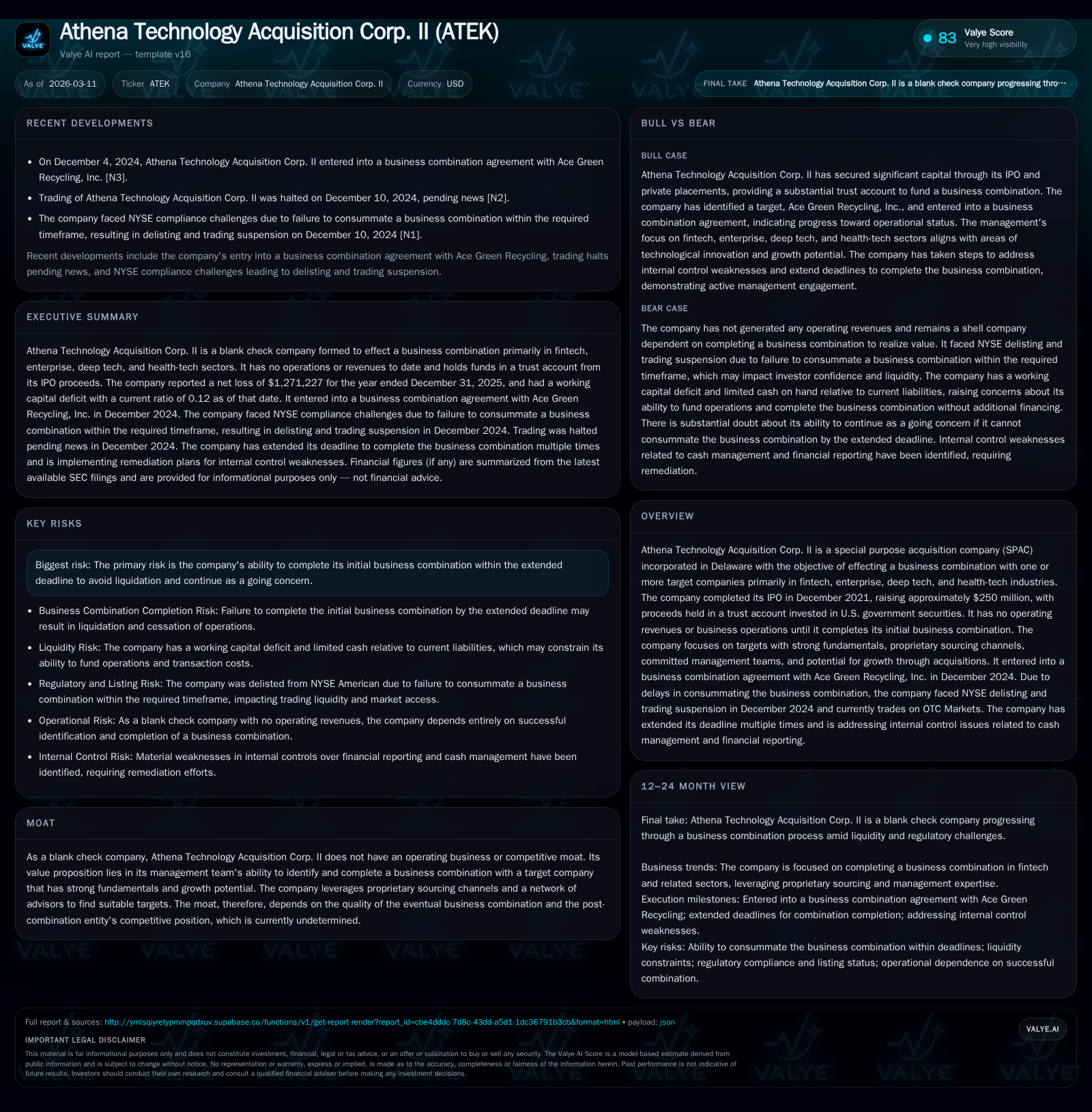

Athena Technology Acquisition Corp. II: Evaluating SPAC Milestones and Capital Deployment

Athena Technology Acquisition Corp. II's trajectory from its sizeable IPO raise to pending business combination underscores mounting liquidity pressures and strategic capital decisions.

Since its December 2021 IPO generating approximately $250 million, Athena Technology Acquisition Corp. II has pursued initial business combinations aimed at fintech and deep-tech targets, most recently aligning with Ace Green Recycling in late 2024. However, repeated extension requests to consummate a deal have resulted in liquidity challenges, a deteriorating working capital position, and NYSE delisting risks. Financing strategies increasingly rely on sponsor loans and nuanced capital structures including earnout shares. Completion of the merger by the revised April 2026 deadline is critical for the company’s future viability and unlocking its latent value.

IPO Capital Raise and Early Growth Trajectory

Athena Technology Acquisition Corp. II launched via an initial public offering (IPO) in December 2021, successfully raising gross proceeds of approximately $250 million through the sale of 25 million units at $10 each [S1][S18]. These units included one share of Class A common stock plus half a redeemable warrant. Complementary private placements added roughly $9.5 million, sold to Athena's Sponsor [S7][S8]. The funds raised were placed in a trust account invested primarily in U.S. government treasury securities, consistent with typical SPAC structures.

As a blank check company incorporated in Delaware for the express purpose of executing one or more business combinations, Athena identified sectors with significant growth potential — specifically fintech, enterprise software, deep technology, and health technology [S1][S18]. It structured its search strategy around proprietary sourcing channels to identify targets with strong fundamentals and committed management teams capable of scaling through organic growth or acquisitions.

The capital raise positioned Athena as a potential conduit for historically underfunded emerging tech companies to access public markets liquidity. Despite this platform potential, Athena did not generate any operating revenues prior to completing a business combination—its income statement reflects typical pre-combination SPAC activity dominated by operational costs without commercial revenues [S1][F1].

Evolution of Business Combination Efforts: Targets and Progress

Athena’s initial foray into business combination talks culminated in an agreement signed April 19, 2023, with Air Water Company [S1]. However, this deal was mutually terminated on December 13, 2023 after protracted negotiations failed to yield consummation [S1]. Following this setback, Athena entered into a Business Combination Agreement on December 4, 2024, with Ace Green Recycling Inc., signaling renewed progress toward the SPAC’s objective [S1][N1].

The terms included standard merger mechanics where Merger Sub would merge into Ace Green Recycling making it a wholly owned subsidiary post-closing [S1]. Shareholders of Ace Green would receive shares in Athena based on an established exchange ratio plus up to 10.5 million earnout shares contingent upon Athena's common stock trading price over five years following the closing [S1]. Additionally, the Sponsor is positioned to receive up to an aggregate of 1.5 million shares subject similarly to performance criteria.

Voting and Support Agreements accompanied these transactions ensuring the Sponsor and certain Ace Green shareholders committed their voting power in favor of the business combination proposal ahead of shareholder meetings [S1]. This blocks potential deal obstruction but simultaneously concentrates voting power among insiders.

The delayed consummation timeline has caused heightened regulatory scrutiny; notably the NYSE has flagged compliance issues due to postponement past initial deadlines tied to SPAC listing standards [N1]. Completion of this merger remains existentially pivotal for Athena.

Liquidity Strains and NYSE Compliance Risks

Liquidity presents one of Athena’s most pressing challenges as it approaches the extended deadline. As of December 31, 2025, operating cash stood at a modest $348,472 while the company reported a working capital deficit of approximately $8 million—a striking imbalance underscoring underlying cash flow stress [F1][S5][S6]. These figures highlight limitations for funding ongoing due diligence or transaction expenses absent sponsor support.

Athena benefits from arrangements with its Sponsor who has injected non-interest-bearing unsecured promissory notes amounting collectively well over $2 million to cover working capital shortfalls and extension fees [S5][S6][S16][S17]. These loans are payable either upon consummation or liquidation; sponsors retain conversion rights into equity units priced at $10 each offering some downside protection but also contribute complexity to post-merger capitalization [S5][S6][S13].

The company secured multiple monthly extension options—now exercising the seventh out of nine permitted extensions delaying the deadline from March 14 to April 14, 2026—and paid associated fees funded largely by Sponsor advances often underwritten through additional subscription agreements involving third-party investors [N1][S21].

Critically, management explicitly acknowledges "substantial doubt" about continuing as a going concern per ASC guidance given current liquidity constraints coupled with mandatory liquidation risk if no combination closes by mid-2026 [S6]. The NYSE notices further underscore market risk around listing status given prolonged uncertainty [N1][S28].

Financial Performance Overview: Income, Cash Flow, and Equity Trends

The absence of operating revenue translates into sustained net losses as Athena focuses resources on pursuing its business combination objectives:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -1 | -1 | +52.0% |

| 2024 | -3 | -3 | -297.8% |

| 2023 | 1 | -1 | -7.9% |

| 2022 | 1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | 7.5 |

| 2024 | 22 | 14.0 |

| 2023 | 240 | -8.9 |

| 2022 | -16.6 |

Source: SEC companyfacts cache [F1].

[F1]

Net losses narrowed materially by over half from FY24 to FY25 though remain significant expenses relating primarily to administrative costs connected with due diligence and extension fees before culmination of any business combination event [F1][S15]. Operating cash flow shows marked improvement but remains negative across all four years illustrating ongoing consumption of cash resources ahead of generating operational revenue streams.

Equity diminished substantially over this period reaching negative territory beyond $17 million as accumulated losses exceed contributed capital—a typical deleveraging pattern for pre-revenue SPACs absorbing costs unrecouped through earnings but risking impairment without deal closure [F1].

Return on equity computed naïvely using net income divided by negative equity approximates +7.5%, reflecting accounting distortions rather than operational returns given net losses combined with highly negative equity balances [F1]. Thus traditional profitability metrics offer limited insight absent transactional inflection.

Capital Allocation: Working Capital Loans, Buybacks, and Sponsor Transactions

Beyond initial trust account funds segregated since IPO closing ($256+ million), Athena deployed a layered approach toward financing transactional overheads:

- Issuance of unsecured promissory notes totaling approximately $422k from Sponsor without interest bearing features; repayable on earlier of specified dates or conversion upon successful business combination [S5][S16].

- A broader suite of working capital loans including extension notes aggregating $1.8 million outstanding at end-2025 provided by Sponsor alongside affiliated entities and certain officers/directors with repayment or conversion options aligns incentives while managing liquidity crunches [S6][S17]

- Several private placement transactions injecting additional capital closely linked structurally with share issuance obligations post-merger create intricate equity financing layers but signal sponsor commitment despite market uncertainty [S7][S8][S22]

- Share repurchase programs showed steep diminution YOY ($3.3 million buybacks in FY25 versus over $21 million prior year), suggesting disciplined conservation amid resource scarcity rather than active reward distributions given absence of earnings capacity [F1][S12]

- Founders converted Class B founder shares into Class A shares mid-term expanding publicly traded share pool but maintaining restrictions supportive of governance continuity ahead of potential de-SPAC transition [S7]

This patchwork corporate finance underscores how Athena's post-IPO capital deployment tactics evolved pragmatically due to protracted timelines compressing available resources with no revenue inflows yet realized.

Potential Value Drivers Post-Combination with Ace Green Recycling

Ace Green Recycling represents Athena’s current primary business combination candidate selected based on criteria emphasizing growth prospects, massive operational synergy opportunities via inorganic expansion paths common among recycling technologies/innovations aligned under environmental sustainability themes—a sector attracting growing institutional visibility within tech-adjacent asset classes [N1][S1].

Terms stipulate that Ace Green shareholders will receive shares tied not just deterministically but also incentive-linked earnouts structured around trading price milestones spanning five years after closing. Up to an aggregate total issuance cap exceeding ten million earnout shares could materialize thereby diluting existing holders but aligning interests towards valuation outperformance post-merger [S1].

Athena’s use of proprietary sourcing channels underscores intimate market knowledge advantages although ultimate value hinge hinges on pragmatic execution effectiveness integrating operational pipelines rather than sheer financial engineering alone—a core challenge transitioning from SPAC shell status toward bona fide operating company.

Key Risks Impacting Future Viability and Market Standing

The foremost existential threat pertains squarely on timing: failure to complete any inaugural business combination before mandated deadlines would trigger mandatory liquidations pursuant to charter provisions stripping shareholder value entirely—a non-trivial risk currently aggravated by prolonged negotiation cycles undermining investor confidence [N1][S23][S28].

NYSE has already flagged listing compliance risks rooted directly in missed milestones characteristic for mid-life SPACs struggling past their implicit ‘use it or lose it’ windows raising delisting probabilities tightening external financing avenues further constraining maneuverability amid sponsor dependency dynamics [N1][S10].

Dilutionary potential from extensive earnout share issuances together with tranche payouts embedded within sponsor voting/support agreements could pressure long-term capitalization structures reducing residual economic ownership stakes for early public investors post-merger approval creating complex governance considerations going forward [S9][S19].

Continued reliance on sponsor funding channels subjects liquidity positions susceptible to shifts outside direct control while absence of baseline revenue leaves Athena exposed purely as acquisition vehicle reliant solely on deal closure execution—factors collectively heightening investment risk monitoring requirements critical pre-close.

Outlook and Critical Milestones Ahead

Looking forward, the principal near-term event is completion of the business combination transaction by April 14, 2026—the last allowable extension date agreed through multiple amendments governed by their certificate provisions enabling incremental time gains albeit diminishing sponsor patience and market goodwill simultaneously [N1][S3][S21].

Investor attention should focus sharply on impending proxy solicitation votes where quorum achievement driven heavily by initial stockholder voting commitments holds decisive sway amid fragmented public holder interest given constrained liquidity positions limiting activist power triggering stockholder redemption demands post-announcement remain integral as well.

Secondary triggers include finalizing merger financing terms encompassing repayment/conversion treatment for working capital facilities along with regulatory cleared listings confirmations impacting trading continuity risks relevant post-close scenario planning needs preparedness for liquidation scenarios if target approval falls short or market conditions impair deal viability—a credible contingency under current stretched circumstances carrying multi-stakeholder impacts across share class complexities evident since IPO inception.

Absent explicit revenue generation capabilities before closing owing inherent SPAC structures means fundamental valuation hinges ultimately on consummation success metering subsequent integration effectiveness defining whether residual embedded promise converts sustainably or dissipates upon formal dissolution.

This report synthesizes publicly available SEC disclosures and recent news sources related specifically to Athena Technology Acquisition Corp. II without speculative projections or investment recommendations. It aims solely to provide a nuanced internal perspective across financial trends and strategic developments within defined regulatory frameworks governing blank check company transitions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments