Verrica Pharmaceuticals' Growth Hinges on YCANTH Expansion and Pipeline Advancement Amid Commercial Execution Risks

FDA-approved YCANTH drives initial revenues while clinical and commercial execution remain critical for Verrica's future trajectory.

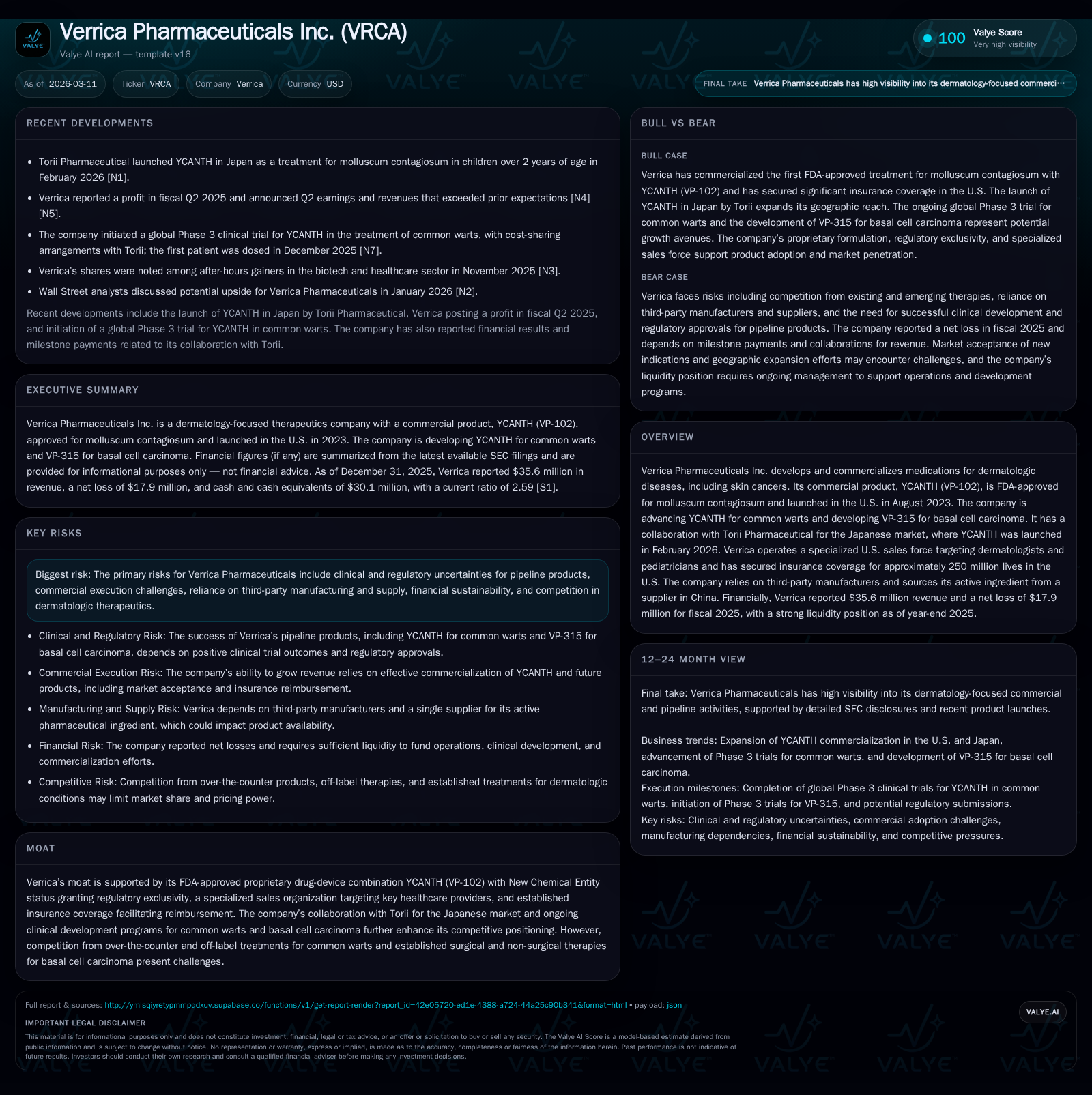

Verrica Pharmaceuticals reported $35.6 million in revenue for fiscal 2025, primarily driven by the recent U.S. launch of YCANTH (VP-102) for molluscum contagiosum, complemented by its introduction in Japan via a partnership with Torii Pharmaceutical. Despite a net loss of $17.9 million, the company has improved operating results from prior years, underpinned by regulatory exclusivity and broad insurance coverage. Growth catalysts include expanding indications for common warts, advancing the oncolytic peptide VP-315 for basal cell carcinoma, and leveraging international partnerships. Challenges include supply risks from contract manufacturing dependencies, reimbursement variability, and ongoing litigation. Cash reserves of $30.1 million and a current ratio of 2.59 provide liquidity resilience amid continued negative operating cash flow.

Company Overview and Product Portfolio

Verrica Pharmaceuticals Inc. develops and commercializes dermatologic therapeutics addressing high unmet needs such as molluscum contagiosum and skin cancers[S1]. Its sole commercial product is YCANTH (VP-102), an FDA-approved topical drug-device combination containing cantharidin for treating molluscum in patients aged two years and older. The product gained FDA approval in July 2023 and launched commercially in the U.S. by August that year.

The company is advancing YCANTH for an additional indication targeting common warts and developing VP-315 (ruxotemitide), an injectable oncolytic peptide candidate focused on basal cell carcinoma (BCC). Strategic partnerships include a licensing agreement with Torii Pharmaceutical enabling YCANTH's launch in Japan in February 2026[N1].

Historical Financial Performance

FY2025 marked Verrica's first full fiscal year generating product revenue following YCANTH's approval and launch. Total revenue reached $35.6 million for the year ended December 31, 2025[F1]. Prior years showed no significant product revenues.

Losses have contracted sharply: net loss narrowed to $17.9 million in FY2025 from $76.6 million in FY2024 and $67.0 million in FY2023[F1]. Operating loss improved similarly from about $65.9 million negative in FY2024 to approximately $12.2 million negative in FY2025[F1]. These improvements reflect initial commercial scale-up rather than contributions from pipeline products.

Operating cash flow remains negative but shows improvement: cash outflow was approximately $17.6 million in FY2025 compared to larger outflows exceeding $60 million in FY2024[F1]. Capital expenditures were negligible at zero dollars in FY2025 after modest spending in prior years[F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -18 | -18 | -12 | 0 | +76.6% |

| 2024 | -77 | -61 | -66 | 27000 | -14.3% |

| 2023 | -67 | -39 | -66 | 362000 | -173.6% |

| 2022 | -24 | -19 | -21 | 302000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -18 | -72.3 |

| 2024 | -61 | 776.7 |

| 2023 | -39 | -339.0 |

| 2022 | -19 | -61.2 |

Source: SEC companyfacts cache [F1].

Commercial Strategy and Market Access

Verrica deploys a specialized sales force of approximately 40 representatives targeting pediatric dermatologists, dermatologists, pediatricians, and select primary care providers—key prescribers of molluscum treatments[S22]. Marketing efforts emphasize YCANTH’s unique FDA-approved status as an HCP-administered therapy.

Insurance coverage reportedly extends to approximately 250 million U.S. lives across commercial plans and government programs including Medicaid[S26]. Reimbursement facilitation advanced with receipt of a dedicated CMS HCPCS Level II J-code (J7354) granted in April 2024 specifically for YCANTH topical administration[S26], easing provider billing.

Physician acquisition channels include specialty pharmacy “white bag” models or buy-and-bill wholesale distribution approaches. To streamline patient access further, Verrica launched YCANTH-Rx—a centralized non-dispensing pharmacy triaging prescriptions irrespective of insurance type.

Pipeline Prospects and Developmental Priorities

The pipeline focuses on expanding YCANTH’s label to include common warts—a widespread condition lacking FDA-approved therapies—and advancing VP-315 as an injectable immuno-oncology candidate for BCC treatment. Clinical data supporting these developments remain pending as Verrica advances regulatory submissions.

Manufacturing and Supply Chain Considerations

Verrica outsources manufacturing without owned production facilities relying on contract manufacturers domestically and internationally[S26]. Cantharidin API is sourced mainly from a China-based supplier previously protected by an exclusivity agreement tied to purchase volume thresholds; this exclusivity expired due to unmet purchase minimums around late 2024 or early 2025 introducing supply concentration risk.[S26]

Maintaining consistent quality under cGMP standards across multiple contract manufacturers remains operationally challenging given natural product sourcing complexities.[S1][S26]

Legal Environment and Risk Profile

Ongoing securities class action litigation alleges insufficient disclosure regarding manufacturing deficiencies at contract facilities affecting regulatory approvals during earlier periods[S27]. Recent court rulings granted class certification indicating prolonged legal proceedings ahead.

Stockholder derivative lawsuits tied to related fiduciary duty claims remain pending. These legal matters may pose reputational or financial risks though management does not currently anticipate material impacts.

Compliance obligations span federal healthcare laws including Anti-Kickback Statute enforcement risk, False Claims Act exposure, HIPAA privacy/security requirements, and transparency mandates such as the Physician Payments Sunshine Act.

Capital Structure, Liquidity & Returns Profile

As of December 31, 2025 Verrica reported cash and cash equivalents totaling approximately $30.1 million against current liabilities of about $16.4 million yielding a current ratio near 2.59—reflecting adequate short-term liquidity but reliance on financing or operational improvements to sustain runway[F1][S4][S10][S23]. Stockholders’ equity stood positive at roughly $24.7 million reflecting accumulated deficits offset by paid-in capital injections[F1].

The company maintains a credit facility established mid-2023 sized at $50 million providing liquidity support; principal repayments began January 2025 triggered by revenue covenant thresholds not met per loan terms which may constrain near-term flexibility.[S4][S10]

Return metrics illustrate ongoing investment phase dynamics: approximate return on equity based on FY2025 net loss over equity is negative around -72% driven by commercialization scale-up costs alongside R&D investments supporting pipeline advancement.[F1]

No dividends or share repurchases have been declared consistent with typical biotech growth-stage capital conservation.

Industry Context & Outlook Considerations

Dermatologic therapeutics target large underserved patient populations particularly pediatric cases of molluscum or common warts where off-label treatments prevail. Proprietary drug-device combinations like YCANTH create regulatory complexity barriers supporting exclusivity value though generic compounding risks remain latent if policies shift.[S24]

BCC treatment trends increasingly incorporate injectable immunotherapies alongside surgery or topical agents making VP-315’s clinical success dependent on demonstrated efficacy and safety differentiation.

Drug pricing pressures persist broadly with legislative actions such as Medicare Drug Price Negotiation Program impacting single-source drugs, while payor fragmentation requires nuanced reimbursement strategies involving PBMs and managed Medicaid programs.

Key forward milestones include adoption trajectory monitoring for YCANTH post-launch relative to estimated addressable morbidity (~6 million prevalent U.S. cases), clinical data readouts supporting common wart indication expansion potential,and progression updates on VP-315 development targeting BCC indications. Supply chain stabilization efforts remain critical given dependency on limited API vendors while resolution progress on ongoing litigation will influence capital market perceptions. Reimbursement environment evolution including CMS coding changes or broader policy reforms affecting patient out-of-pocket costs warrant close attention.

Conclusion

Verrica Pharmaceuticals is navigating early commercialization phases generating initial revenues from its novel YCANTH platform while confronting challenges typical of emerging biopharma firms including sustained operating losses driven by commercialization investments and pipeline development costs.[F1] FDA-granted exclusivity status combined with broad insurance coverage supports foundational market positioning enabling initial penetration efforts. International expansion via Torii introduces geographic diversification albeit still nascent relative to dominant U.S operations.[N1] Future growth depends heavily on effective execution driving physician uptake alongside successful translation of pipeline assets into additional approved indications or products. Financial discipline managing liquidity combined with strategic capital planning remains essential given ongoing cash flow deficits despite recent improvements.[F1] Legal proceedings introduce uncertainty though management currently views associated risks as manageable. Regulatory compliance complexity applies keenly given proprietary drug-device nature requiring continued operational diligence over coming periods. Overall prospects reflect typical early-commercial biotech risk-return profiles combining innovation potential tempered by execution complexities.

This report summarizes publicly available information as of March 11, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments