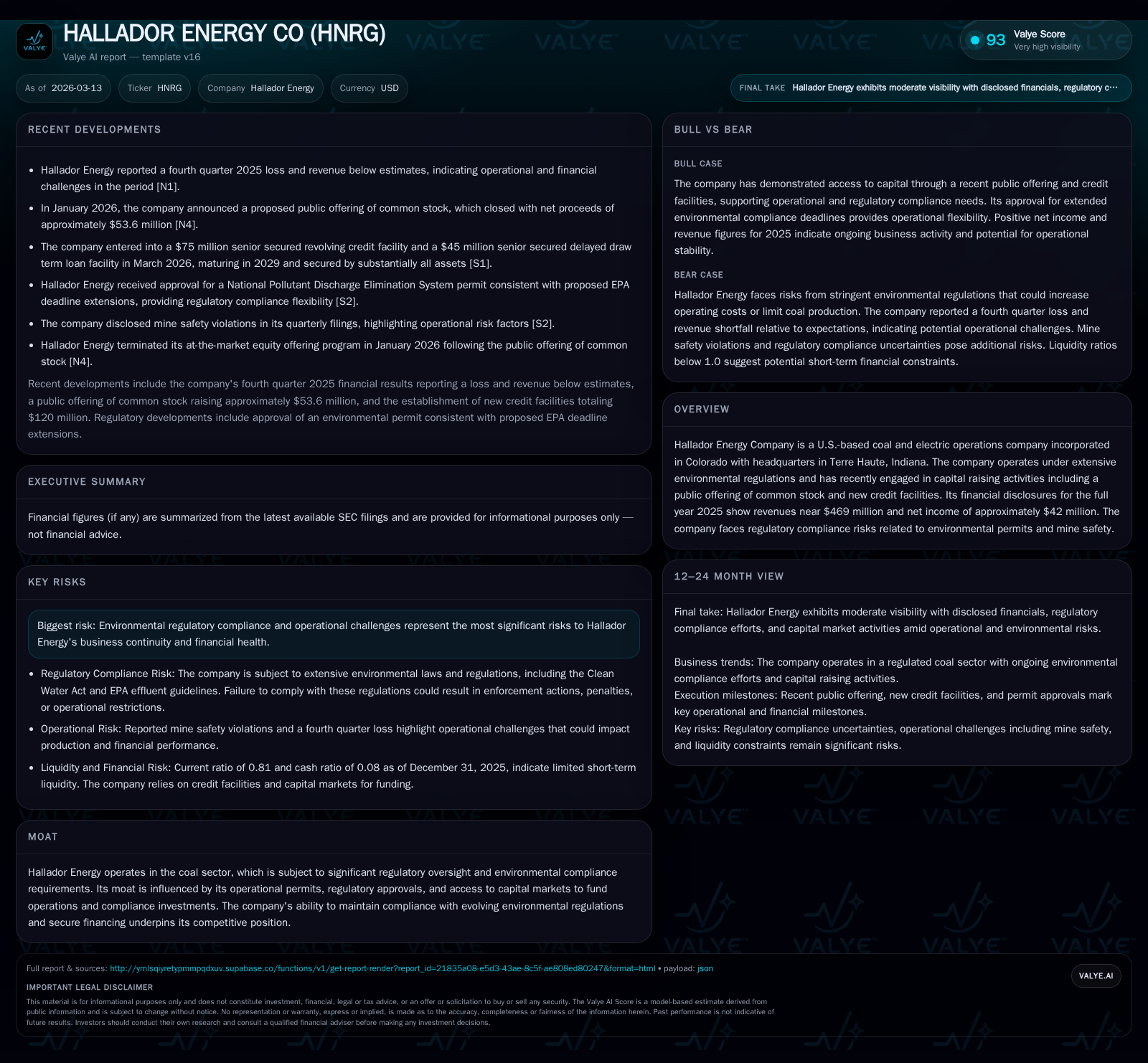

Hallador Energy Co Rebounds from Turbulent Year with Stabilized Electric and Coal Operations

Hallador Energy Company returned to profitability in 2025 after a heavy loss in 2024, supported by its coal-fired Merom Power Plant and strategic capital moves under tightening environmental rules.

Hallador Energy Company experienced significant volatility between 2023 and 2025, suffering a sharp operating loss in 2024 before staging a robust recovery in 2025 with revenue growth and positive operating income. The company’s operational core remains the Merom Power Plant alongside coal mining operations, both subject to strict environmental regulations that pose ongoing compliance risks. Strategic refinancing, including a new credit agreement and a public equity offering in early 2026, has strengthened Hallador’s liquidity position and enabled continued investments. Key growth drivers include permit acquisitions for expansion and navigating extended regulatory deadlines, although risks persist from potential regulatory shifts and market demand fluctuations for coal.

From Volatility to Recovery: Hallador’s Fiscal Performance Over Four Years

Hallador Energy's fiscal journey over the recent four-year span underscores a striking turnaround marked by severe losses followed by operational rebound. Revenue expanded notably by +16% from $404 million in FY2024 to $469 million in FY2025 (see Table below), recovering well after the steep contraction from $634 million in FY2023.

The operating income line illustrates Hallador’s rollercoaster trajectory: turning from a sizeable loss of $-218 million in FY2024 to a healthy $61 million gain in FY2025. The negative swing in FY2024 stemmed largely from impairment charges or restructuring costs aligning with industry-wide headwinds facing coal operators under market pressures and environmental mandates [F1]. Yet operational cash generation increased simultaneously by +23%, ending at over $81 million for FY2025. This was accompanied by an almost 30% surge in capital expenditures to $69 million — investments reflecting maintenance, regulatory compliance efforts, and selective development [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 469 | 42 | 81 | 61 | +16.1% | +118.5% |

| 2024 | 404 | -226 | 66 | -218 | -36.3% | -604.9% |

| 2023 | 634 | 45 | 59 | 65 | +75.3% | +147.4% |

| 2022 | 362 | 18 | 54 | 30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 12 | 26.2 |

| 2024 | 13 | -216.8 |

| 2023 | -16 | 16.7 |

| 2022 | 0 | 8.4 |

Source: SEC companyfacts cache [F1].

*Note: Financials for FY represent periods ended December each year; all figures sourced from company filings [F1].

Operational Backbone: The Merom Power Plant and Coal Mining Assets

A centerpiece of Hallador’s electric generation is the Merom Power Plant located in Sullivan County, Indiana—a coal-fired station with two steam turbine units totaling a nameplate capacity of approximately 1,080 MW [S1]. Nameplate capacity signifies maximum theoretical output capability during continuous full power operation; however actual production varies influenced by operational constraints and market dispatch.

Merom reported an accredited capacity averaging around ~775 MW during FY2025 compared to ~823 MW the prior year. Accredited capacity reflects the capacity value recognized within the Midcontinent Independent System Operator (MISO) market framework for reliability purposes based on rolling performance metrics spanning multiple years [S1]. Concurrently, the net capacity factor—percentage of actual net electricity produced relative to potential maximum output—increased markedly from approximately 44% in FY2024 to about 56% during FY2025 following operational stability improvements [S1]. This improvement responded well to market conditions favoring dispatchable coal assets amid grid reliability concerns.

Complementing electric production are Hallador’s coal reserve assets managed through rigorous annual reviews by qualified independent professionals conforming with SEC requirements [S1]. The Merom site also benefits logistically from adjacent rail and truck facilities facilitating efficient coal deliveries to power generation units as well as waste handling through its onsite landfill operations covering more than one hundred acres [S1].

Regulatory Landscape: Navigating Environmental Compliance Deadlines

Hallador operates within an increasingly stringent regulatory environment centered around federal EPA constraints including National Pollutant Discharge Elimination System (NPDES) permits tied to effluent guidelines (ELG rule). In October- November of FY2025, Hallador submitted and received conditional approval for an NPDES permit incorporating proposed deadline extensions under the EPA’s ELG Deadline Extensions Rule published October 2, 2025 [S2][S5]. These extensions would defer certain zero-discharge system compliance deadlines by five-to-six years up to December 31, 2034 versus the original phase-out date at end-2029.

Finalization of this rule remains pending public comment closure by November 3, 2025 [S2][N1]. Without finalization aligning with deadline extensions, Hallador risks Clean Water Act non-compliance as of December 31, 2025 potentially exposing it to enforcement or immediate costly upgrades [S2]. Additionally disclosed mine safety compliance records highlight ongoing operational diligence necessities typical across coal mining peers [S2][S7]. Regulatory adherence thus represents both an operational imperative and material risk.

2025 Capital Structure Overhaul and Its Leverage Parameters

Strategic capital restructuring culminated on March 5, 2026 when Hallador inked a Credit Agreement unlocking two principal facilities: (i) a senior secured revolving credit facility sized at $75 million; and (ii) a senior secured delayed draw term loan facility capped at $45 million subject to conditions precedent [S4][S6][S8]. These facilities supplant prior credit arrangements formerly held with PNC Bank.

Debt service costs under these agreements hinge on variable interest terms dependent on elected Base Rate or Term SOFR benchmarks augmented by margins linked directly to Hallador’s leverage ratios—a structured cushion familiar among energy sector borrowers balancing liquidity for capex-intensive regulated operations [S4].

The arrangement enforces restrictive affirmative/negative covenants including total leverage ratios ranging between approximately two-to-three times earnings before interest/tax/depreciation/amortization, fixed charge coverage minimums above unity (1.25x), as well as minimum liquidity thresholds initially set at about $20–30 million [S4]. Proprietary asset pledges underpin these secured obligations providing creditor comfort amid evolving business risk.

Projected Growth Drivers and Potential Environmental Constraints

Growth opportunities predominantly center on capitalizing expansion tracts adjacent to Merom (approximately seventy-two acres under option) enabling potential capacity or efficiency enhancements aligned with market demand [S1][N1]. Conservative permit renewal strategies coupled with anticipated NPDES timelines extending ELG compliance afford Hallador measured flexibility on capital outlays while deferring certain investment burdens.

Conversely, evolving emissions policies remain uncertain; failure of deadline extension finalization could force accelerated compliance expenditures or operational curtailment constraining expansion viability [S2][S5]. Market demand for coal-fired generation is subjected simultaneously to regional grid dynamics favoring reliability but juxtaposed against broader decarbonization trends restricting long-term growth scope.

Assessing Cash Flow Generation, Capital Expenditures, and Free Cash Flow

Operating cash flow exhibited robust growth of +23% year-over-year reaching over $81 million for FY2025—benefiting from improved power plant utilization and cost management measures [F1]. Parallelly, accounting for capital expenditures climbing nearly thirty percent primarily due to maintenance capital projects balanced free cash flow positively near $12 million (defined here as operating cash flow minus capex) reinforcing short-term financial flexibility despite reinvestment pace [F1].

This free cash flow profile implies that capital outlays are sustainable within existing cash generation capabilities without pressing immediate external funding obligation although ongoing debt servicing necessitates prudence.

Dividends, Share Buybacks, and Return on Equity Trends

Dividend payments have not been part of Hallador's recent shareholder returns post-2013 levels—the last documented dividends date back several years suggesting capital conservation prioritization amidst operational adjustments [F1]. Share repurchase programs have not been disclosed recently either per latest filings [S23][S26].

Return on equity finished the fiscal year at an approximate figure near or above twenty-six percent—calculated as net income relative to average shareholders’ equity—demonstrating effective equity utilization amid profitability restoration after multi-year losses [F1][S26]. This ratio reflects the successful conversion of earnings powered by improved operations without dilution effects offsetting gains.

What Investors Should Watch: Milestones and Upcoming Catalyst Events

Crucial near-term events revolve around EPA's final determination on the ELG Deadline Extensions Rule anticipated by November 3, 2025 —a regulatory inflection point that will dictate investment pacing related to wastewater discharge compliance mechanisms [N1][S2]. Monitoring subsequent quarterly reports will also be imperative given newly established debt covenants triggering periodic covenant tests impacting liquidity assessments post-March 2026 refinancing rollout.

Furthermore, ongoing market factors such as fluctuations in natural gas prices influencing dispatch economics for coal plants—and potential legislative actions impacting fossil fuel regulation—constitute persistent risk vectors beyond company control shaping medium-term outlooks.

This analysis synthesizes verified financial data and regulatory disclosures specific to Hallador Energy Company without extrapolating beyond documented sources. It aims to provide a comprehensive perspective on financial results, strategic initiatives, operational context, regulatory challenges, and prospective developments reflecting the company's current state as of early Q2-2026.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments