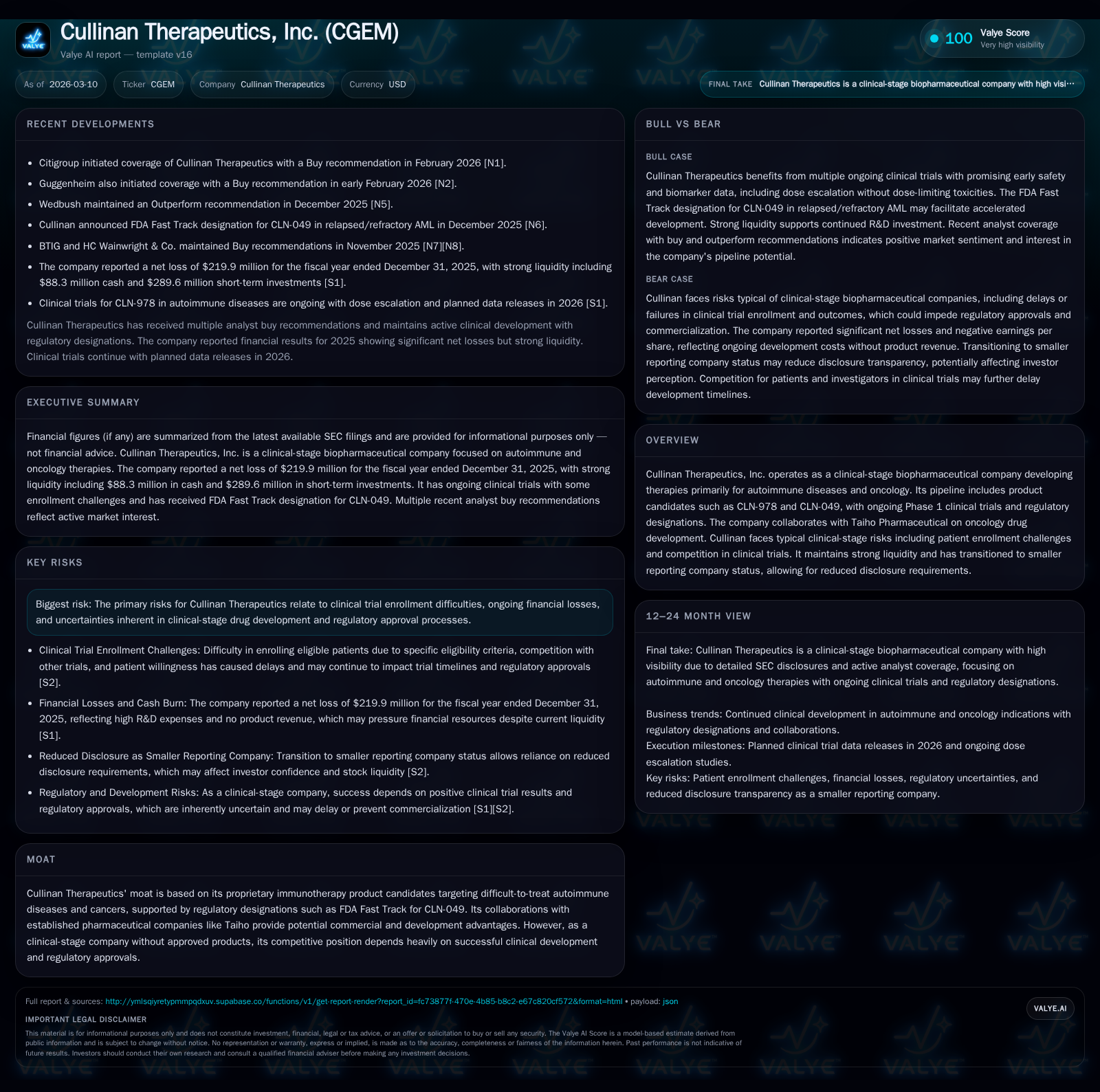

Cullinan Therapeutics’ Clinical Pipeline and Capital Discipline Shape Its Future Outlook

Cullinan Therapeutics advances novel immunotherapies against autoimmune diseases and oncology within a framework of disciplined capital management amid trial enrollment risks.

Cullinan Therapeutics remains a clinical-stage biopharmaceutical company focused on immunotherapy candidates CLN-978 and CLN-049 targeting difficult autoimmune conditions and hematologic malignancies. The firm faces typical developmental headwinds, including patient enrollment bottlenecks and clinical risks, offset by regulatory incentives like FDA Fast Track designation for CLN-049 and a strategic oncology partnership with Taiho Pharmaceutical. While operating losses have deepened year-over-year due to sustained R&D investment, the company maintains strong liquidity with a current ratio over 10, enabling a runway into 2029 under its current plan. Market interest has grown following recent positive analyst buy initiations, though milestones hinge on upcoming clinical readouts and enrollment progress. Cullinan’s financial discipline prioritizes cash preservation without dividends or buybacks, focusing capital allocation toward pipeline advancement.

Historical Growth Trajectory: Operating Losses Amid Advancing Clinical Programs

Cullinan Therapeutics has experienced increasing operating losses over recent years driven by heightened investment in its clinical-stage programs. Operating income declined approximately 22.7% year-over-year from -$196.9 million in FY2024 to -$241.6 million in FY2025 [F1]. Net losses similarly widened from -$167.4 million to -$219.9 million, worsening by about 31.4% [F1]. These figures reflect significant research and development expenditures as Cullinan focuses resources on advancing early-phase studies.

Operating cash flow remains negative at roughly -$175.8 million most recently, consistent with ongoing cash consumption aligned with trial progression [F1]. Capital expenditures are minimal relative to overall spend, consistent with the asset-light nature typical of clinical-stage biotech companies.

Despite persistent losses, Cullinan's liquidity profile is strong: as of December 31, 2025, current assets totaled approximately $386.8 million versus $37.7 million in current liabilities, yielding a robust current ratio of about 10.25 [F1]. This positions the company well to fund operations through multiple years without immediate need for capital raises.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -220 | -176 | -242 | 49000 | -31.4% |

| 2024 | -167 | -145 | -197 | 0 | -9.3% |

| 2023 | -153 | -134 | -191 | 208000 | -237.7% |

| 2022 | 111 | -127 | 145 | 1133000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -176 | -53.8 |

| 2024 | -145 | -28.4 |

| 2023 | -134 | -33.8 |

| 2022 | -128 | 20.8 |

Source: SEC companyfacts cache [F1].

The data illustrate Cullinan's transition from positive operating income in 2022 to increasing operating losses reflecting clinical scale-up.

Clinical Pipeline Focus: Advances and Challenges in Autoimmune and Oncology Trials

Cullinan’s pipeline centers on two main immunotherapy candidates: CLN-978 targeting autoimmune diseases including rheumatoid arthritis (RA), systemic lupus erythematosus (SLE), and Sjögren’s syndrome; and CLN-049 aimed at oncologic indications such as relapsed/refractory acute myeloid leukemia (AML) [S20][S25]. Both remain in Phase 1 development.

CLN-049 has received FDA Fast Track designation granted in late 2025 following compelling monotherapy activity data presented at the ASH Annual Meeting demonstrating promising response rates even among heavily pretreated AML patients including those with high-risk TP53 mutations [S26][S29]. Dose escalation continues with expansion cohorts planned throughout 2026.

Autoimmune trials for CLN-978 encounter enrollment challenges typical of this therapeutic area [S9][S10]. For instance, stringent eligibility criteria particularly concerning disease severity have contributed to higher-than-anticipated screening failures causing delays in the systemic lupus erythematosus cohort [S9]. Such hurdles reflect broader sector difficulties recruiting patients willing to accept risks related to first-in-human biologics amid available therapies.

Factors constraining enrollment include patient proximity to trial sites; limited availability of specialized investigators; requirements for genetic tumor sequencing for target confirmation in oncology; and competition among contemporaneous trials exploring novel immunomodulatory approaches [S10]. These impact statistical power calculations essential for pivotal study success.

Partnerships as Growth Engines: The Taiho Collaboration and Regulatory Milestones

Cullinan's collaboration with Taiho Pharmaceutical anchors its oncology strategy via shared development risks related to zipalertinib — a targeted agent distinct yet complementary to CLN-049 — with Taiho initiating rolling NDA submissions aiming accelerated approval [S18]. This partnership exemplifies risk-sharing arrangements common among clinical-stage biotech firms wherein milestone payments and profit sharing provide validation alongside resource leverage.

Milestone payments could total up to $130 million upon U.S regulatory approvals plus a fifty-fifty split of pretax profits from commercialization [S18]. The Fast Track status for CLN-049 may facilitate accelerated regulatory interactions including rolling submissions contingent on successful dose selection and enrollment completion [S26].

Investor Expectations: Analyst Buy Ratings and Upcoming Clinical Catalysts

Market commentary includes coverage initiations by Guggenheim [N2] and Citigroup [N1], both issuing buy recommendations emphasizing confidence in Cullinan’s differentiated immunotherapy portfolio supported by capital discipline ensuring runway visibility.

Key upcoming milestones include initial safety and biomarker readouts from single dose escalation parts of the Phase 1 OUTRACE trials for CLN-978 across RA and SLE cohorts expected Q2–Q3 2026 [S20]. Dose expansion updates on CLN-049 including recommended Phase 2 dosing determinations are anticipated later in Q3/Q4 along with initiation of combination studies in frontline AML [S25].

These catalysts represent typical value drivers for early-stage biotechs reliant on advancing clinical signals rather than commercial revenues.

Capital Allocation Profile: Robust Liquidity With No Dividends or Buybacks

Cullinan does not currently pay dividends nor conduct share repurchases; instead capital is allocated towards sustaining clinical programs [S11][S12][S13]. Cash equivalents stood near $88.3 million at fiscal year-end within total current assets exceeding $386 million—providing runway through at least end of calendar year 2028 based on existing operational plans disclosed during earnings calls [S15][F1].

This conservative capital deployment approach aligns with maintaining operational longevity amid timing volatility inherent to clinical development rather than returning capital to shareholders.

Financial Health: Cash Burn Rate & Return on Equity

The approximate return on equity (ROE) is about negative 53.8%, calculated by dividing net loss (-$219.9 million) by total shareholders’ equity ($408.7 million) as of December 31, 2025 [F1]. This level is consistent with expectations for a pre-revenue biotech investing heavily in R&D.

Free cash flow approximates negative $175.8 million—operating cash flow less capex—matching burn rates cited internally supporting multi-year funding sufficiency absent unplanned acceleration or setbacks [F1]. Equity has decreased somewhat relative to prior years but remains above $400 million supporting balance sheet stability.

There is no indication of outstanding borrowings or recent financing events based on filings disclosing neither new debt nor equity raises during latest reporting periods [S23][S24].

Strategic Risks: Enrollment Challenges & Reporting Changes Following Smaller Reporting Status

Management highlights risks related to patient enrollment difficulties that may delay trial completion or regulatory approvals if sample sizes do not meet required statistical thresholds set by FDA or global agencies [S7][S9][S10]. Competition for qualified patients is intense as multiple trials vie within narrow populations especially when novel mechanisms challenge physician/patient acceptance compared to established treatments.

Additionally, effective December 31, 2025 Cullinan transitioned to smaller reporting company status allowing reduced disclosure requirements under SEC rules which may impact investor perceptions regarding transparency and governance rigor [S2][S7]. This change could affect stock liquidity or attractiveness despite compliance cost savings.

These structural challenges are compounded by investigator site competition favoring larger sponsors or more advanced pipelines potentially limiting recruitment velocity critical for maintaining trial momentum as acknowledged internally [S8][S9].

This analysis integrates audited financial metrics alongside operational disclosures portraying Cullinan Therapeutics as a well-capitalized clinical-stage biotech advancing promising immuno-oncology assets supported by strategic partnerships amid inherent enrollment challenges shaping developmental risk profiles across its lead product candidates.

Disclaimer: This report is prepared solely for informational purposes without providing any investment advice or recommendations concerning securities referenced herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments