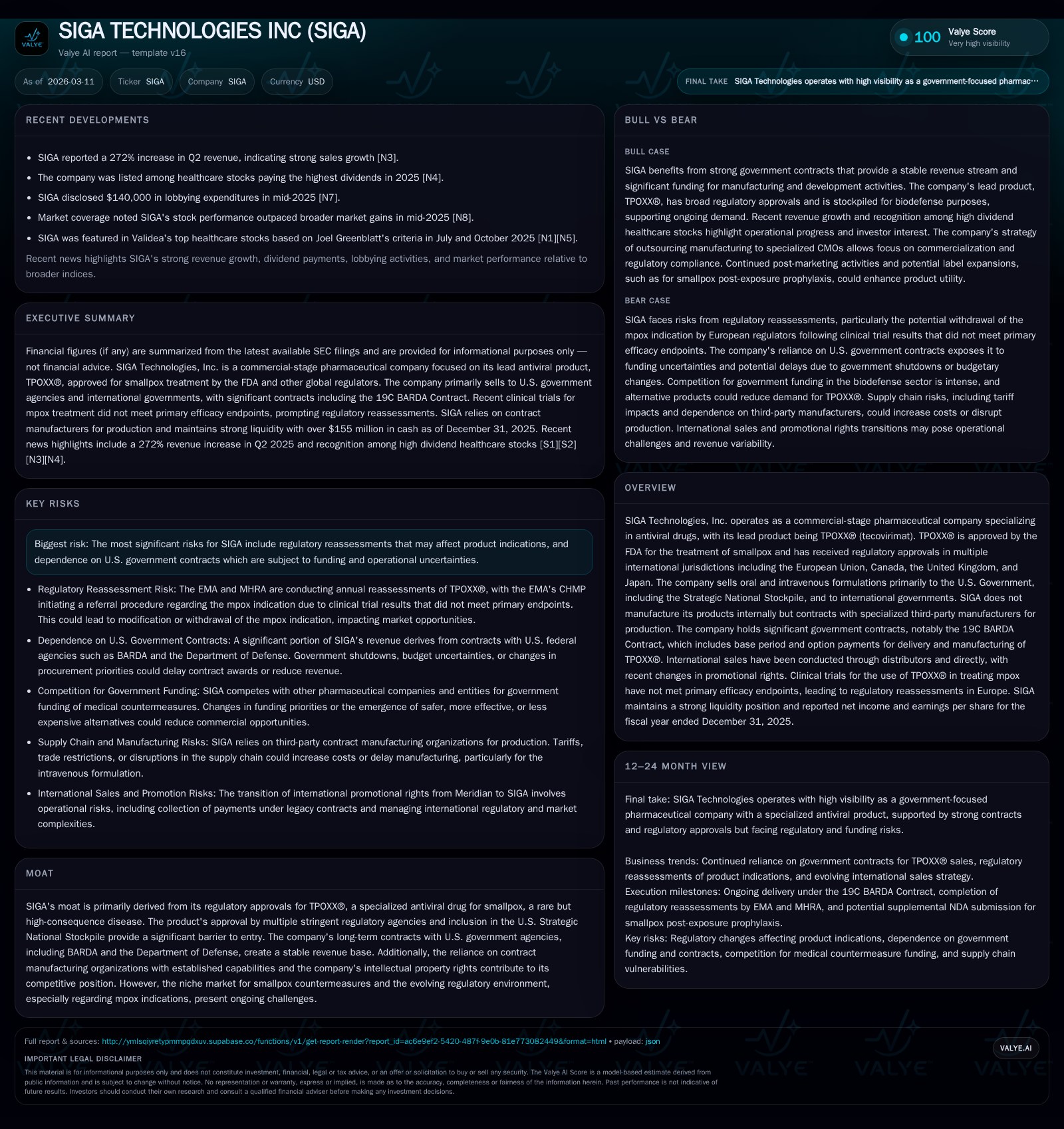

SIGA Technologies’ Trajectory: Balancing Government Contracts and Regulatory Risks

SIGA's antiviral niche anchors stable revenues amid shifting regulatory approvals and government contract dependencies.

SIGA Technologies focuses on providing TPOXX®, an FDA-approved antiviral for smallpox, primarily through U.S. government contracts including the 19C BARDA contract. Its financial performance over recent years shows strong revenue growth driven by government procurement but with noticeable volatility in income reflecting contract timing and expense dynamics. The company's reliance on government funding presents both a stable revenue base and vulnerability to political and budgetary uncertainties. Regulatory developments, especially from international agencies reviewing TPOXX®'s mpox indication, impose ongoing market access challenges. Capital allocation reflects solid profitability and dividend payouts, while operations hinge on a third-party contract manufacturing model that balances flexibility with supply chain risks.

Historical Financial Performance and Key Growth Drivers

SIGA Technologies’ financial history over the past several years portrays a company leveraging its specialized antiviral offering, TPOXX®, predominantly through government contracts. Revenues expanded markedly from $1.57 million in 2018 to $4.26 million in 2019 [F1]. This foundational growth set the stage for accelerated top-line expansion fueled chiefly by deliveries under the pivotal 19C BARDA Contract — a multi-year fixed-price agreement with option periods substantially exercising SIGA's manufacturing and delivery commitments.

This contract has largely shaped SIGA’s operating income trajectory: a peak operating income of approximately $83.6 million in 2023 descended sharply to $23.7 million in 2025 [F1]. These oscillations stem from the timing of option exercises under the BARDA contract and associated cost recognitions, typical within fixed-price arrangements where expense recognition may outpace revenue recognition depending on backlog fulfillment schedules.

Net income mirrored this pattern, reaching $68.1 million in 2023 before contracting to roughly $23.3 million by year-end 2025 [F1]. Operating cash flow remained relatively robust despite income dips — generating nearly $43.5 million in 2025 — signaling sustainable cash generation capability from core government procurements [F1]. Capital expenditures have been minimal relative to revenues (~$29K in 2019 versus larger earlier investments), aligned with SIGA’s capital-light commercial model reliant on third-party manufacturers [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 23 | 43 | 24 | -60.7% |

| 2024 | 59 | 49 | 70 | -13.0% |

| 2023 | 68 | 95 | 84 | +100.8% |

| 2022 | 34 | 42 | 43 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 43 | 0 | 11.7 |

| 2024 | 43 | 0 | 27.4 |

| 2023 | 32 | 11 | 34.6 |

| 2022 | 33 | 13 | 19.9 |

Source: SEC companyfacts cache [F1].

Note: Some YoY changes reflect comparison gaps in data availability; however overall trends highlight contract-driven volatility.

Dependence on U.S. Government Contracts: Stability Meets Vulnerability

SIGA’s commercial operation centers fundamentally on its relationship with U.S. governmental bodies — predominantly under the Department of Health & Human Services serving through BARDA and the Department of Defense — as described extensively in the company's filings [S1][S2][S4]. The current revenue model includes fixed-price procurement contracts featuring base periods with multiple option years which provide conditional revenue but significant uncertainty depending on governmental decisions.

As of December 31, 2025, SIGA had seen the execution of all options under its prominent “19C BARDA Contract,” representing the lion’s share of its revenues [S1]. However, this accomplishment shifts critical exposure toward future contract awards or renewals which are subject to Congressional appropriations processes and political considerations that could delay or reduce funding levels [S2]. The company highlights that failure to secure follow-on contracts promptly would materially jeopardize operational continuity given the absence of diversified revenue streams [S1][S4].

Financially this manifests as sizeable liquidity buffers; at year-end 2025 SIGA’s current ratio was near 11.83x reflecting approximately $213 million in current assets against $18 million current liabilities — a strong solvency position counterbalancing contracting uncertainty [F1]. Yet dependence on government budgets infuses risk into revenue predictability as exercise of options remains discretionary without guaranteed continuation orders [S1]. Extended federal shutdowns introduce further delays affecting contracting offices causing operational disruptions [S2][S24].

This contracting framework requires SIGA to carefully manage fixed pricing risks inherent in estimating manufacturing costs upfront; failure to control production expenses could compress margins due to fixed reimbursement rates [S1]. Additionally government contract compliance injects rigorous regulatory oversight including audit mechanisms capable of retroactive financial impacts or sanctions if non-compliance is detected [S4][S25][S30].

Regulatory Landscape Influences on Market Access and Future Demand

TPOXX® benefits from an unusual global regulatory footprint reflecting its biodefense orientation. It earned FDA approval for oral formulation in July 2018 and intravenous use in May 2022 explicitly targeting smallpox treatment [S1][S21]. Beyond the U.S., marketing authorizations have been granted by EMA (European Medicines Agency), MHRA (UK), PMDA (Japan), and Health Canada for orthopoxvirus diseases including smallpox as well as mpox (monkeypox) indications [S1][S21].

Importantly these approvals under "exceptional circumstances" confer marketing licenses conditioned on continued safety monitoring due to ethical constraints precluding traditional efficacy trials for rare viral threats [S1]. As such regulators demand annual reassessments that weigh emerging post-market data on benefit-risk profiles to determine ongoing authorization validity.

Recently on July 24, 2025 EMA's Committee for Medicinal Products for Human Use initiated a referral procedure questioning TPOXX®’s efficacy against active mpox following clinical trial results scrutiny specifically assessing randomized placebo-controlled studies conducted in the Democratic Republic of Congo and elsewhere [S1][S21][S22]. This procedural escalation introduces potential regulatory headwinds affecting European sales channels should adverse reassessments lead to label restrictions or withdrawal.

Complementing FDA activity is an ongoing supplemental NDA (new drug application) submission for label expansion covering post-exposure prophylaxis (PEP) against smallpox estimated now within twelve months following delays linked mainly to external CDC trial sample analyses impacted by governmental shutdowns [S21][S25]. Success here could unlock further government procurements enhancing TPOXX®'s market scope domestically.

Moreover SIGA operates within complex multi-jurisdictional regulatory environments where requirements vary drastically between countries influencing clinical trial design mandates, labeling conditions, pricing frameworks and reimbursement eligibility [S4]. Such complexity necessitates rigorous post-approval pharmacovigilance commitments including fulfillment of data collection obligations imposed by exceptional circumstance approvals globally.

Forward-Looking Outlook: What to Watch in Contracts and Approvals

At present no explicit forward revenue or earnings guidance has been offered outside previously disclosed target timelines around supplemental NDA submissions and international regulatory proceedings [N/A news; S1][S2]. Consequently monitoring future business momentum pivots critically around:

- U.S Government decisions about renewal or replacement procurements related to TPOXX®, given the expiration of prior BARDA Contract options at end-2025.

- Outcomes of EMA's ongoing referral procedure regarding mpox indication validity which could materially affect European market access.

- Progression of supplemental new drug applications targeting broader label expansions such as smallpox post-exposure prophylaxis which could enhance procurement volumes domestically.

- Possible geopolitical shifts or public health emergency declarations motivating government stockpile replenishment programs.

Due to dependence on FY Congressional appropriations cycles impacting BARDA budget allocations any delays or uncertainties therein may constrain contracting prospects or postpone deliveries extending working capital pressure periods [S2][S24]. The company further notes that procurement contracts will likely remain predominantly fixed-price with moderate inflation escalations requiring careful cost management going forward [S1].

Internationally SIGA’s emerging direct sales push since reacquisition from Meridian Medical Technologies adds strategic focus but also susceptibility as collection cycles rely partly on third-party distributors managing customer relationships outside North America [S14]. The ramp-up pace of global biodefense markets remains uncertain thus broadening exposure alongside concentrated product reliance.

Capital Allocation Patterns: Profitability, Cash Flow, and Shareholder Returns

Capital efficiency metrics underscore strong profitability albeit somewhat volatile given contracting terms discussed prior. For fiscal year ending December 31, 2025:

- Net income stood at approximately $23.3 million yielding an estimated ROE near 11.7%, derived by dividing net income by shareholders’ equity totaling about $198.8 million year-end [F1].

- Operating cash flow remained robust at $43.47 million underpinning structural business cash generation capabilities despite net income contraction compared with prior peak years.

- SIGA paid dividends exceeding $43 million in both FY2024 and FY2025 reflecting consistent shareholder return priorities while curtailing share repurchases since FY2024 suggests prudent treasury management amidst uncertain contracting landscape [F1].

- Capex remained negligible (>0), consistent with outsourcing manufacturing strategy that limits heavy internal plant investments reducing fixed asset burdens.

The combination of strong free cash flow conversion supports ongoing dividend distribution capacity while preserving balance sheet strength offering operational flexibility should contracting revenues slow unexpectedly or incremental R&D investments be pursued for label expansions or new countermeasures development efforts paralleling industry norms.

Future capital deployment choices are expected to continue balancing returns maintenance against required investments aligned with evolving biodefense market trends described above.

Contract Manufacturing Model: Operational Implications in Supply Chain

Unlike many pharmaceutical peers owning internal production complexes SIGA employs a fully outsourced manufacturing paradigm engaging specialized contract manufacturing organizations (CMOs) for producing TPOXX® oral and intravenous formulations [S1]. This approach confers several advantages:

- Flexibility scaling output volumes responding dynamically to option exercises under government contracts avoiding sunk costs endemic to owned facilities.

- Focus investment capital toward commercialization activities such as regulatory affairs or marketing rather than costly plant upgrades.

- Leveraging CMO expertise meeting stringent quality standards essential for biodefense products destined for national stockpiles subjected to federal audits.

However this dependency introduces operational vulnerabilities notably:

- Risk concentration if CMO partners fail meeting delivery deadlines or quality benchmarks potentially disrupting timely government stockpile replenishment obligations leading to penalties or lost future contracts.

- Limited daily operational control requiring rigorous supplier oversight programs ensuring compliance with applicable FDA cGMP regulations alongside foreign health authority mandates governing export shipments.

- Supply chain disruptions originating externally such as raw material shortages or logistical constraints amplifying operational risks intrinsic within fixed-price contract frameworks.[S13][S23]

Consequently SIGA must maintain proactive supply relationships mitigating embargoes or geopolitical trade sensitivities relevant especially given national security orientations inherent within biodefense product supply chains.

Disclaimer: This analysis summarizes available public data and SEC filings without incorporating any non-public material information nor providing investment recommendations or price forecasts concerning SIGA Technologies Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments