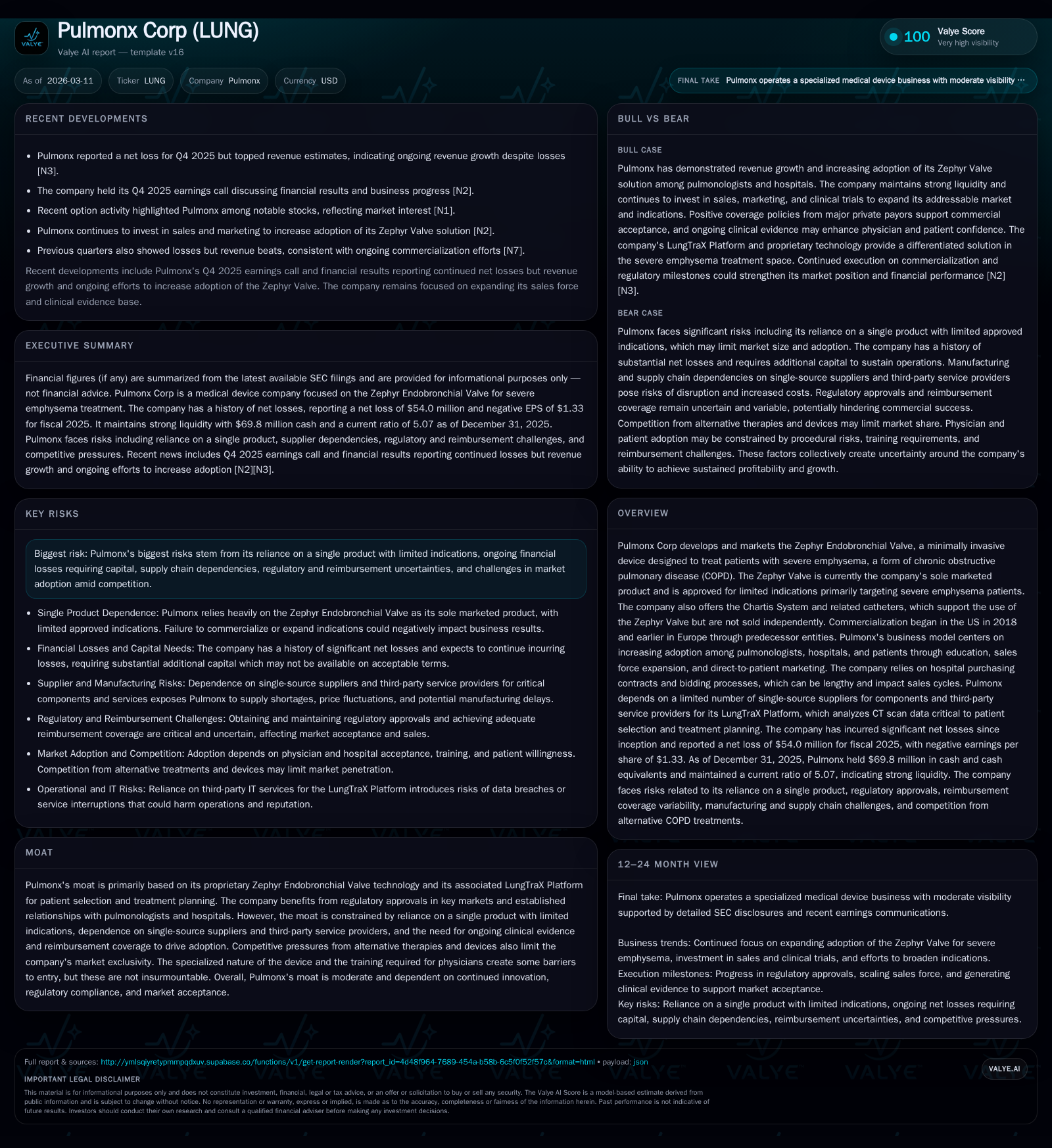

Pulmonx Corp’s Growth Challenges and Financial Strain from Single-Product Reliance in Severe Emphysema Treatment

Pulmonx Corp continues to expand adoption of its Zephyr Valve for emphysema amid persistent losses and regulatory headwinds.

Pulmonx Corp generates nearly all revenue from its proprietary Zephyr Endobronchial Valve, targeting severe emphysema patients with limited indications. Since initiating US commercialization in 2018, revenue growth has been modest with persistent operating losses exceeding $53 million in 2025. The company faces adoption hurdles stemming from dependence on single-product sales, lengthy hospital purchasing processes, reimbursement uncertainties, and an ongoing Department of Justice investigation settlement. Despite robust margins above 70%, Pulmonx’s negative cash flows and declining equity position underscore capital intensity amid investments in sales expansion and clinical trials. Scaling broader market penetration will depend on navigating manufacturing risks, regulatory approvals, competitor dynamics, and sustained clinical evidence.

Company Overview

Pulmonx Corp commercializes a minimally invasive treatment for patients suffering from severe emphysema through its flagship product, the Zephyr Endobronchial Valve. This valve is designed to improve lung function by reducing hyperinflation by occluding diseased lung lobes, offering an alternative to surgery for patients who are either unwilling or unsuitable candidates for more invasive procedures. Introduced commercially in the U.S. in 2018 following FDA pre-market approval (PMA), the Zephyr Valve has a longer history of availability in Europe beginning in the early 2000s under predecessor entities.

Complementing the valve technology are the Chartis Pulmonary Assessment System and LungTraX Platform aimed at refining patient selection criteria for optimal outcomes. Additionally, Pulmonx is advancing its pipeline with the AeriSeal System—a polymer foam designed to treat collateral ventilation—and is conducting pivotal global trials (CONVERT II) for FDA approval [S1].

Historical Performance & Growth Drivers

Annual revenues have grown steadily but remain concentrated solely around the Zephyr Valve system leveraging direct sales primarily within North America (95% of revenue). For fiscal year ending 2025, Pulmonx recorded $90.5 million revenue versus $83.8 million in 2024—reflecting an approximate 8% increase year-over-year driven by expanded sales force efforts and incremental hospital adoption [F1][S1]. Gross margins remain robust at roughly 74%, consistent with prior years, suggestive of efficient manufacturing cost control despite scale constraints.

However, profitability remains elusive with operating income losses at -$53.7 million for FY2025—a slight improvement compared to prior years but still indicative of ongoing heavy investment in commercialization infrastructure and product development [F1]. Net income losses echoed this trend at approximately -$54.0 million for the same period.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -54 | -32 | -54 | 452000 | +4.2% |

| 2024 | -56 | -32 | -58 | 1447000 | +7.3% |

| 2023 | -61 | -38 | -62 | 807000 | -3.3% |

| 2022 | -59 | -45 | -59 | 1318000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -33 | -99.8 | |

| 2024 | -33 | -65.7 | |

| 2023 | 0 | -38 | -51.4 |

| 2022 | 27000 | -46 | -38.3 |

Source: SEC companyfacts cache [F1].

Table: Pulmonx annual financial highlights showing steady revenue growth alongside persistent net losses and declining equity capitalization [F1]

Competitive Position & Moat

Pulmonx’s competitive edge primarily stems from its proprietary Zephyr Valve technology complemented by diagnostic platforms focused on patient selection—critical given emphysema's heterogeneous presentation among sufferers [S1]. Regulatory approvals including FDA PMA status and CE Mark certification underpin global marketing rights alongside reimbursement agreements in major geographies enhancing accessibility.

Nevertheless, the moat remains moderate:

- Product portfolio concentration solely on Zephyr Valve limits diversification benefits while broadening label indications is pending success of ongoing clinical trials.

- Adoption is constrained both by inertia within hospital purchasing systems involving protracted contracting cycles and physician preferences shaped by existing standards of care or alternative therapies such as bronchoscopic lung volume reduction approaches.

- Single-source suppliers coupled with manufacturing ramp risks could impair supply chain reliability.

- Training requirements imposed by device complexity create a barrier for new entrants but might also slow scaling velocity for Pulmonx itself as it educates pulmonologists across diverse healthcare settings [S1][S16][S18].

Risks & Challenges

Significant exposure arises from reliance on one primary product with limited FDA-approved indications which restricts addressable patient populations [S2]. The company faces various operational risks including:

- Negative cash flows: Operating cash outflows amounted to over -$32 million in FY2025 exacerbated by capital expenditures despite recent cuts [F1].

- Legal / Regulatory scrutiny: An ongoing U.S DOJ investigation into marketing and sales practices resulted in recorded settlement liabilities creating uncertainty around potential additional costs or reputational harm [S4][S5][S6].

- Product-related risks such as procedural complications (e.g., pneumothorax or procedure-related mortality) impose cautionary constraints on wider physician uptake.

- Reimbursement volatility remains a looming concern as payors periodically revise coverage criteria or limit payment rates affecting procedure frequency.

- Manufacturing scale-up hurdles coupled with dependency on third-party suppliers could disrupt supply continuity or inflate costs [S16].

- Limited long-term safety data may temper confidence among payors and clinicians until broader real-world evidence accrues.

Future Growth Prospects

Pulmonx targets growth through various strategic thrusts:

- Expanding U.S market share via larger sales organization deployment aimed at interventional pulmonologists coupled with direct-to-patient outreach campaigns to stimulate demand awareness.

- Geographic diversification maintaining distributor partnerships internationally while steadily increasing direct sales penetration.

- Advancing pipeline products such as the AeriSeal system through successful clinical trials could unlock expanded indications beyond current emphysema subsets [N1][S1].

- Continuing generation of high-quality clinical evidence supporting improved patient outcomes addressing quality-of-life improvements documented through measures like BODE Index scores may reinforce guideline endorsements worldwide.

- Pursuit of more favorable reimbursement coverage anticipating healthcare policymakers might adjust policies favoring less invasive management strategies vis-à-vis traditional surgeries.

However, growth ceiling derives from finite severe emphysema populations fitting current selection criteria; any decline in underlying COPD prevalence owing to reduced smoking rates constitutes a secular headwind over time [S16][S17].

Financial Outlook & Capital Allocation

No explicit forward guidance currently issued; however recent earnings commentary flags expectation for continued investments in sales capacity building alongside ongoing R&D directed at pipeline completion including CONVERT II trial milestones scheduled over coming quarters [N1][N2][S3]. Monitoring incremental improvements in product adoption rates alongside milestone readouts related to expanded label claims will be key indicators.

Capital structure reflects financial strain evidenced by diminishing shareholder equity—from approximately $154 million four years ago down to roughly $54 million post-loss absorption—highlighting recurring operating deficits necessitating external financing including debt facilities established most recently with Perceptive Credit Holdings [F1][S10][S12][S18][S3]. Liquidity appears sufficient near-term given cash reserves exceeding current liabilities (current ratio 5) but sustained negative free cash flow (-$33 million in FY2025 after capex) emphasizes ongoing need for careful cash management and potential capital raises if profitability thresholds remain unmet.

Dividend payments and share repurchases are effectively non-existent reflecting focus on reinvestment amid loss-making mode ([F1]).

Summary & What to Watch For

Pulmonx sits at a critical juncture balancing impressive innovation addressable only to a narrow patient subset against financial sustainability challenges typical of capital-intensive medtech startups focused on a singular proprietary device platform.

Key metrics to monitor include:

- Quarterly revenue trajectory vs historic moderate growth trends reflecting adoption momentum or stalls,

- Progress updates from pivotal clinical trials especially regarding AeriSeal,

- Developments around legal settlements impacting expenses or corporate governance,

- Reimbursement environment shifts influencing procedure penetration,

- Operating margin movements signaling scaling efficiencies or cost pressures,

- Cash burn rate relative to liquidity buffers informing possible financing needs.

Effective navigation of these elements will determine if Pulmonx can leverage its technological moat into broader commercial success or continue facing structural headwinds limiting profitability prospects.

Disclaimer: This analysis is based solely on publicly available information as cited; it does not constitute investment advice nor implies any recommendation regarding Pulmonx Corp securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments