Uranium Energy Corp's Strategic Expansion Through Vertical Integration and Physical Inventory

UEC leverages its low-cost ISR mining, a growing physical uranium stockpile, and refining capabilities to capitalize on rising domestic uranium demand amid favorable policy support.

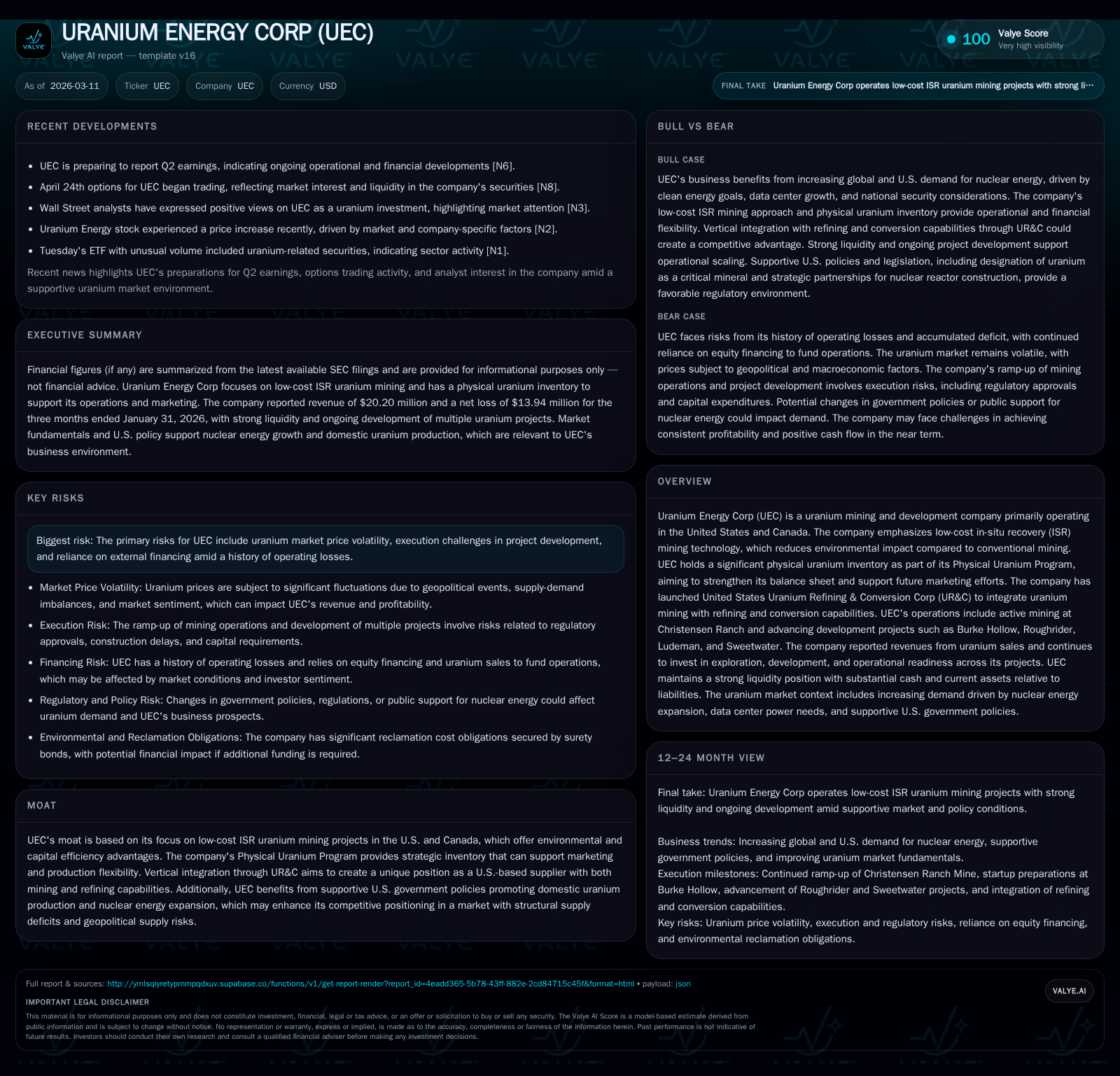

Uranium Energy Corp (UEC) has built its growth around low-cost in-situ recovery uranium mining primarily in the U.S. and Canada, complemented by a strategic Physical Uranium Program that bolsters liquidity and marketing flexibility. Operational revenues emerged notably since FY2023 driven by Christensen Ranch ramp-up, though operating losses have deepened reflecting ongoing development investments. The launch of United States Uranium Refining & Conversion Corp (UR&C) marks vertical integration into refining and conversion, enhancing supply chain control and positioning UEC to benefit from increasing U.S. government incentives promoting domestic nuclear fuel production. Liquidity remains ample via multiple equity raises underpinning capex for exploration and project development with a focus on scaling production and securing origin premium sales in a structurally tight global uranium market.

Robust Historical Growth Routed in Strategic ISR Mining

Uranium Energy Corp (UEC) has demonstrated significant revenue acceleration beginning with fiscal year 2023 when it commenced uranium sales linked to its operational ramp-up at Christensen Ranch Mine. Fiscal year 2023 revenue stood at approximately $164 million, advancing dramatically from $22.4 thousand in FY2022 — essentially transitioning from pre-production to active commercialization. However, this surge was accompanied by an operating income reversal; FY2023 marked a modest operating profit of $8.9 million but was followed by steep operating losses totaling $56.4 million in FY2024 and further expanding to $73.3 million in FY2025 [F1].

These operating losses reflect deliberate capital allocation toward project development, exploration, operational scale-up costs, and general corporate expenses required during the strategic growth phase. While net income turned negative in FY2023 ($-3.3 million), losses deepened to $29.2 million in FY2024 and significantly increased to $87.7 million in FY2025 [F1]. This operational trajectory aligns with the company's planned expansion emphasizing low-capital-intensive ISR techniques, which allow for relatively rapid development cycles compared to conventional mines.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 67 | -88 | -64 | -73 | +29737.9% | -200.0% |

| 2024 | 0 | -29 | -106 | -56 | -99.9% | -783.6% |

| 2023 | 164 | -3 | 73 | 9 | +609.8% | -163.0% |

| 2022 | 23 | 5 | -53 | -23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -70 | -8.9 |

| 2024 | -108 | -3.8 |

| 2023 | 72 | -0.5 |

| 2022 | -54 | 1.6 |

Source: SEC companyfacts cache [F1].

*Decline partially driven by shift from purchased uranium sales in inventory-building years.

Physical Uranium Program: Bolstering Flexibility Amid Market Fluidity

UEC’s Physical Uranium Program represents a forward-looking tactical asset accumulation strategy where uranium is purchased on the spot market at prices below average global mining costs—as of January 31, 2026, UEC held approximately 1,456,000 pounds of physical purchased uranium with all purchase commitments fulfilled [S2]. This substantial inventory serves multiple distinct purposes: strengthens the balance sheet amidst commodity price appreciation; supplies strategic inventory for future marketing flexibility with utility customers; and maximizes availability of the company’s domestic production capacity for premium-priced U.S.-origin contracts aligned with evolving government procurement initiatives such as the Uranium Reserve under the Nuclear Fuel Working Group recommendations [S2][S3].

This physical stock wisely positions UEC to capitalize on anticipated origin premiums that utilities are increasingly willing to pay for non-Russian sourced uranium amidst geopolitical tensions reshaping supply chains [S27]. It mitigates some exposure to pure mining upstream volatility by offering a ready-to-sale inventory book that can be deployed tactically depending on prevailing market conditions.

Vertical Integration through UR&C: Enhancing Control over the Fuel Cycle

A defining element of UEC’s strategic expansion is the establishment of United States Uranium Refining & Conversion Corp (UR&C), which integrates refining and conversion capabilities into its existing mining operations—a significant vertical step towards controlling more facets of the nuclear fuel supply chain domestically [S2]. This move enhances UEC’s competitive position against traditional producers who often depend on external refiners or international infrastructure.

In a sector where geopolitical supply insecurities are intensifying due to sanctions on Russian nuclear suppliers and supply chain reconfigurations across Europe and North America, UEC gains potential pricing power but also fulfills emerging governmental mandates for domestic fuel cycle completeness [S23]. The synergy reflects an understanding that successful near-term scaling requires not only mined ore but also reliable processing pathways.

Government Supports and Geopolitical Factors Fueling Demand

Demand tailwinds for UEC’s assets are markedly supported by bipartisan U.S legislative actions including the Nuclear Fuel Security Act, Inflation Reduction Act provisions incentivizing domestic nuclear energy production, alongside a range of other policies collectively aimed at boosting energy independence while expanding clean baseload power generation capacity [N6][S23]. These policies seek to develop robust domestic nuclear fuel cycles against a backdrop of rising global electricity demand projected to increase approximately 3.6% annually through 2030—and even faster in data center fueling driven by AI infrastructure expansion per Goldman Sachs forecasts [S2].

Furthermore, structural deficits exist between uranium production versus requirements globally—projected mid-case shortfalls near 67 million pounds U3O8 annually through 2026 accumulating beyond 340 million pounds within a decade—highlighting entrenched underinvestment faced by legacy producers while secondary inventories wane [S27]. This dislocation portends elevated pricing power for U.S.-based suppliers like UEC positioned with both resource base and processing capability.

Navigating Financial Profile: Capital Raises, Operating Metrics, and Cash Flows

UEC’s financial posture benefits from robust liquidity supported primarily through repeated equity financing programs—at-the-market offerings (ATM) led by Goldman Sachs among others—public offerings completed as recently as October 2025 yielding gross proceeds above $230 million including over-allotment options exercised [S12][S21][S25]. As of January 31, 2026 cash & equivalents stood at $486 million with current assets near $598 million against liabilities just over $20 million delivering an exceptionally healthy current ratio exceeding 28x signaling strong working capital sufficiency [F1][S4][S18].

The company continues experiencing net operating cash flow deficits reflecting front-loaded mineral property expenditures ($44.6 million during six months ended January 31, 2026) supporting exploration/extraction readiness principally across Roughrider, Burke Hollow, Christensen Ranch projects plus administrative expense inflation contributed by expanded headcount needs offsetting gross profits from purchased uranium sales ($10 million gross profit reported) [F1][S5][S10][S19].

Capital expenditures increased substantially reaching $5.48 million for FY2025 consistent with scaling production operations contrasted with modest prior levels; this capex focuses largely on facility expansions plus site readiness rather than speculative investments alone indicating strategic deployment towards commercial output growth [F1]. Shareholders’ equity grew steadily surpassing $984 million evidencing dilution funding model supporting aggressive development trajectory albeit without debt leverage burdens clearly measurable currently [F1]. This combination shows ongoing dependence on equity markets balanced against improving operational contributions.

Development Pipeline: Project Progress and Exploration Focus

The company’s multi-project footprint illustrates staged advancement spanning operational extraction readiness to near-term pre-extraction completion approaching full production phases.

- Christensen Ranch Mine continues ramp-up producing over ~114k pounds of precipitated uranium during H1 FY26 with expectation for further growth as new areas become operationally active [S10][S19].

- Burke Hollow achieved final construction milestones preparing startup pending state regulatory reviews emphasizing ‘pre-extraction’ phase compliance critical for go-live timelines [S19].

- Roughrider Project undergoing resource expansion drilling campaigns allocating >$4 million recently targeting reserves growth enabling future mine life extensions along ISR technology pathways [S5][S10].

- Ludeman drilling accelerated focusing on feasibility-scale data collection while Sweetwater mill refurbishment engineering is underway positioning that flagship Canadian deposit closer towards economical utilization adding refining throughput synergy downstream via UR&C integration plans [S19].

Other projects remain held in ‘operational readiness’ states meaning expenditures continue primarily on permit maintenance plus minimal labor force retention pending resource evaluation or regulatory clearance maintaining flexibility while minimizing capital consumption beyond essentials.

What to Watch: Market Prices, Regulatory Milestones, and Production Scaling

Near-term monitoring indicators include uranium spot price trajectories impacting timing/volume decisions on sales from physical inventory—the program underpins liquidity but is sensitive to market volatility typified most recently by prices oscillating between ~$85-$101 per pound reflecting short-term supply/demand imbalances alongside geopolitical uncertainties notably post Russia-Ukraine invasion restrictions reshaping sourcing patterns [N2][S27][N6].

Additionally, progress at UR&C refining capacity buildouts will be critical benchmarks influencing vertical integration returns alongside planned federal contracting opportunities associated with national enriched uranium reserves—a component poised to drive origin-premium domestic sales possibly facilitating higher-margin commercial deals for UEC loads.

Production scaling success including timely regulatory approvals especially concerning new wellfields/infrastructure necessary to deliver sustained ISR output will directly condition cash flows generation capacity shifting operating losses downward over time similarly key will be contract awards emerging amid utilities' renewed long-term contracting trends restoring pricing visibility previously eroded during market doldrums.

This report synthesizes public filings and verified disclosures without speculative forecasts or investment recommendations.It aims solely to convey a detailed analytical perspective based on disclosed financials, capsule operational narratives,and material market shifts affecting Uranium Energy Corp as of early calendar year 2026. All figures represent data compiled up to reports filed by March 10th, 2026.The reader should consider further institutional research when evaluating risk/return profiles associated with this specialty commodity-focused entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments