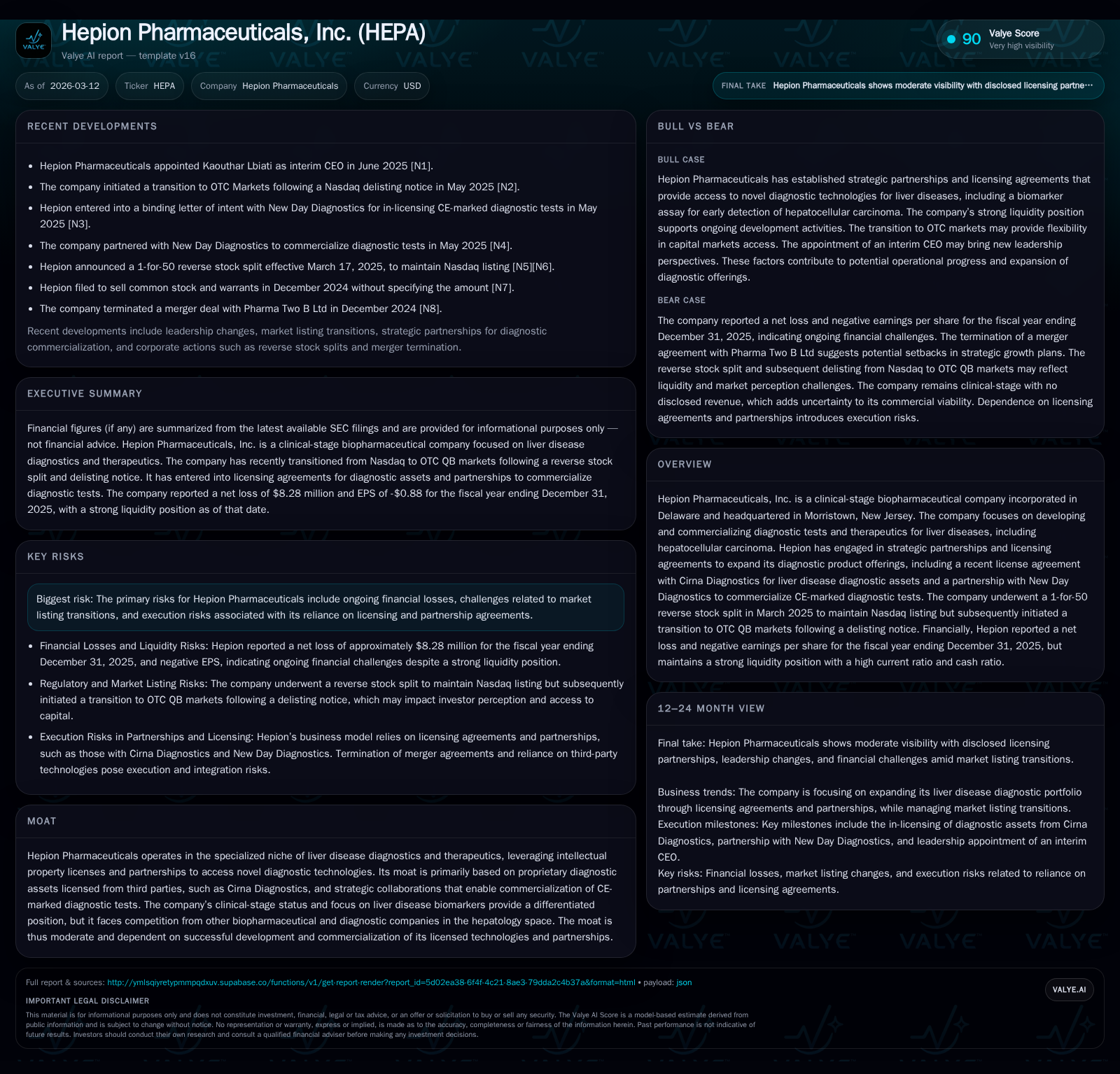

Hepion Pharmaceuticals' Strategic Pivot to Liver Disease Diagnostics Amid Financial Constraints

Facing continued operating losses and liquidity challenges, Hepion Pharmaceuticals shifts focus from therapeutic development to licensing diagnostic tests for liver diseases.

Hepion Pharmaceuticals, initially focused on developing therapeutics for chronic liver diseases, has transitioned to licensing and commercializing diagnostic products due to sustained net losses and limited capital. The company wound down its clinical trial for its lead drug candidate rencofilstat in 2024 due to funding shortfalls and has since acquired rights to several CE-marked diagnostic tests from New Day Diagnostics as well as novel biomarker assays from Cirna Diagnostics. Despite improved operating results in 2025, Hepion's runway extends only into Q3 2026 absent additional financing. Capital allocation is prioritized toward licensing expenditures with no dividends or buybacks reported. Future growth hinges on commercialization success of licensed diagnostics and securing further capital [F1, S1, S9, S13].

Company Background and Historical Financial Performance

Hepion Pharmaceuticals, Inc., based in Morristown, New Jersey, was originally focused on developing therapeutics for chronic liver diseases. Its lead candidate was rencofilstat (formerly CRV431), a cyclophilin inhibitor targeting liver fibrosis pathways. However, funding constraints led to the wind-down of its ASCEND-NASH clinical trial in April 2024 [S1].

Financial data indicate persistent operating losses since inception. Operating income improved significantly from a loss of approximately $45 million in FY2022 to about -$4.16 million in FY2025 — a roughly 78% improvement year-over-year from FY2024 to FY2025 [F1]. Net losses remained substantial at approximately -$8.28 million in FY2025 compared to -$13.19 million in FY2024.

Operating cash flow also remained negative but improved by approximately 82% between FY2024 (-$18.2 million) and FY2025 (-$3.27 million), reflecting efforts to reduce burn rate during financial pressures. Capital expenditures were minimal and stable around $14k annually through recent years.

Equity experienced volatility: it declined sharply from $7.28 million at end-2023 to negative $1.86 million at end-2024 before recovering to $2.67 million at end-2025. This fluctuation reflects impairments associated with discontinued therapeutic assets.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | -3 | -4 | +37.3% | |

| 2024 | -13 | -18 | -19 | 14304 | +73.0% |

| 2023 | -49 | -41 | -48 | 14304 | -15.9% |

| 2022 | -42 | -35 | -45 | 16336 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -310.3 | |

| 2024 | -18 | 708.0 |

| 2023 | -41 | -672.0 |

| 2022 | -35 | -84.6 |

Source: SEC companyfacts cache [F1].

Table: Selected Financial Metrics for Hepion Pharmaceuticals (Source: [F1])

Strategic Shift Toward Diagnostics Licensing

Following the cessation of clinical activities for rencofilstat due to lack of funding [S1], Hepion pivoted towards acquiring diagnostic product rights which require lower capital investment than drug development.

In May 2025 the company licensed CE-marked diagnostic tests for celiac disease, respiratory multiplex panels (COVID/Influenza A/B/RSV), Helicobacter pylori detection and hepatocellular carcinoma from New Day Diagnostics LLC. The initial consideration included approximately $525k cash plus equity shares valued at $270k with potential milestone payments up to $17.15 million contingent on regulatory approvals and sales performance as well as royalty payments based on net sales [S1].

In February 2026 Hepion executed an intellectual property license agreement with Cirna Diagnostics LLC granting access to novel biomarker assays detecting mutant circulating tumor RNA for early diagnosis of hepatocellular carcinoma in high-risk patients. The agreement includes upfront payments ($50k), patent expense coverage obligations and milestone payments up to $2.35 million plus sales milestones up to $4.5 million with royalties payable in the low single digits [S13].

These transactions underscore Hepion’s strategic repositioning towards diagnostics leveraging third-party technologies rather than internally developed therapeutics.

Liquidity Position and Capital Allocation

Despite improvements in operating metrics during FY2025 [F1], Hepion remains financially constrained. Management disclosed that available cash resources are expected to be exhausted by Q3 2026 absent new financing [S1]. This has led to slowed clinical trial timelines and an emphasis on preserving liquidity.

The balance sheet shows a strong current ratio (~10.25) driven by current assets exceeding current liabilities substantially; however this likely reflects non-cash assets such as receivables or deposits rather than significant liquid cash reserves at year-end 2025 [F1].

Capital allocation has prioritized licensing arrangements over shareholder returns; no dividends or share repurchases have been reported during recent periods [F1,S9]. This conservative approach aligns with the company’s need to conserve resources while investing selectively in diagnostic assets expected to drive future revenue.

Governance and Leadership Updates

Leadership changes accompanied this transition phase: CFO John Brancaccio resigned effective June 30th 2025 citing personal reasons [S16]. Dr. Kaouthar Lbiati was appointed interim CEO June 16th 2025 and formally named CEO January 8th 2026 under an employment agreement with a base salary of $350k plus performance bonuses tied to financing milestones or change-of-control events [S14,S15,S17].

The Board consists of four directors reelected at the June 12th annual meeting with advisory votes on executive compensation passed without significant opposition [S12].

Outlook and Considerations

Hepion operates within a competitive hepatology diagnostics market where early detection of liver fibrosis progression and liver cancer remains an unmet need.

The shift from therapeutics development toward diagnostics licensing reduces capital intensity but places execution risk on successfully commercializing licensed products across Europe initially via CE-mark approvals.

Future growth depends heavily on regulatory acceptance of these diagnostics alongside effective marketing partnerships to achieve sales milestones embedded in license agreements.

Persistent funding needs remain critical; without successful capital raises or strategic partnerships soon the company’s ability to sustain operations beyond late-2026 is uncertain.

Investors should monitor upcoming filings for updates on commercialization progress and financing initiatives that will materially influence Hepion’s trajectory.

Conclusion

Hepion Pharmaceuticals exemplifies challenges faced by small clinical-stage biopharmas reliant on external funding amid costly drug development cycles. After halting its lead therapeutic program due to capital constraints it has repositioned as a diagnostics-focused entity through licensing deals designed for faster market entry with lower upfront costs.

While financial losses persist albeit at improving rates and cash flow remains negative but trending positively [F1], near-term viability depends on securing additional financing before Q3 2026 as stated by management [S1]. The success of newly licensed diagnostic products will be key drivers of value creation moving forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments