector.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 197 | 10 | 18 | 15 | +1.1% | +1.6% |

| 2024 | 194 | 10 | 12 | 14 | +1.6% | -43.7% |

| 2023 | 192 | 18 | 29 | 13 | -1.3% | +486.3% |

| 2022 | 194 | 3 | 3 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | 8 | 8.7 |

| 2024 | 2 | 5 | 9.4 |

| 2023 | 2 | 24 | 18.2 |

| 2022 | 2 | -1 | 3.8 |

Source: SEC companyfacts cache [F1].

Note: Significant fluctuations around operating cash flow and net income between FY22-FY24 highlight possible timing or non-recurring events.

Impact and Integration of the My Medic Acquisition

January 15, 2026 marked a pivotal strategic expansion for Acme United with the asset purchase agreement closing for My Medic—a supplier specializing in tactical, trauma, and emergency response kits targeting primarily direct-to-consumer channels [N1][S10]. The acquisition involved payment of $14.6 million upfront with total consideration capped at $18.7 million including contingent payments tied to revenue milestones through end-2027 [S16].

Purchased assets encompass inventory, equipment, intellectual property portfolios—encompassing patents, trademarks, trade names—and established customer/supplier relationships [S10]. These additions augment Acme’s existing portfolio well beyond traditional consumer products into critical safety gear sectors aligned with first responders and outdoor enthusiasts.

While the deal offers revenue diversification prospects through rapid medical response items with resilient demand profiles, SEC risk disclosures emphasize integration complexity as a primary challenge , underscoring potential volatility as operations merge systemically.

The inclusion of IP rights suggests an intent to leverage proprietary designs and brand equity within direct channels — a sector increasingly driven by specialized digital marketing strategies unique from Acme’s legacy wholesale focus.

Operational Efficiency and Capital Expenditure Dynamics

FY2025 financials reveal notable operational activity underlying expansion efforts: capital expenditures surged nearly 49% year-over-year to approximately $10.65 million—its highest recorded level over the recent four-year span [F1]. This uptick implies targeted investment possibly related to scaling new product manufacturing capabilities or facility enhancements post-acquisition.

Despite this step-up in capex intensity, operating cash flow grew by over half compared to prior year results ($18.2 million vs $12 million), generating free cash flow estimated near $7.6 million after accounting for capital outlays [F1]. This metrics profile demonstrates that operational execution remains robust enough to internally fund growth initiatives without immediate liquidity stress.

Elevated capex can also reflect planned modernization or automation projects typical within manufacturing firms seeking efficiency leverage while integrating new product domains.

Liquidity Strength and Capital Structure Overview

Liquidity remains a cornerstone strength for Acme United entering fiscal year-end 2025 with a robust current ratio exceeding four times (4.21), supported by substantial current assets ($96 million versus liabilities around $23 million) [F1]. Cash reserves stood at a healthy $3.6 million enabling nimble responsiveness for operational contingencies or working capital management.

Critical is the extension of its senior secured revolving credit facility totaling $65 million through May 31, 2027—the key financing backbone facilitating acquisition closes such as My Medic as well as capex outlays [S9][S11]. Terms remain consistent without material change following the amendment completed mid-2025.

Debt leverage appears conservatively managed given reported equity growth trends (~$117 million equity end-FY25), providing flexibility for future external funding if necessary while maintaining balance sheet integrity.

Dividend Policy, Shareholder Returns, and Buyback Analysis

Acme United has maintained a shareholder-friendly dividend approach with continuous annual increases from roughly $1.9 million paid in fiscal year 2022 to over $2.3 million distributed by end-2025 [F1]. This steady increment indicates confidence in cash flow sustainability.

In contrast, share repurchase activity has been absent since fiscal year 2022 when buybacks stood at approximately $1.47 million; no documented repurchases occurred thereafter [F1]. This conservative buyback stance may reflect management prioritizing cash preservation for strategic uses such as acquisitions or infrastructure investments rather than returning capital via authorized repurchases.

When considered alongside an approximate return on equity near 8.7%, these policies suggest balanced shareholder return discipline aligned with measured reinvestment strategy.

Risk Factors from SEC Filings: Acquisition Integration and Market Competition

SEC filings articulate two principal risks shaping Acme’s medium-term outlook: integration risk related to the recent My Medic acquisition and competitive market pressures within tactical/emergency product segments [S2][S4][S5].

Integration risk includes challenges in assimilating disparate operational systems, retaining key customer relationships, managing contract transitions, maintaining supply chain continuity, and achieving expected synergies without material margin dilution [S16]. Sector vernacular emphasizes "customer retention" volatility during mergers and "competitive pricing pressure" arising from entrenched rivals serving specialized markets.

Competition dynamics are notable because tactical trauma supplies often require certifications or adherence to emergency response protocols limiting commoditization but exposing players like Acme to boutique competitors with niche branding advantages.

Acme currently discloses no significant legal proceedings indicating clean regulatory standing but must maintain vigilance given evolving product standards common within safety equipment sectors [S5].

Forward-Looking Considerations: What to Watch

With explicit management guidance scant across filings, monitoring execution against several milestones is vital:

- Revenue contributions from My Medic asset lines over coming quarters will signal successful integration impact on top line and EPS prospects [N1][N2].

- Renewal or repricing terms of revolving credit facility post-2027 will affect financial flexibility for potential incremental acquisitions or working capital cycles [S3].

- Observable shifts in capex allocation may indicate either capacity ramp-up success or reallocation amid strategic pivots.

- Broader market demand trends within direct-to-consumer emergency trauma kits could influence organic growth beyond base business given shifting consumer behavior towards preparedness products.

Sector-specific supply chain nuances remain pertinent; disruptions could affect inventory turn rates given components sourcing constraints typical across specialized medical accessories distribution channels.

Disclaimer: This analysis synthesizes publicly available financial data, SEC filings, and news sources without providing investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments