Voyager Acquisition's SPAC Model Hinges on Healthcare Merger Execution and Capital Structure

Voyager Acquisition Corp., a Cayman Islands-based SPAC focused on healthcare, relies heavily on its upcoming merger to transition from a blank check company to an operating entity.

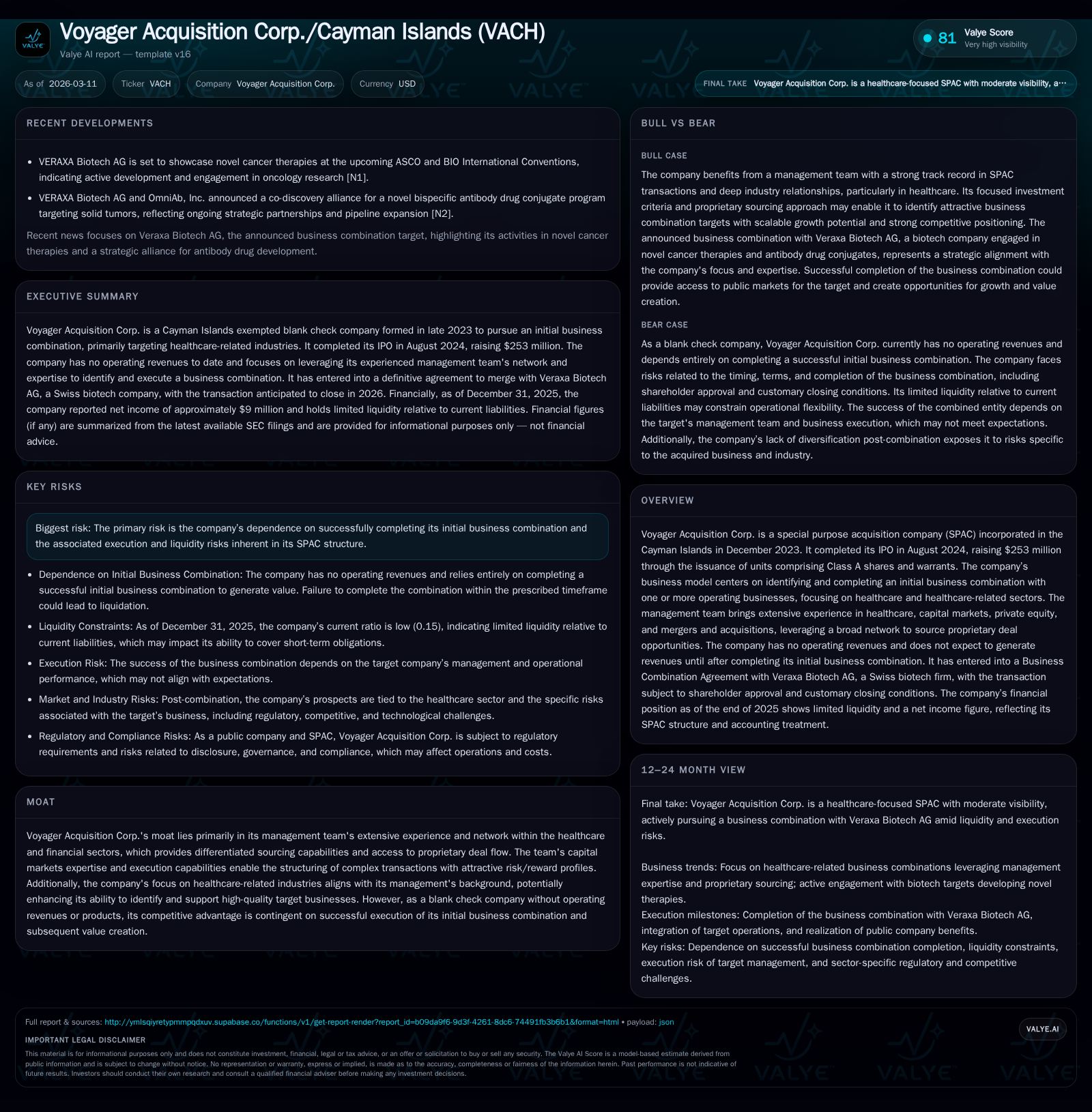

Voyager Acquisition Corp. launched in late 2023 as a SPAC with a $253 million IPO targeting healthcare companies. To date, it has no operating revenue or business of its own and stands at a crossroads pending completion of its initial business combination, presently agreed with Swiss biotech Veraxa Biotech AG. Its management team’s experience across healthcare and capital markets forms the basis of its competitive moat, centered on deal sourcing and execution capabilities. Financially, Voyager has reported losses consistent with a pre-combination SPAC and holds minimal working capital outside its trust account. Future growth depends primarily on successful deal closure and integration of the target, while liquidity is safeguarded but subject to typical redemption rights. Investors should monitor the timing, terms, and shareholder approvals of the business combination as key milestones.

Company Overview

Voyager Acquisition Corp., incorporated under Cayman Islands law in December 2023, functions as a special purpose acquisition company (SPAC) with an explicit focus on healthcare and allied sectors [S1]. It completed its initial public offering (IPO) in August 2024, issuing 25.3 million units at $10 each to raise $253 million gross proceeds [S1], [F1]. Each unit includes one Class A ordinary share and half of a warrant exercisable for an additional share at $11.50.

Historical Performance and Operational Status

As a newly minted blank check company, Voyager maintains a holding structure without any operating business or revenue stream pre-merger [S1]. The fiscal year ending December 31, 2025, manifested typical SPAC financial characteristics: operating loss expanded from approximately $0.7 million (FY2024) to $1.78 million (FY2025), stemming primarily from increased legal, administrative, and due diligence expenses linked to evaluating its target acquisition [F1]. Despite these losses, net income was positive at around $9.0 million in FY2025 versus $4.14 million prior year due principally to non-operating gains such as interest income or changes in equity instruments valuation [F1].

Operating cash flow remains negative but improved modestly from -$703k (FY2024) to -$486k (FY2025), underpinning ongoing investment in transaction preparation without generating operating profits [F1]. Equity reported at ($13.15) million negative reflects accounting treatment for warrants and equity derivative liabilities common among SPAC structures [F1]. The current ratio stands low at approximately 0.15 (current assets over liabilities), reflective of minimal circulating working capital aside from cash in trust [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 9 | -486182 | -1785259 | +117.1% |

| 2024 | 4 | -703468 | -702959 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -68.4 |

| 2024 | -36.4 |

Source: SEC companyfacts cache [F1].

Voyager's financials confirm zero revenue status consistent with pre-business combination stage.

Management Expertise and Competitive Moat

Voyager’s value proposition centers on its experienced management team whose backgrounds span healthcare operations, private equity investing, capital markets execution, and M&A transactions [S1], [S8], [S28]. This confers advantages including:

- Proprietary Deal Sourcing: Extensive industry relationships within life sciences and healthcare sectors provide access to exclusive opportunities often unavailable through broad auction processes.

- Capital Markets Navigation: Expertise enables structuring transactions with tailored financing—equity issuance, debt financing or hybrids—to optimize cost of capital post-combination.

Beyond deal closing, Voyager supports post-merger operational growth through strategic partnerships formation, brand development alongside influential industry figures, and talent recruitment for boards and executive teams—key for scaling within complex healthcare ecosystems [S8].

Focused Investment Criteria

Target businesses are sought within an enterprise value range of approximately $160 million to $2 billion; characterized by scalable growth potential; defensible competitive positioning via intellectual property or technology advantages; and led by committed professional management teams aligned with investor interests [S4], [S5], [S18]. Additionally, targets should be positioned to leverage benefits inherent in public ownership including broad capital market access [S4].

Current Liquidity and Capital Structure

IPO proceeds largely reside in a trust account designated for investor redemptions upon shareholder approval voting related to the business combination [S6], [S12], [S14]. Public shareholders can redeem shares at roughly $10.05 per unit plus accrued interest—providing principal protection against adverse outcomes such as failure to complete a merger within the prescribed timeline [S14], [S24].

Sponsor indemnification agreements provide additional protection against creditor claims impacting trust assets though residual risks persist if indemnification cannot be fully enforced [S24]. Monthly operational costs are modest (~$10k/month paid to Sponsor affiliate), reflecting efficient overhead control pre-combination [S26].

No external debt financing is currently secured or planned before the initial business combination completion; however Voyager retains flexibility to use cash raised or raise debt/equity securities for acquisition financing as needed [S7]. The Business Combination Agreement with Veraxa Biotech AG was amended in February 2026 increasing implied merger consideration to approximately $1.35 billion—consistent with Voyager’s investment range—and extending the deadline through August 7, 2026 [S13].

Growth Outlook: Dependent on Initial Business Combination Execution

Future growth depends entirely on consummating the initial business combination successfully within required timeframes followed by realizing synergy gains from integration efforts. While details remain limited publicly regarding the target Veraxa Biotech AG, the company aligns with Voyager’s healthcare focus.

Key growth drivers include:

- Accelerated scaling via strategic partnerships catalyzed by Voyager’s network.

- Accessing broader U.S. and global equity/debt capital markets post-merger facilitating expansion investments.

- Operational efficiency improvements driven by public company disciplines.

Constraints include:

- Risks of delay or failure completing the initial business combination triggering potential liquidation.

- Redemption demands that may reduce available capital for growth initiatives.

- Single-industry concentration risks post-merger affecting diversification.

Monitoring merger progress including shareholder vote outcomes and regulatory approvals remains critical.

Returns and Capital Allocation Policy

As a pre-business combination SPAC without operating earnings generation so far:[F1]

- Approximate ROE calculated as net income divided by negative equity yields around -68%, reflecting warrant accounting rather than operational performance.

- Negative operating cash flow persists consistent with lifecycle phase.

- No dividends or share repurchase programs exist; all capital allocation focuses on structuring the initial business combination while preserving public shareholder liquidity rights via redemption provisions embedded contractually for investor protection [S6], [S14], [S19].

Conclusion & Monitoring Points

Voyager Acquisition typifies a healthcare-focused SPAC positioned at a pivotal stage: holding substantial IPO proceeds secured in trust accounts protecting investors against incomplete deals; bearing typical pre-combination financial profiles; reliant on management expertise for deal sourcing and execution.

Key elements warranting close observation include:

- Timely closing of the amended Business Combination Agreement before August 7th deadline.

- Shareholder approval process dynamics including redemption elections impacting net acquisition proceeds.

- Post-merger integration strategies influencing operational scalability within targeted healthcare niches.

This analysis is based solely on publicly available filings as of March 11, 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments