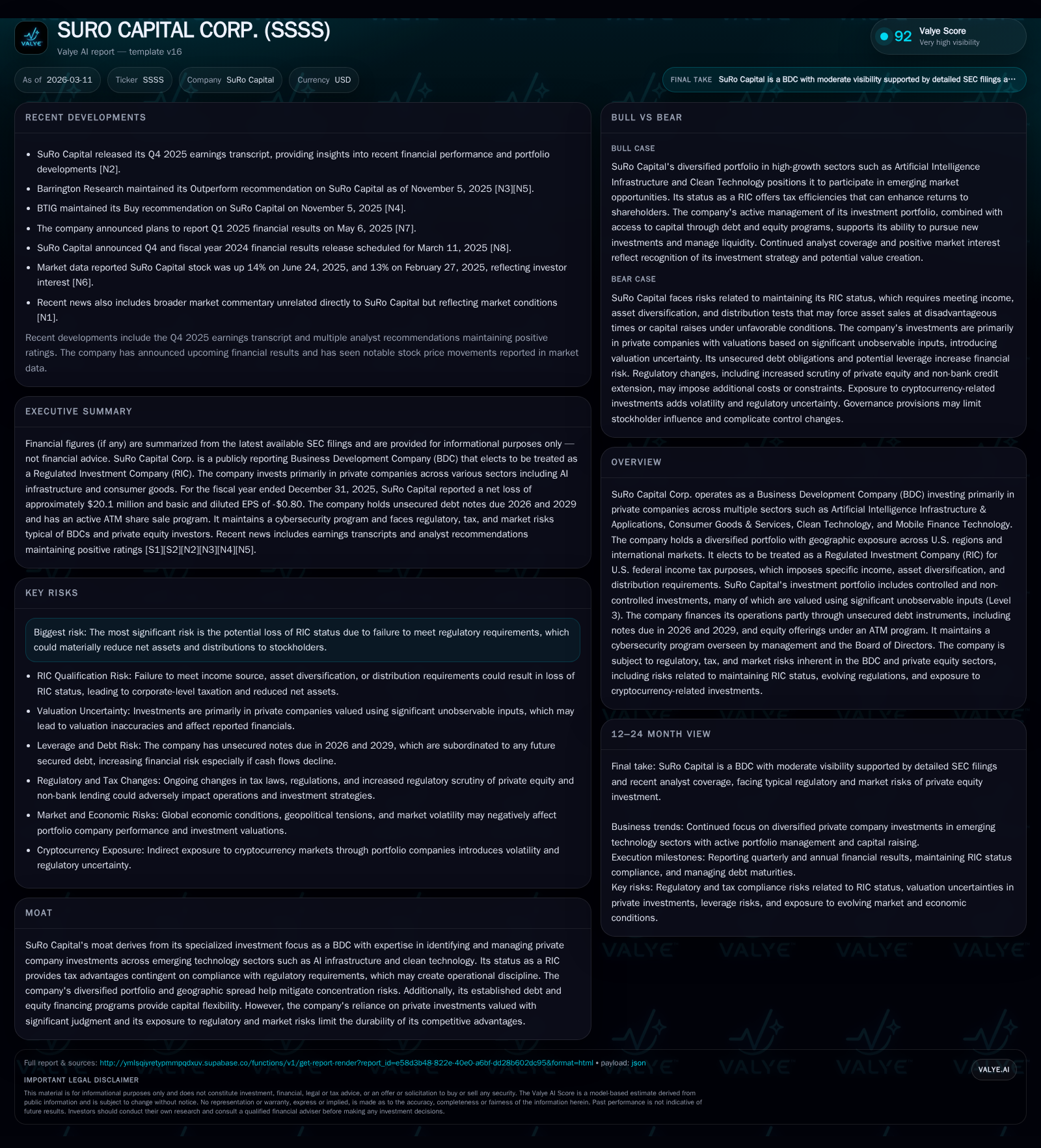

SuRo Capital Corp. Rebounds: Assessing Returns and Risks in Private Equity Ventures

SuRo Capital shows improved operating cash flows despite deepening net losses, highlighting valuation complexities and leverage challenges in its BDC model.

SuRo Capital Corp., a business development company investing primarily in private companies across emerging sectors, reported a significant increase in operating cash flow for fiscal year 2025 alongside a notable net loss. The divergence between cash generation and earnings largely stems from fair value measurement fluctuations tied to Level 3 inputs used for its private portfolio. Equity grew moderately while dividends expanded sharply, though share repurchases paused despite available authorization. Regulatory risks center on maintaining RIC status under strict income and diversification rules, which may necessitate rapid portfolio adjustments. Looking ahead, growth depends on sector momentum, capital management, and navigating regulatory constraints.

Financial Trajectory: Analyzing Recent Fiscal Years' Performance

SuRo Capital's financial results over the last four fiscal years reveal marked swings characteristic of its BDC investment approach concentrated in private equity. Net income fluctuated significantly—from losses of approximately -$12.4 million in FY2022 and -$9.1 million in FY2023 to a modest profit of $44.5 thousand in FY2024 before plunging again to a -$20.1 million loss in FY2025 [F1]. This volatility contrasts with a sharp improvement in operating cash flow, which rose from negative $110.6 million in FY2022 to positive $2.37 million in FY2024 and then surged to over $34.3 million in FY2025 [F1]. The disparity between earnings and cash flow reflects substantial non-cash fair value adjustments.

Equity showed moderate variation but trended upward after a dip: from $210 million at end-FY2022 down to $157.6 million at end-FY2024 before recovering to $205 million at end-FY2025 [F1]. Dividends paid increased dramatically from under $150K in prior years to nearly $12 million in FY2025 [F1], signaling enhanced capital return efforts amid ongoing net losses. Share repurchases, previously material ($21.4M in FY2022; $14.2M in FY2023), halted entirely by FY2024-25 despite over $25 million remaining authorized under the repurchase program [F1][S4].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -20 | 34 | -45308.8% |

| 2024 | 0 | 2 | +100.5% |

| 2023 | -9 | 2 | +26.4% |

| 2022 | -12 | -111 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 12 | 9 | -9.8 |

| 2024 | 0 | 9 | 0.0 |

| 2023 | 0 | 14 | -4.5 |

| 2022 | 27 | 21 | -5.9 |

Source: SEC companyfacts cache [F1].

Note: Share repurchases not reported for FY2025; dividends and buyback figures exclude partial year adjustments.

This pattern illustrates SuRo’s dynamic where operational liquidity has strengthened substantially even as earnings remain sensitive to investment valuation changes.

Investment Focus and Portfolio Composition: Navigating Level 3 Valuations

SuRo Capital primarily invests in private companies spanning sectors such as Artificial Intelligence Infrastructure & Applications, Clean Technology & Sustainable Solutions, Consumer Goods & Services including Mobile Finance Technology [S21]. These assets generally lack liquid market prices requiring fair value accounting based on Level 3 inputs — unobservable assumptions management uses to estimate market participant valuations [S1].

Such valuation methods inherently inject volatility into periodic financial results given reliance on internal models amid limited comparables for private stakes. Consequently, fluctuations in reported earnings often reflect shifts in valuation assumptions rather than operational business changes.

For investors accustomed to the private equity BDC space this underscores the need to emphasize cash flow trends and assess credibility of valuation methodologies underpinning Level 3 measurements.

Leverage Position and Regulatory Compliance Within the BDC Framework

Operating under the Small Business Credit Availability Act (SBCAA), SuRo can reduce its asset coverage requirement—the ratio of equity to debt—from the standard minimum of 200% down to as low as 150%, subject to shareholder or independent director approval [S6]. This enables increased leverage capacity up to roughly two-thirds debt relative to total assets; however SuRo currently maintains conservative leverage aligned with covenants on its unsecured notes due December 2026 and other debt instruments [S6][S7].

The Company’s outstanding debt includes unsecured notes bearing a fixed coupon of 6%, maturing December 30, 2026 [S13]. Covenants mandate maintaining asset coverage above specified thresholds; failure could restrict dividends or share repurchases [S15].

Leverage amplifies investment returns when asset values rise but also magnifies downside risk during valuation declines or operational setbacks [S6]. This leverage profile critically influences dividend sustainability and capital deployment flexibility within SuRo’s BDC structure.

Capital Allocation Dynamics: Dividends Growth Amid Buyback Suspension

Capital return strategy shifted notably entering FY2025 when dividends increased sharply to nearly $12 million from minimal prior payouts [F1][S18][S20]. Conversely share repurchases halted since early FY2024 despite an authorized program expanded up to approximately $64 million through October 31, 2026 [S4]. Market conditions likely contributed to management’s cautious stance on buybacks amid economic uncertainties.

Additionally SuRo operates an At-the-Market (ATM) equity offering program initiated mid-2020 providing flexible capital raising without fixed issuance targets [S4]. This facilitates incremental stock sales at prevailing prices supporting liquidity or new investments without recent dilution events noted.

Dividend growth reflects confidence supported by improving cash flows though continued net losses—partly due to unrealized valuation timing differences—temper sustainability expectations [S18][S20].

Regulatory Risks Impacting RIC Status and Investment Discipline

A central risk factor is SuRo’s election as a Regulated Investment Company (RIC), which affords favorable tax treatment contingent upon compliance with strict criteria governing qualifying income sources (minimum 90%) and asset diversification tests measured quarterly [S1]. Failure risks incurring corporate taxes that could materially reduce distributable earnings.

Given much of SuRo’s portfolio consists of illiquid private companies with valuation uncertainty it may face forced dispositions at disadvantageous prices if unable to timely meet diversification or income sourcing rules [S1].

Annual distribution requirements further compel payout levels potentially constrained by asset coverage ratios or debt covenants limiting borrowings or equity returns [S15][S20]. Management must balance portfolio construction prudently against regulatory mandates—a key consideration for investors.

Future Growth Vectors: Sector Exposure and Market Opportunities

SuRo’s investment themes align with secular growth drivers including AI infrastructure enabling digital transformation; clean technology addressing environmental imperatives; fintech innovations reshaping finance; plus consumer services adapting to evolving behaviors [N1][S21]. Its portfolio exhibits geographic diversity spanning U.S. regions—Northeast (35%), West (22%), Midwest (22%)—and includes international exposure (1–8%), providing some risk dispersion benefits [S21].

However growth potential is moderated by underlying illiquidity paired with regulatory constraints limiting rapid portfolio rebalancing necessary for RIC compliance or capital structure flexibility amid macroeconomic uncertainties impacting deal flow and pricing [N1][S12]. Thus future outcomes hinge on navigating these intersecting dynamics successfully.

Upcoming Milestones and Strategic Watchpoints for Investors

Key performance indicators warranting close attention include:

- Quarterly Net Asset Value (NAV) fluctuations particularly driven by Level 3 valuation input revisions affecting unrealized gains/losses;

- Management actions regarding refinancing or redemption decisions around notes maturing December 2026 amidst interest rate environment developments [S9];

- Communications on adherence to RIC diversification tests or required portfolio adjustments;

- Activity levels under ATM equity offerings signaling capital needs or dilution potential;

- Dividend declaration patterns reflecting confidence amid earnings volatility.

The subjective nature of private investment valuations combined with regulatory frameworks creates inherent uncertainties complicating milestone visibility yet defines critical inflection points shaping SuRo's operational discipline.

Disclaimer: Analysis based solely on publicly available filings through March 11, 2026. Not investment advice.

Comments