Tandy Leather Factory’s 2025 Transition: Earnings, Asset Sales, and Operational Shifts

Examining how asset divestitures and operational changes shaped Tandy Leather's financial profile and growth outlook in 2025.

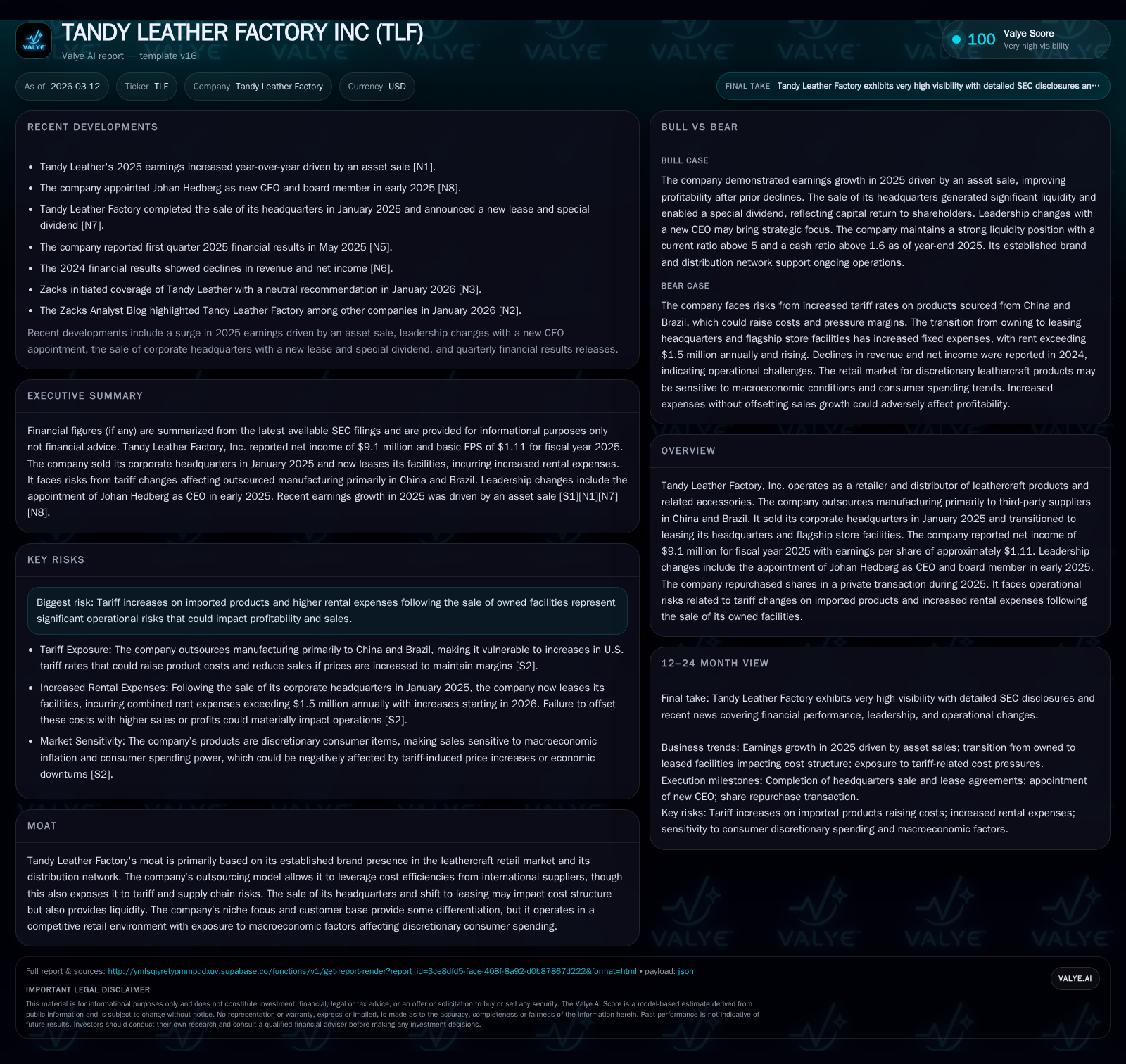

Tandy Leather Factory reported a net income of $9.1 million in fiscal 2025 driven primarily by the sale of its corporate headquarters, contrasting with an operating loss of $0.96 million reflecting operational pressures. Revenue grew modestly by approximately 1.7%, but escalating import tariffs on outsourced products from China and Brazil, combined with increased leasing costs following asset sales, compressed profitability. New CEO Johan Hedberg steered strategic adjustments including share repurchases and managing the balance between capital reinvestment and shareholder returns. Going forward, tariff developments, lease cost escalations, and operational efficiencies will be critical to sustaining growth amid a competitive discretionary retail environment.

Earnings Surge Amid Asset Divestitures: The 2025 Picture

Fiscal year 2025 marked a transformative period for Tandy Leather Factory as it recorded net income of $9.1 million despite an operating loss near $1 million [F1]. This divergence hinges chiefly on the company's strategic sale of its corporate headquarters and related properties early in the year [N1][S1]. The infusion of liquidity from these asset disposals bolstered the bottom line through one-time gains, temporarily masking underlying operating challenges.

While operating results were subdued, the capital generated allowed Tandy Leather to reposition financial resources strategically amid rising costs and structural shifts.

Revenue Stability and Operating Challenges: Unpacking the Financials

Revenue for 2025 showed a modest increase of approximately 1.7% year-over-year — continuing a trend of relative top-line stagnation from prior periods [F1]. However, this modest growth belies growing headwinds impacting margins.

The transition from ownership to leasing facilities introduced new fixed expenses that compressed operational profitability [S2][S4]. Concurrently, tariff escalations on imports sourced primarily from China and Brazil began eroding gross margins; these duties elevated cost bases forcing considerations around price adjustments which risk dampening demand.

Together these factors drove operating income into negative territory (-$963K) despite maintaining revenue traction [F1][S4].

Tariffs and Leasing Costs: Emerging Constraints on Profitability

The company faces significant pressure from increased tariffs on imported goods manufactured abroad, particularly those sourced from China and Brazil [S2][S4]. These tariffs could necessitate retail price increases which carry risk for volume attrition given the discretionary nature of leathercraft products.

Moreover, closing ownership of its Fort Worth headquarters has led to substantial leasing costs, with combined initial rent exceeding $1.5 million annually starting in 2025 and scheduled annual escalations thereafter [S2][S5]. This shift markedly alters fixed-cost structures compared to prior real estate ownership economics.

This complex interplay between import charges and leasing expenses elevates operational leverage risks for Tandy Leather amidst volatile external factors.

Supply Chain Outsourcing Risk and Market Positioning

Tandy Leather’s business model revolves around outsourcing product manufacturing predominantly to third parties in China and Brazil [N1][S4]. This strategy enables cost efficiencies critical in a competitive retail segment but simultaneously exposes the firm to supply chain fragilities amplified by geopolitical trade tensions.

Despite such risks, Tandy maintains a defensible niche through its established brand recognition within leathercraft retail coupled with an extensive distribution network — elements that constitute core moat factors amid broader discretionary spending cycles.

Leadership Changes and Strategic Priorities Under Johan Hedberg

The early-2025 appointment of Johan Hedberg as CEO marks a pivotal governance shift aimed at navigating operational challenges revealed in recent filings [N1][S8]. Hedberg's leadership focuses on balancing liquidity derived from asset sales with prudent capital deployment decisions including enhanced shareholder value initiatives.

His tenure coincides with critical restructuring steps such as transitioning facility management toward leasing models and mitigating tariff-induced cost escalations.

Capital Allocation Moves: Share Repurchases Versus Investment Needs

Reflecting new capital deployment priorities under Hedberg’s guidance, Tandy Leather repurchased shares in a private transaction totaling approximately $1.36 million in 2025 — a notable increase compared to negligible activity in prior years [F1][S8][S19].

However, this return policy contrasts with increased capital expenditure outlays which rose steeply to $7.53 million for the year (up over 150% YoY), possibly signaling investments tied to operational restructuring or technology upgrades aimed at offsetting rising costs elsewhere [F1][S19].

Operating cash flow was negative at -$556K while free cash flow (operating cash flow minus capex) swung to an outflow near -$8 million marking liquidity pressures beneath headline profits [F1].

This reflects an ongoing capital deployment tradeoff where maintaining competitiveness demands fresh spending even as shareholder distributions resume cautiously.

Key Milestones Ahead: What Investors Should Monitor

Looking beyond historical results, several milestones are crucial trackers for assessing Tandy’s ability to stabilize growth:

- Progress on negotiating or adapting to tariff regimes impacting import duties from key supplier countries.

- Lease renegotiation outcomes or efficiencies realized in response to elevated leasing costs beyond initial $1.5 million estimates.

- Operational improvements under CEO Hedberg addressing negative operating leverage trends.

- Market reception of any product price adjustments passed onto consumers amid inflationary pressures.

- Cash flow recovery trajectories balancing capex demands with cash generation enhancements. These variables collectively determine if current strategic pivots crystallize into sustainable earnings momentum or if margin pressures persist [N1][S2].

Cash Flow Dynamics and Return On Equity Analysis

Despite reported net income gains heavily influenced by one-time asset sale profits, core cash flow generation faced headwinds manifested by negative free cash flow totaling approximately -$8 million after accounting for capex spikes [F1]. Operating cash generation declining sharply (-112% YoY) underscores underlying business operations require efficiency gains.

Nonetheless, return on equity is relatively robust at about 17.3%, owing primarily to large net income driven outside regular earnings streams [F1][S15]. This juxtaposition marks a cautionary tale where accounting profitability contrasts underlying operating fragility requiring close scrutiny going forward.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 9 | -1 | -1 | 8 | +1000.6% |

| 2024 | 1 | 5 | 1 | 3 | -78.1% |

| 2023 | 4 | 5 | 4 | 1 | +207.1% |

| 2022 | 1 | 1 | 1 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1363000 | -8 | 17.3 |

| 2024 | 0 | 2 | 1.4 |

| 2023 | 11000 | 4 | 6.7 |

| 2022 | 1798000 | 1 | 2.4 |

Source: SEC companyfacts cache [F1].

Table shows key financial metrics highlighting revenue growth stagnation alongside volatile earnings impacted sharply by non-operational asset transactions.

This analysis is based solely on publicly filed documents and recent news reports as cited; it does not constitute specific investment recommendations or forecasts. Readers should consider comprehensive due diligence including market conditions before forming conclusions about Tandy Leather Factory's financial future.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments