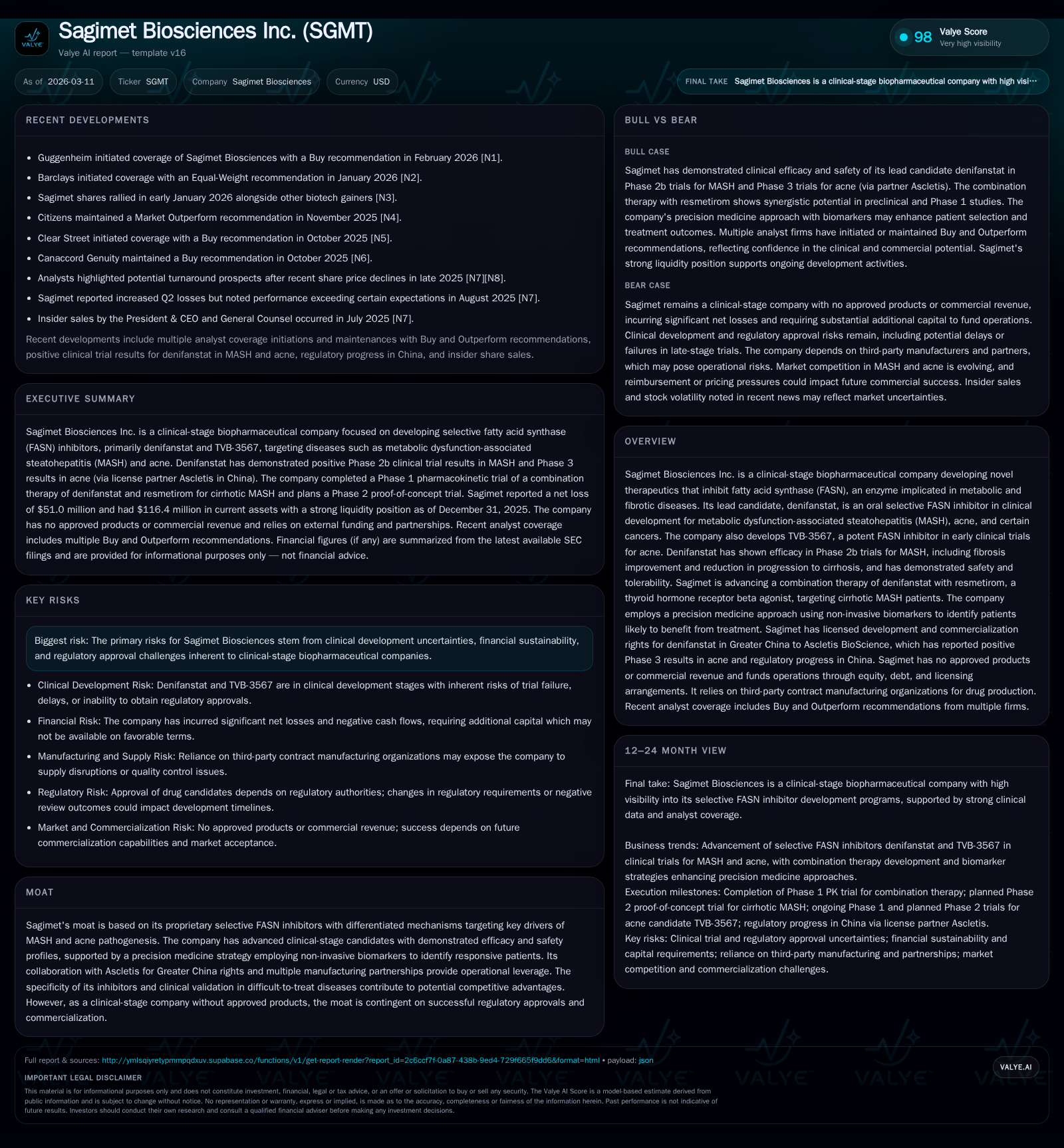

Sagimet Biosciences: Clinical Progress and Capital Strategy in Fatty Acid Synthase Inhibition

Sagimet leverages selective FASN inhibition to target MASH and related diseases, balancing advancing clinical milestones with prudent cash management amid regulatory complexities.

Sagimet Biosciences concentrates on developing selective fatty acid synthase inhibitors, notably denifanstat, which has demonstrated efficacy in Phase 2b trials for metabolic dysfunction-associated steatohepatitis (MASH). While the company has expanded its pipeline into dermatological and oncological indications, it remains a clinical-stage entity with an operating loss trajectory and a sizable cash runway supporting ongoing R&D. Regulatory hurdles and reimbursement pressures pose material risks, yet strategic partnerships and biomarker-driven precision medicine underpin its competitive positioning. Near-term catalysts include further trial readouts, regulatory submissions, and biomarker validations critical for Sagimet's transition toward commercialization.

Clinical Evolution and Historic Performance Trends

Sagimet Biosciences has advanced its selective fatty acid synthase (FASN) inhibitor program over recent years with intensified investment in R&D aimed at metabolic dysfunction-associated steatohepatitis (MASH) and other indications. From FY2023 to FY2025, the company’s operating income declined from -$30.74 million to -$56.89 million, representing an approximately 4.5% worsening year-over-year between FY2024 and FY2025 [F1]. Net losses similarly grew from -$27.88 million in FY2023 to -$51.04 million in FY2025, reflecting continued expenditures on pivotal clinical studies and preparation for potential commercialization.

Operating cash flows have also trended negatively, increasing their burn rate by roughly 7.6% YoY into fiscal 2025 as clinical activities intensified [F1]. This loss expansion arises chiefly from larger-scale Phase 2b/Phase 3 trials aligned with denifanstat's advancement in MASH targeting fibrosis.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -51 | -46 | -57 | -12.0% |

| 2024 | -46 | -42 | -54 | -63.5% |

| 2023 | -28 | -24 | -31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -45.8 |

| 2024 | -29.2 |

| 2023 | -30.6 |

Source: SEC companyfacts cache [F1].

The upward trajectory in research expense allocations correlates directly with successful completion of FASCINATE-2 results and initiation of Phase 3 programs [S1]. Despite escalating losses typical for developmental-stage biopharma firms, Sagimet maintains robust liquidity positions facilitating continued operations.

Precision Medicine Focus: Targeting MASH with Selective FASN Inhibitors

Denifanstat acts as a selective oral FASN inhibitor impacting three key pathogenic pathways in MASH: steatosis reduction, anti-inflammatory effects, and anti-fibrotic activity [S1]. This approach is unique relative to other MASH modalities that often focus narrowly on fibrosis or metabolic parameters.

The Phase 2b FASCINATE-2 trial enrolled 168 biopsy-confirmed MASH patients with moderate-to-advanced fibrosis (stages F2-F3). Denifanstat achieved all primary endpoints after 52 weeks compared to placebo, including significant histological improvements:

- Fibrosis improvement ≥1 stage with no worsening of MASH in the F3 modified intention-to-treat population: 49% vs. placebo’s 13% (p=0.0032).

- Fibrosis improvement ≥2 stages: denifanstat arms showed up to 34% vs placebo’s low single digits (p=0.0065).

- Statistically significant lower progression to cirrhosis (F4): denifanstat 5% vs placebo 11% (p=0.0386).

These biopsy-based outcomes—considered the gold standard in NASH/MASH trials—are complemented by AI-enabled histology (SGH HistoIndex platform), offering advanced lesion quantification beyond human pathologist scoring [S1].

Furthermore, denifanstat's safety profile remained favorable throughout the study period with tolerability suitable for chronic administration.

This biomarker-driven precision medicine strategy leverages non-invasive diagnostics to stratify patients likely to derive benefit, aligning with industry trends toward tailored therapies in hepatology.

Recent Initiation of Broker Coverage and Market Sentiment

In early 2026, two notable brokerages initiated coverage on Sagimet with different perspectives reflecting divergent risk-reward assessments:

- Guggenheim launched with a Buy rating emphasizing the promising clinical data from denifanstat’s Phase 2b trial, growth potential in largely unmet MASH patient subsets including cirrhotic stages, and strategic partnerships enabling geographic expansion [N1].

- Barclays assigned an Equal-weight rating highlighting uncertainties around future regulatory approvals given the absence of precedent FDA approvals in cirrhotic MASH as well as broader reimbursement concerns affecting pricing power [N2].

These contrasting stances illustrate industry recognition of Sagimet’s scientific advances while underscoring persistent execution challenges inherent to clinical-stage biotech stocks.

Assessing Pipeline Prospects for Metabolic and Dermatological Indications

Beyond denifanstat’s lead indication in MASH, Sagimet pursues leveraging its selective FASN inhibition platform for additional disease areas:

- TVB-3567 is under early-phase investigation targeting acne vulgaris—a dermatological condition also linked mechanistically to aberrant fatty acid metabolism [S1]. The development here capitalizes on topical/localized delivery potentials reducing systemic risk.

- A combination therapy pairing denifanstat with resmetirom — a thyroid hormone receptor beta agonist — is being explored specifically for cirrhotic MASH patients who represent a subset lacking effective treatment options currently [S1]. This synergistic approach aims at addressing multiple disease axes simultaneously.

This diversified pipeline strategy reduces dependence on a single product-event catalyst while exploiting overlapping pathogenetic mechanisms within metabolic/fibrotic disorders.

Financial Framework: Operating Loss Trajectory, Cash Position, and Capital Efficiency

As of December 31, 2025 SAGT held $35 million in cash & equivalents backed by $116 million in current assets balanced against minimal current liabilities of approximately $5.1 million [F1]. The resultant current ratio near ~22.8 far outpaces typical biotech liquidity norms indicating excellent short-term solvency.

However, operating cash flow remains negative at about $45.7 million annually due mainly to ongoing clinical expenditures including trial enrollment costs and manufacturing scaling efforts [F1][S19][S21][S29].

Sagimet explicitly states that despite sufficient cash runway for at least the next twelve months based on current plans per its FY2025 filing, variable operational needs or expedited development timelines could necessitate earlier capital raises [S19]. The company continues utilizing controlled equity offerings as a flexible financing vehicle under recent sales agreements totaling up to $75 million [S29].

This capital structure approach reflects standard practices among clinical-stage peers focused primarily on development rather than revenue generation resources.

Decoding Sagimet’s Return Metrics and Capital Allocation Policies

The approximate return on equity calculated for FY2025 stands near -46%, consistent with sustained net losses during heavy investment phases before product commercialization attempts [F1]. This figure typifies the negative ROE profile commonly observed among nascent biotechs prioritizing pipeline maturation over immediate profitability.

There are no dividends or share repurchase programs disclosed owing to capital scarcity realities and an explicit focus on reinvesting resources into research progressions rather than distributing shareholder returns currently [F1].

Capital deployment thus centers strategically on advancing registrational trials targeting key endpoints substantiating potential FDA approval applications.

Regulatory Hurdles, Reimbursement Environment, and Risk Landscape

Sagimet faces regulatory scrutiny typical for novel therapies targeting complex indications such as MASH which lacks fully approved therapies especially in advanced fibrosis stages (F3-F4) [S4][S5][S6][S7][S8]. Approval success depends heavily on demonstrating durable histopathologic benefit alongside safety profiles acceptable for chronic use.

Payer dynamics present challenges given increasing third-party skepticism about pricing new pharmaceuticals without clear pharmaco-economic advantage or established treatment standards [S4][S6][S28]. Formulary placement may require costly health technology assessment studies supporting cost-effectiveness claims beyond initial FDA approval.

Furthermore compliance regimes encompassing federal anti-kickback rules, data privacy laws including HIPAA expansions and international GDPR-like statutes introduce operational complexity across markets impacting launch preparedness [S22].

Litigation risks related to marketing practices or post-marketing surveillance failures remain relevant contingent upon eventual commercialization steps.

Strategic Collaborations and Manufacturing Partnerships as Operational Levers

Sagimet’s collaboration agreement granting Ascletis rights across Greater China represents a critical regional out-licensing tactic accelerating geographic market access without corresponding upfront commercial infrastructure build-out costs [S1].

Multiple contract manufacturing organizations (CMOs) engaged provide flexibility in drug substance production ensuring adherence to cGMP standards needed across late-phase clinical trial material supply chains potentially scaling toward commercial volumes if approvals are granted [S13][S15].

Such partnership arrangements distribute operational risks while leveraging external specialized expertise improving time-to-market agility common among small biotech innovators.

Near-Term Catalysts and Key Milestones to Monitor

Sagimet’s forthcoming value inflection points center around anticipated regulatory filings leveraging comprehensive datasets from FASCINATE phase programs alongside planned Phase 3 study initiations or completions evaluating denifanstat alone or combined therapies targeting severely fibrotic MASH cohorts [N1][N2][S3].

Biomarker validation studies enhancing patient selection precision remain pivotal enabling cost-effective trial designs potentially reducing heterogeneity associated with traditional biopsy-based enrollment criteria ['analysis']. Additionally attention will focus on ASCLETIS collaboration developments clarifying regional commercialization timing or revenue sharing structures.

Careful monitoring of evolving U.S./international reimbursement policies influenced heavily by ongoing healthcare reform initiatives—including Medicare drug price negotiation models under legislation—will be crucial given their impact on potential market launch economics [S14][S16][S17].

Sagimet stands at a crossroads bridging encouraging mechanistic science validated clinically yet still navigating conventional biotech hurdles involving financing strategies amid regulatory/reimbursement uncertainties characteristic of this high-risk arena.

This analysis is intended solely for informational purposes based on publicly available SEC filings and reputable news sources as cited; it does not constitute investment advice or recommendations to buy or sell securities of Sagimet Biosciences Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments