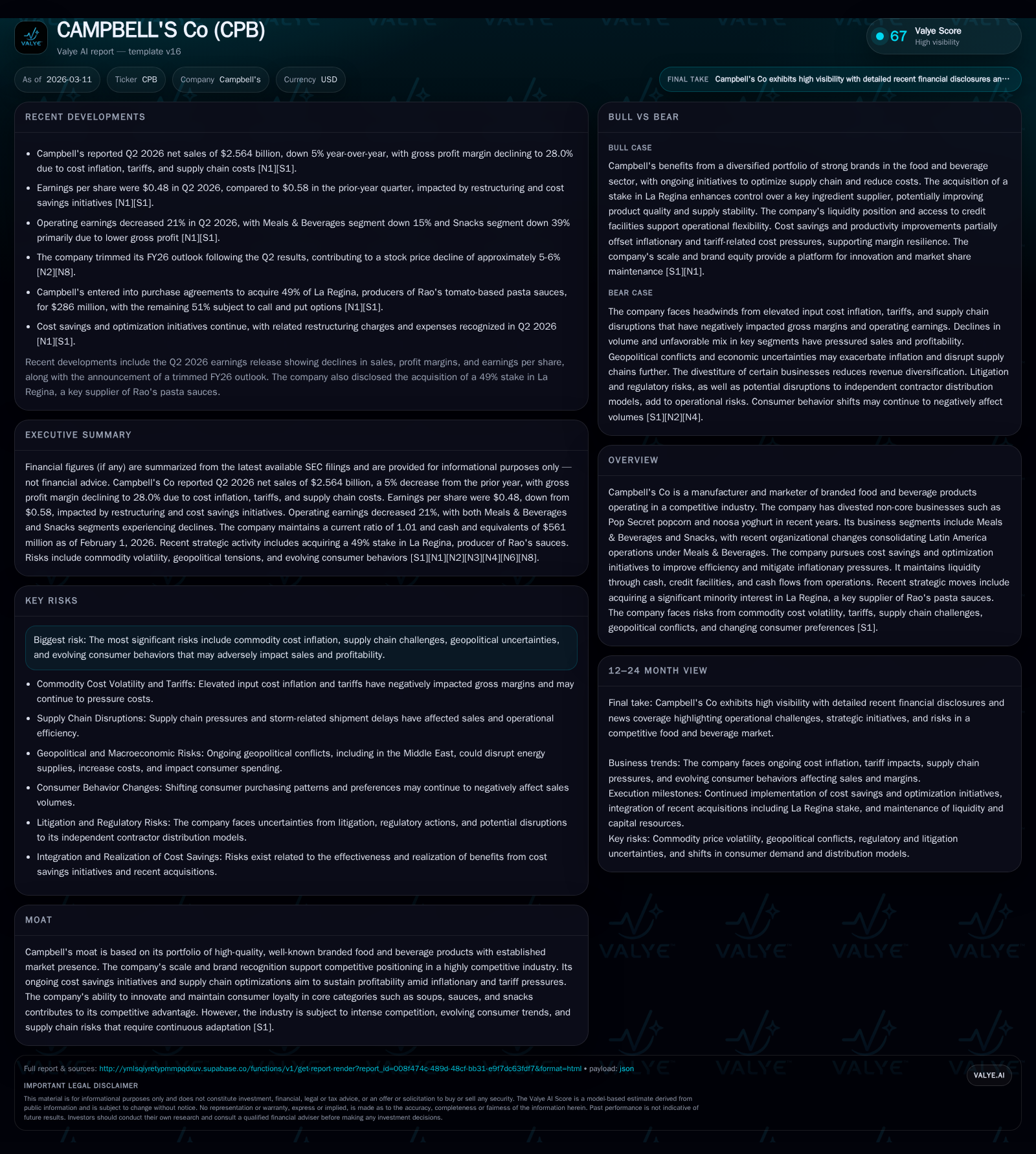

Campbell's Co Navigates Margin Pressures and Volume Challenges Amid Strategic Cost Savings

The branded food company addresses inflationary headwinds and shifting consumer trends through portfolio focus, operational efficiencies, and disciplined capital management.

Campbell's Co has demonstrated steady revenue growth driven by its core branded products over recent years. However, the company faces persistent margin pressures from commodity inflation, tariffs, and volume softness across its key segments. Strategic cost savings initiatives targeting $375 million in annual run-rate savings by 2028 aim to mitigate these challenges. Capital allocation remains focused on consistent dividends and active share repurchase programs while managing near-term debt maturities with a solid liquidity position. The recent acquisition of a minority stake in La Regina, producer of Rao’s pasta sauces, positions Campbell's for potential premium segment growth amid an uncertain macroeconomic environment.

Introduction

Campbell's Co (CPB) is a leading manufacturer of branded food and beverage products operating during challenging inflationary pressures, tariff-related costs, and changing consumer behaviors. The company has streamlined its portfolio by divesting non-core businesses such as Pop Secret popcorn (August 2024) and noosa yoghurt (February 2025), refocusing on its core Meals & Beverages segment which now includes Latin American operations [S2].

Historical Performance

Between fiscal years 2022 and 2025, Campbell's revenue increased steadily from approximately $8.56 billion to $10.25 billion, reflecting a compound annual growth rate of about 6.4% [F1]. Operating income peaked in FY2023 at $1.31 billion before declining to $1.12 billion in FY2025 during margin pressures [F1]. Net income similarly rose through FY2023 but moderated thereafter.

Margin contraction has been notable; gross profit margins declined by roughly 250 basis points in the first half of fiscal 2026 compared to the prior year period due primarily to tariff impacts (~230 basis points) and input cost inflation [S19][S20]. Productivity improvements and pricing initiatives provided partial relief.

Volume trends have been subdued with declines of approximately 2% in Meals & Beverages and 5% in Snacks segments during early 2026, influenced by shifting consumer purchasing patterns and inventory adjustments [S23][S24]. Pricing actions delivered modest net price realization gains (~1%).

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 10.3 | 602 | 1131 | 1124 | +6.4% | +6.2% |

| 2024 | 9.6 | 567 | 1185 | 1000 | +3.0% | -33.9% |

| 2023 | 9.4 | 858 | 1143 | 1312 | +9.3% | +13.3% |

| 2022 | 8.6 | 757 | 1181 | 1163 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 459 | 62 | 705 |

| 2024 | 445 | 67 | 668 |

| 2023 | 447 | 142 | 773 |

| 2022 | 451 | 167 | 939 |

Source: SEC companyfacts cache [F1].

Table: Four-year financial summary highlighting revenue growth, profitability metrics, cash flow generation, capital expenditures, dividend payments, and share repurchases [F1]

Business Segments & Strategic Initiatives

Campbell's operates primarily through two segments: Meals & Beverages—which includes soups, sauces (including Latin America), and beverages—and Snacks featuring brands like Pepperidge Farm cookies.

A key strategic move was the acquisition of a 49% equity interest in La Regina di San Marzano di Antonio Romano S.p.A., the exclusive producer of Rao’s tomato-based pasta sauces [S2]. This investment enhances Campbell's influence over product quality and supply chain management while retaining options for future ownership expansion through call/put provisions.

The company continues its multi-year cost savings initiatives targeting $375 million in annual pre-tax savings by fiscal year-end 2028; about $180 million has been realized as of early FY26 [S15][S22]. Initiatives encompass manufacturing footprint optimization as well as enhancements to the Snacks direct-store-delivery network.

Near-Term Performance & Outlook

In the latest quarterly results reported March 11, 2026, revenue declined approximately 4% year-over-year due to volume softness despite pricing efforts [N1][N9][S19][S20]. Operating earnings decreased between approximately 15% (Meals & Beverages) to nearly 40% (Snacks), reflecting ongoing margin pressures tied to commodity costs and tariffs partially offset by productivity gains.

The company anticipates moderation in inflationary pressures throughout calendar year 2026 alongside continued tariff mitigation efforts [S2], though volume challenges are expected to persist given ongoing shifts in consumer spending patterns [N9]. Geopolitical instability including conflicts in the Middle East poses further uncertainty around energy prices that could affect consumer demand [S2].

Capital expenditures are projected at approximately $370 million for fiscal year ending August '26, directed toward production network upgrades, IT infrastructure projects including ERP implementations post-Sovos Brands acquisition integration [S14][S22].

Capital Allocation & Financial Health

Campbell's maintains disciplined capital allocation balancing shareholder returns with reinvestment needs. Dividends paid totaled approximately $459 million in FY25 with quarterly dividends held steady at $0.39 per share into FY26 [F1][S4]. Share repurchase authorizations include a $500 million program initiated in September 2021 with about $301 million remaining as of early ’26 plus an anti-dilutive program authorized September ’24 with roughly $172 million capacity left [S4].

Liquidity is robust with cash & equivalents totaling $561 million as of February ’26 alongside a current ratio near parity (current assets ~$2.73 billion vs liabilities ~$2.69 billion) [F1][S5][S9]. The company manages near-term debt maturities including $400 million senior notes due March ’26 expected to be refinanced or repaid using internal resources supplemented by revolving credit or commercial paper facilities [S12]. Long-term debt includes recent issuances extending maturities into mid-2030s at fixed rates providing stability amid market volatility.

Risks & Industry Context

Key risks include sustained commodity price volatility affecting input costs; tariff complexities impacting sourcing; global supply chain disruptions; geopolitical tensions influencing energy prices; regulatory challenges especially concerning independent contractor classification within Snacks distribution; litigation exposures; cybersecurity threats; evolving consumer preferences leaning towards fresh or plant-based alternatives; and competitive retail dynamics [S17][S18][N1].

Forward-Looking Considerations

While explicit volume guidance was trimmed during Q2 earnings commentary reflecting cautious outlooks [N9], critical factors shaping future performance include:

- Realization of synergies from La Regina equity investment potentially enhancing margins through supply chain control.

- Progress on cost savings programs supporting operating leverage improvement.

- Recovery trajectory of consumer demand particularly for soups and hearty meals post-inflationary environment.

- Efficient management of debt refinancing amidst rising interest rate environments.

- Navigating geopolitical uncertainties which could materially impact energy prices and thus discretionary grocery spending.

Conclusion

Campbell's Co continues to leverage its strong brand portfolio amid complex macroeconomic headwinds marked by inflationary input costs, tariff effects, supply chain challenges, and evolving consumer behaviors. While top-line growth remains solid at mid-single-digit rates over recent years [F1], profitability has been pressured notably during early fiscal ’26 results. Strategic investments such as the La Regina stake alongside extensive cost savings initiatives underscore management’s intent to restore margin strength over time.

Capital deployment balances steady shareholder returns via dividends and share buybacks with prudent debt management maintaining liquidity resilience under market uncertainties.

Monitoring execution on cost efficiencies alongside volume recovery will be essential indicators for operational sustainability going forward.

This analysis is based solely on publicly available information including latest SEC filings as of March 11, 2026, recent earnings call transcripts, industry context considerations but does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments