AeroVironment’s Strategic Evolution amidst Contracting Revenues and Rising Compliance Demands

AeroVironment addresses declining revenue and intensifying regulatory requirements by leveraging its unmanned systems expertise and government relationships.

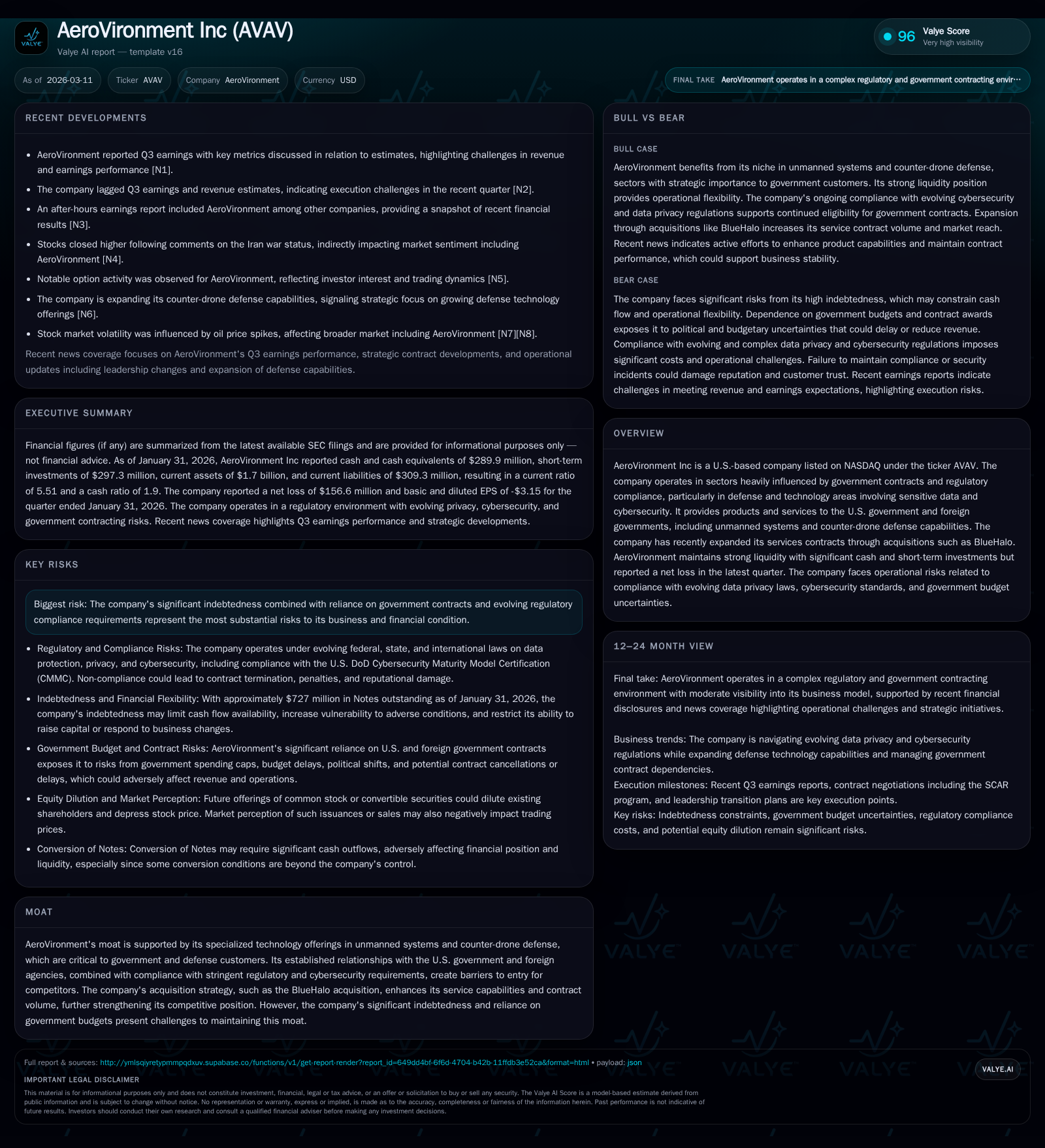

AeroVironment Inc has experienced a contraction in revenues and profitability over recent fiscal years, reflecting headwinds in defense contracting timing and budget uncertainties. Regulatory compliance, especially around data privacy and cybersecurity in government contracts, is becoming increasingly complex and costly. The company's strategic acquisition of BlueHalo expands its service contract footprint, partially offsetting challenges. However, elevated indebtedness constrains financial flexibility amid shrinking operating cash flows. The firm’s near-term outlook hinges on navigating U.S. government budget cycles, export license timelines, and adherence to evolving cybersecurity standards.

Revenue Downturn and Profitability Trends: A Historical Performance Review

AeroVironment has faced a notable downturn in revenue generation culminating in FY2025. Annual revenue slid by approximately 6.4% year over year to $117.4 million [F1], underscoring a contraction in new contract awards or delayed government spending patterns common in defense sectors characterized by unpredictable budget cycles.

Operating income fell sharply by 43.2% relative to the prior fiscal year, dwindling to about $40.8 million [F1]. This significant compression contrasts with prior years where AeroVironment returned to modest profitability following sizable losses recorded in FY2023 (-$178.7 million operating loss) linked presumably to restructuring charges or asset impairments within program adjustments [F1]. Net income echoed this trend showing a diminished gain of $43.6 million after the FY2023 loss spike [F1].

Operating cash flow displayed increased stress, flipping negative at roughly -$1.3 million for FY2025 from positive $15.3 million the year prior [F1]. Capital expenditures held steady near $22.8 million [F1], reflecting ongoing investments in technology platforms despite shrinking cash generation capability.

This financial snapshot reveals AeroVironment grappling with scalability challenges inherent in government contracting where timing of awards and billing strongly impacts near-term cash flows.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 44 | -1 | 41 | 23 | -26.9% |

| 2024 | 60 | 15 | 72 | 23 | +133.9% |

| 2023 | -176 | 11 | -179 | 15 | -4109.5% |

| 2022 | -4 | -10 | -10 | 22 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | |

| 2024 | -8 | |

| 2023 | -3 | -32.0 |

| 2022 | -32 | -0.7 |

Source: SEC companyfacts cache [F1].

Table shows AeroVironment's annual revenue, income, cash flow trends highlighting the recovery trajectory from large losses yet ongoing revenue softness.

Government Contracts and Regulatory Landscape: Implications for Future Growth

Constitutive of AeroVironment’s business model is heavy reliance upon U.S Department of Defense (DoD) contracts alongside international governmental agreements anchored by export licenses [S10][S11]. This dependence injects significant exposure to federal budget volatility including appropriations delays or continuing resolutions that frequently disrupt program funding cadence leading to deferred contract awards or payment bottlenecks [S11]. The company explicitly warns that any U.S government shutdown could hamper execution under current programs especially post-BlueHalo acquisition which expanded the services contracts considerably [S11].

Furthermore, evolving regulatory compliance demands impose incremental operational costs that may constrain margins or limit contract qualifications:

Compliance with the DoD’s Cybersecurity Maturity Model Certification (CMMC) framework is mandatory for continued contract eligibility; costs related to achieving and maintaining certification are substantial and can escalate [S8]. Failure here risks suspension or loss of contracts.

Data privacy regulations across jurisdictions—primarily the European GDPR and California’s CCPA—increase complexity surrounding customer data handling protocols consistent with contractual confidentiality clauses [S4][S9]. The rapid evolution of these laws introduces uncertainty regarding ongoing compliance costs.

Non-compliance scenarios might trigger legal action or reputational damage affecting future contract awards [S7][S8]. Moreover, international export license delays can impair fulfilment capacity for overseas clients limiting revenue growth trajectories [S11].

This layered regulatory environment requires sustained internal controls investments and agile risk management to safeguard AeroVironment’s position as a preferred government contractor.

Counter-Drone Development and Service Expansion: Innovations Enhancing the Moat

AeroVironment maintains a competitive moat through specialized unmanned system technologies encompassing UAVs and cutting-edge counter-drone defense solutions tailored for modern warfare contingencies [N7]. The integration of acquisitions like BlueHalo notably increased the company's service contract volume, allowing it to offer more comprehensive support services alongside product sales—a critical factor enhancing customer retention amid high contract capture rates typical of defense procurement cycles .

Strategically, these moves position AeroVironment to capitalize on Contract Modification Events (CMEs), which often result from shifting defense priorities requiring flexible responses from suppliers [N7]. Export licenses remain an operational sensitivity influencing international sales timelines but AeroVironment’s increasingly integrated product-service model amplifies competitive barriers by bundling deliverables across the drone lifecycle.

The company's focus on developing commercial versions of military technology (e.g., phased-array BADGER antenna systems post-stop work negotiations) signals intent to exploit adjacent civilian markets thereby diversifying end-market exposure somewhat beyond traditional defense budgets [S27].

Financial Health Spotlight: Indebtedness, Liquidity, and Capital Structure

On balance sheet metrics at January 31, 2026 reveal $727 million aggregate principal indebtedness representing a substantial leverage burden reflecting debt issued partly for financing acquisitions like BlueHalo [S5][S12][F1]. This capped flexibility since servicing this level of debt consumes a notable portion of operating cash flow thus constraining discretionary investment options.

Liquidity snapshots are comparatively robust: current assets stood at $1.7 billion against $309 million current liabilities yielding a strong current ratio of approximately 5.5x—a considerable cushion for short-term obligations including working capital needs [F1]. However, aggressive leverage imposes restrictive covenants limiting capability to raise additional capital without covenant breaches while dilution risk lurks from convertible notes settlement via common stock issuance diluting existing shareholders if conversions occur ahead of maturity dates [S6][S12][S14].

Financial discipline remains paramount as AeroVironment navigates between deleveraging aims and continued R&D investment commitments intrinsic to sustaining technological relevance in its sector.

Capital Allocation Patterns: Shareholder Returns and Investment Priorities

AeroVironment historically refrains from dividends distribution while share repurchases have been minimal — small buyback programs dating back several years suggesting conservative capital return policies underpinned by internal reinvestment needs more than shareholder yield orientation [F1].

Capital expenditure outlays hovered around $22-$23 million annually during the observed period even as cash flows tightened—a clear indicator that sustaining technology platform upgrades remains a priority despite compressed free cash flow (negative approximately $24 million calculated as CFO minus capex for FY2025) [F1].

Return on equity measured roughly at 7.9% trails peer aerospace/defense averages hinting at capital intensity stress amid turbulent earnings volatility; restoring higher returns likely depends on stabilizing operational cash inflows and possibly debt reduction initiatives enabling freer allocation toward growth opportunities or investor distributions.

What to Watch: Contract Backlog, New Regulations, and Market Dynamics Shaping Near-Term Outlook

Absent explicit forward guidance from corporate disclosures on upcoming fiscal periods beyond existing SEC filings [N4], critical indicators for monitoring AeroVironment’s trajectory include:

- Backlog progression relative to recent quarters will shed light on whether pipeline momentum offsets risks from federal funding freezes or program cancellations triggered by political shifts.

- The speed at which export licenses are granted affects international order fulfillment directly impacting top-line recovery prospects.

- Successful navigation of evolving CMMC certification rounds will be crucial given government emphasis on cybersecurity resilience in contracting criteria.

- Geopolitical developments heightening demand for unmanned systems or counter-drone capabilities could improve tender volume but remain subject to congressional budgetary approval dynamics posing downside risks.

Overall, the interplay between expanding compliance burdens, leveraged balance sheet management, contracted revenues, and innovation-driven moat preservation places AeroVironment at an inflection point demanding careful operational deftness aligned with governmental procurement cycles.

This analysis assembles information solely from official company filings ([F1],[S#]), recent news reports ([N#]), and recognized regulatory disclosures through March 2026 without speculative extrapolation beyond documented facts. The content should not be construed as investment advice but rather as an independent evaluation aimed at institutional research audiences seeking nuanced understanding of AeroVironment's business environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments