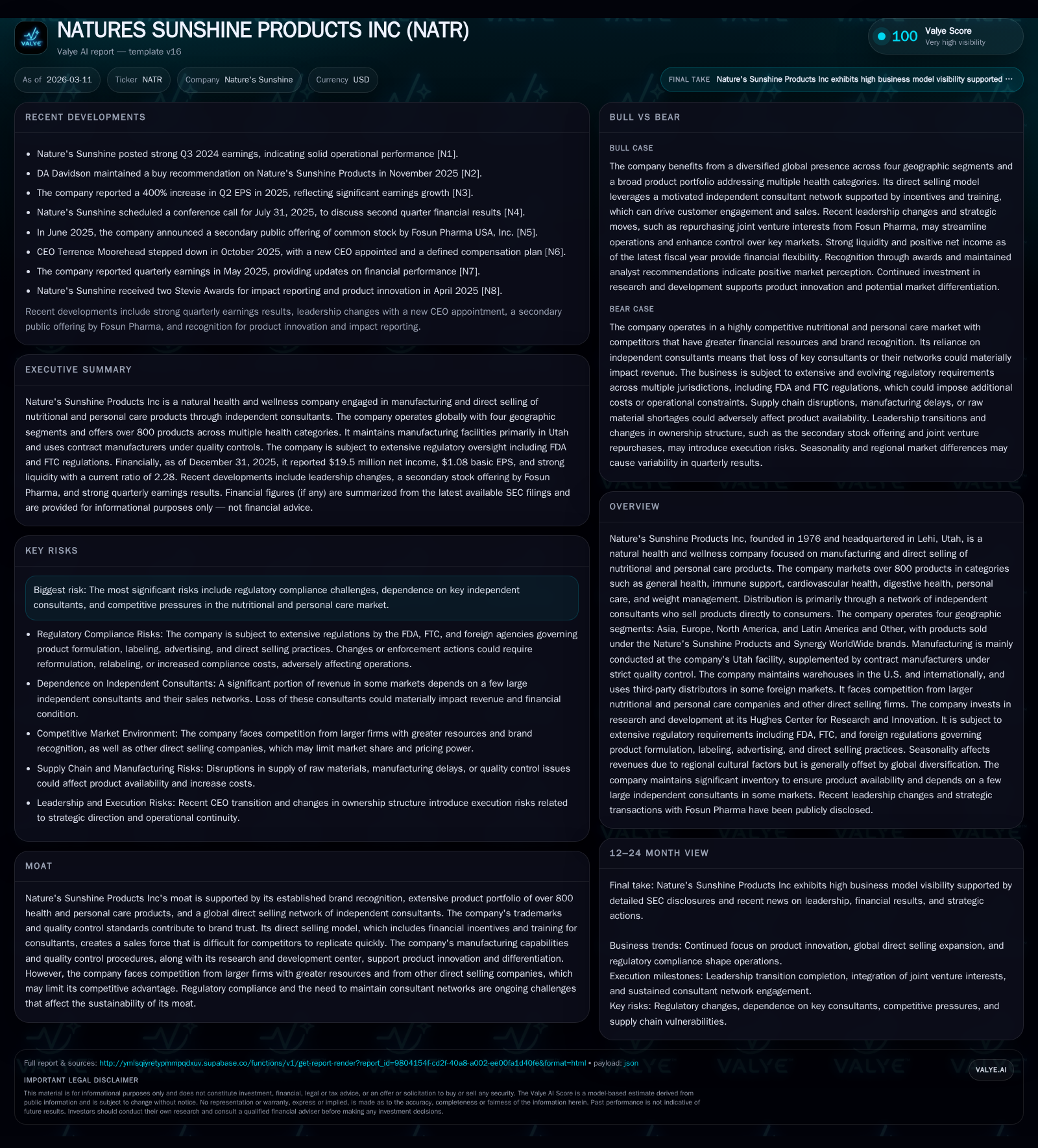

Nature’s Sunshine Products Inc: Unpacking a Turnaround in Health and Wellness Retail

Examining Nature’s Sunshine Products' financial resurgence alongside regulatory challenges shaping its direct selling business.

Nature's Sunshine Products Inc has demonstrated a notable financial turnaround marked by revenue growth and significant net income improvement, supported by operational efficiencies and consultant network expansion. This revival occurs within a complex regulatory environment, featuring ongoing trade compliance investigations and evolving direct selling regulations, especially in Asia. Geographic sales dynamics and product portfolio diversification underpin sales resilience, while strong cash flows facilitate enhanced capital return activities. Investors should monitor regulatory developments and operational milestones that could materially affect growth trajectories and risk profiles.

The Financial Turnaround: Historical Performance and Key Growth Drivers

Nature’s Sunshine Products Inc has revitalized its financial health following years of steady performance. The company reported a revenue increase to $88.29 million in FY2025 from $83.93 million in FY2024, representing a solid year-over-year grow of approximately 5.2%. Operating income rose sharply to $24.74 million for FY2025 compared to $20.10 million the prior year—a 23.1% uplift highlighting improved operational efficiency. Net income accelerated even more dramatically to $19.52 million, up 153.7%, benefiting from margin enhancements and likely improved cost controls as well as the expanded reach of its independent consultant salesforce [F1][N1].

Operating cash flow reached $35.32 million in FY2025, increasing nearly 40% versus the previous year despite a reduction in capital expenditures to $6.48 million (-40.9% YoY), reflecting prudent investment aligned with optimizing existing manufacturing infrastructure primarily located in Spanish Fork, Utah [F1]. This financial trajectory evidences a pivot towards leaner operations and better execution across distribution channels.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 20 | 35 | 25 | 6 | +153.7% |

| 2024 | 8 | 25 | 20 | 11 | -49.0% |

| 2023 | 15 | 41 | 19 | 10 | |

| 2022 | 1 | 16 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 16 | 29 |

| 2024 | 9 | 14 |

| 2023 | 6 | 31 |

| 2022 | 14 | -7 |

Source: SEC companyfacts cache [F1].

The improvement is attributable to an expanded independent consultant base incentivized through enhanced compensation programs and training initiatives alongside stable product demand within core health categories [N1][S10].

Navigating Regulatory Headwinds in the Direct Selling Landscape

Despite recent financial gains, Nature’s Sunshine contends with significant regulatory pressures central to its direct selling model and product distribution framework. Since November 2024 the company has been engaged in an internal investigation concerning historic compliance with U.S. trade control laws culminating in voluntary disclosures to the Bureau of Industry and Security (BIS) and Office of Foreign Assets Control (OFAC) in September 2025 [S4][S14]. While these investigations cover breaches estimated at less than one percent of net revenue per year over recent fiscal periods—they pose risks of monetary penalties and increased compliance costs.

Moreover, direct selling regulations enforced by entities such as the FTC tightly govern sales compensation structures to prevent pyramid schemes based improperly on recruitment rather than bona fide product sales [S4][S8]. Key markets such as China and South Korea impose legal caps on consultant compensation which compel Nature's Sunshine to tailor incentive frameworks locally—introducing operational complexity [S4][S9][S15]. These geographic regulatory nuances demand ongoing adaptation that may constrain growth or require costly business model adjustments.

Beyond direct selling rules are extensive government regulations regulating dietary supplement formulation, labeling and advertising chiefly from the FDA within the U.S., alongside worldwide counterparts governing each local market [S5][S6][S22]. The company must navigate rigorous Good Manufacturing Practices (GMP) standards applied both internally at its Utah site and contract manufacturers internationally under strict quality control regimes [S10]. Advertising scrutiny by both the FTC and states’ attorneys general carries potential reputational risks if unsubstantiated claims emerge from independent consultants’ marketing efforts [S11]. Also notable is exposure to anti-bribery enforcement risk under the Foreign Corrupt Practices Act amid heightened DOJ/SEC vigilance particularly in China [S6].

Geographic Segmentation Impact on Sales Dynamics

Nature's Sunshine operates across four primary segments: Asia; Europe; North America; Latin America & Other—with Asia representing a strategically vital but regulatory challenging geography [S15][S24]. These segments operate under twin brands: Nature's Sunshine Products primarily for nutritional supplements and Synergy WorldWide focusing on personal care lines.

Each region's distinct regulatory environment shapes consultant compensation schemes—particularly direct selling restrictions holding sway most strongly in Asian markets which require capped earnings models limiting recruiter incentives relative to other regions [S4][S15][S26]. Correspondingly consumer cultural norms influence direct selling adoption rates—for example mature direct sales markets like North America tend to have more established consultant networks whereas emerging economies reflect more volatile sales cycles affected by seasonality like Lunar New Year impacts [S26].

The Latin America & Other segment uniquely includes wholesale distribution partnerships granting regional autonomy but buffering against some direct compliance burdens while enabling broader market access [S24]. Supply chain logistics also differ by region; international third-party distributors complement domestic warehouses facilitating smooth order fulfillment tailored appropriately for each geography’s operational constraints [S25].

Product Portfolio Evolution and Innovation Insights

The company's diversified product catalog encompasses over 800 formulations spanning six principal categories: general health (including subcategories such as blood sugar support and cognitive function), immune support designed for systemic reinforcement, cardiovascular supplements promoting heart health optimization, digestive aids regulating gastrointestinal functions, personal care offerings including botanically derived soaps and lotions, plus weight management products emphasizing meal replacements and caloric metabolism enhancers [S10].

Manufacturing is mostly centralized at their Utah facility certified for pharmaceutical-grade GMP compliance with supplemental contract manufacturing vetted rigorously for adherence to proprietary quality controls ensuring product consistency globally [S10][S21]. The Hughes Center for Research and Innovation plays a pivotal role sustaining pipeline vitality through clinical research validating new compositions or improving existing products enhancing competitive differentiation among nutraceutical peers [S21].

This breadth supports cross-selling within consultant networks fostering broader customer engagement across multiple wellness dimensions which helps mitigate dependency on single categories or seasonal fluctuations.

Capital Allocation Strategy: Strong Cash Flow Supports Shareholder Returns

Strong operating cash flow generation enabled Nature’s Sunshine to maintain disciplined capital allocation improving shareholder value principally through increased share repurchases totaling $16.3 million in FY2025 compared with $8.86 million the prior year while suspending dividends post-2021 aligns with reinvestment priorities despite historically modest dividend payouts [F1].

Capital expenditures contracted substantially (-40.9%) reflecting completion of previous capacity expansions or modernization at their Utah manufacturing plant consistent with their asset-light reliance on contract manufacturers abroad [F1]. Improved operating margins combined with moderate capital investment resulted in robust free cash flow (~$28.8 million), empowering greater balance sheet flexibility.

Equity has been efficiently leveraged yielding an approximate return on equity around 18.5%, demonstrating effective reinvestment of earnings bolstered by cost containment measures fostering upward momentum in profitability metrics [F1]. The company's liquidity remains sound with current assets exceeding current liabilities by over double supporting operational stability amidst external uncertainties.

Perspectives on Future Growth Opportunities and Constraints

While no formal forward guidance was provided apart from recent quarterly updates underscoring Q3 strength [N1], Nature's Sunshine highlights growth drivers including expansion of its independent consultant base through targeted training programs; development of novel formulations to capture evolving consumer wellness trends; and expansion into newer international markets facilitated by obtaining necessary regulatory approvals ahead of launching new products or entering fresh jurisdictions [N1][S1].

Conversely headwinds persist due to continuing scrutiny from trade sanction regulators impacting supply chain robustness; evolving FTC directives potentially mandating adjustments to sales compensation frameworks particularly affecting high-growth Asian regions; increased costs related to ensuring GMP certification globally; plus macroeconomic pressures such as currency fluctuations given significant non-U.S.-dollar denominated revenues that can compress reported earnings when translated back into USD reporting currency [S4][S23][N1]. Close monitoring of ongoing trade investigations’ outcomes will be critical.

Investor Takeaways: Milestones to Monitor and Risk Factors

Investors should track several key factors going forward: progress toward resolution or mitigation of export control investigations representing an imminent influence on compliance-related expense volatility; amendments implemented to comply with new or revised compensation caps particularly affecting Chinese or Korean markets; continued organic revenue growth supported by consultant network scale gains especially outside traditional core geographies; maintenance of GMP certification standards providing quality assurance integral to brand trust; expansion into emerging wellness categories driven by ongoing R&D output; sustained positive free cash flow generation funding buybacks; plus vigilance on reputational risks stemming from consultant advertising practices subject to FTC enforcement actions.

Risks are material given regulatory enforcement unpredictability intrinsic to multijurisdictional direct selling operations plus dependency on a limited number of high-performing consultants generating outsized portion of segment revenues introduces concentration risk if attrition occurs unexpectedly [S27]. The complexity inherent in balancing global trade compliance with maximizing distributor incentives forms a delicate governance tightrope necessitating continuous attention from management.

In conclusion, Nature’s Sunshine Products Inc exhibits compelling evidence of operational recovery underscored by strong financial metrics juxtaposed against inherent regulatory headwinds characteristic of nutraceutical direct selling companies operating cross-border. This duality requires stakeholders maintain vigilant oversight of evolving external constraints while appreciating underlying fundamentals strengthened through strategic execution internally.

This analysis is based solely on publicly available SEC filings ([F1], [S#]) and news sources ([N#]). It does not constitute investment advice but aims to provide an informed perspective on Nature's Sunshine Products Inc's historical performance, strategic challenges, and forward-looking considerations within the natural health products industry.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments