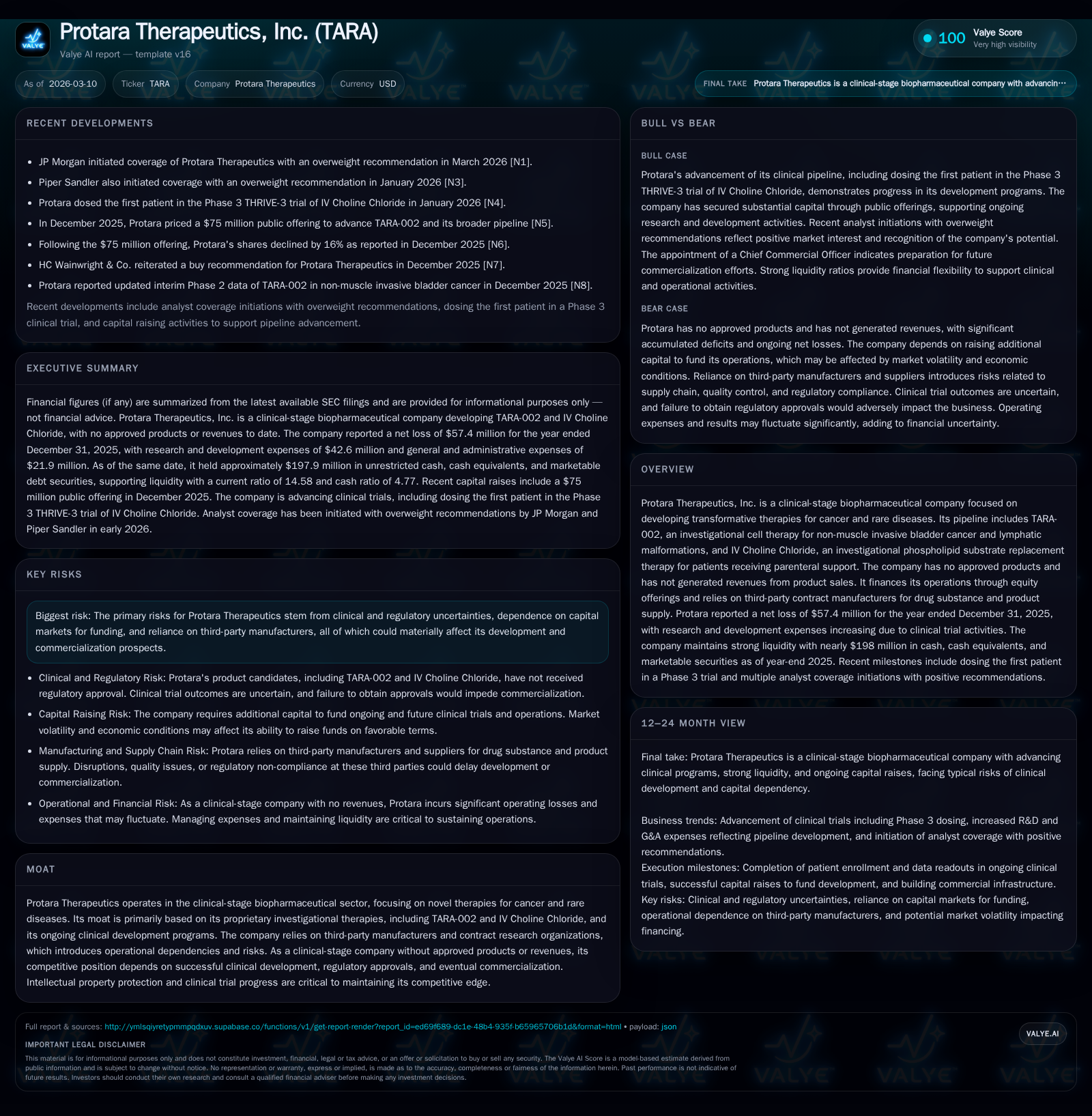

Protara Therapeutics Builds Clinical Momentum while Managing Operating Deficits

Protara pursues clinical advances in cancer and rare diseases while navigating the inherent financial demands of early-stage drug development.

Protara Therapeutics remains a pre-revenue, clinical-stage biopharmaceutical company focused on innovative therapies in oncology and rare disease. Despite persistent operating losses driven by escalating R&D expenses, the company has bolstered its cash reserves through equity financings, maintaining healthy liquidity to fund ongoing trials. Key pipeline assets TARA-002 for non-muscle invasive bladder cancer and IV Choline Chloride for parenteral nutrition support are advancing through critical clinical stages, with expectations aligned to regulatory milestones yet unquantified by formal guidance. Risks typical to clinical-stage drugmakers—regulatory uncertainty, reliance on third-party manufacturers, and capital market dependence—persist as fundamental considerations.

Reviewing Historical Financials: Growth Metrics and Expense Drivers

Protara Therapeutics operates without any approved products or commercial sales revenue to date. Revenues have remained static at approximately $2.95 million annually since FY2014, a figure primarily comprised of non-product-related income [F1]. The company’s operating losses have fluctuated considerably but trended upward again in FY2025, reaching a deficit of -$64.5 million, reversing a moderate improvement seen between FY2023 and FY2024 [F1]. This loss trajectory corresponds directly with rising research and development (R&D) expenses that multiplied by over one-third in the most recent year due to intensified clinical trial activity [S13][S25]. General and administrative costs also grew but at a lower rate.

Operating cash flow (CFO) presents a stark picture of expanding negative free cash flow generation, deteriorating from -$26.5 million in FY2022 to a substantial -$56.4 million in FY2025 [F1]. This indicates increasing cash consumption required to fund operations before any commercial product launch.

However, working capital stands out as an exceptional strength; with current assets of roughly $159.5 million against current liabilities of about $10.9 million at year-end 2025 (current ratio 14.58), Protara carries robust short-term liquidity buffers [F1], [S4]. Capital expenditures remain low ($94 thousand in FY2025), consistent with the asset-light model typical of many biopharma companies relying heavily on outsourced manufacturing and clinical services.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -57 | -56 | -65 | 94000 | -28.8% |

| 2024 | -45 | -36 | -49 | 63000 | -10.3% |

| 2023 | -40 | -38 | -44 | 45000 | +38.7% |

| 2022 | -66 | -26 | -67 | 120000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -56 | -29.2 | |

| 2024 | -36 | -26.7 | |

| 2023 | 91000 | -38 | -59.2 |

| 2022 | 90000 | -27 | -64.6 |

Source: SEC companyfacts cache [F1].

Source: [F1]

The company’s accumulated deficit stood at approximately $302.4 million as of Dec 31, 2025 [S1]. This underscores the capital-intensive nature of Protara's operation without foreseeable near-term revenues.

Clinical Pipeline: Current Progress and Strategic R&D Investments

Protara is focused chiefly on two investigational therapies: TARA-002 and IV Choline Chloride [S1], [N1]. TARA-002 is an autologous cell therapy under clinical evaluation for non-muscle invasive bladder cancer (NMIBC) and lymphatic malformations (LMs), representing biologic approaches tailored toward difficult-to-treat conditions marked by high unmet medical needs [S1], [N1]. IV Choline Chloride addresses choline deficiency among patients receiving parenteral nutrition—a niche indication without existing sterile injectables approved—indicating potentially unique market positioning backed by patents extending through 2041 [S12].

Clinical trial activity has intensified notably since early 2024. Research and development expenses attributable directly to TARA-002 rose substantially—to $18.4 million in NMIBC alone—and IV Choline Chloride costs nearly doubled year-over-year to $8.5 million in 2025 [S25]. These figures include expenses for CRO engagement as well as manufacturing material supplied via CDMOs—a reliance that highlights supply chain dependencies common across small biotechs [S13], [S25].

JP Morgan initiated coverage with an Overweight rating signaling confidence in Protara’s scientific rationale and ongoing registrational studies but acknowledged that clear forward guidance or timelines remain limited at this stage [N1], [S3]. The cautious optimism reflects standard biopharma asymmetries where regulatory approval requires multi-phase validation over extended periods.

Capital Structure Dynamics and Liquidity Position

Funding operations during this prolonged clinical period depends heavily on external capital markets given the absence of product-related cash inflows. Protara’s last two years saw significant equity raises: approximately $102.8 million gross proceeds from December 2024 public offerings accompanied by an additional $86.3 million raised in December 2025 public equity sales under shelf registration filings [S23]. Combined with private placements earlier in 2024 yielding ~$45 million gross proceeds plus warrant exercises generating incremental capital (> $3 million), this series of financings has fortified the company's balance sheet considerably [S23].[F1]

As of December 31, 2025, Protara’s unrestricted cash plus equivalents totaled approximately $49.7 million; however, adding marketable debt securities lifts total liquid assets close to $198 million—a considerable stash enabling operational continuity well into anticipated registrational milestones over the next year [F1], [S9],[S27].

Notably absent from disclosures is meaningful long-term debt exposure; this equity-centric capital structure reduces financial leverage risk but entails dilution impacts inherent to growth-phase biotech operating models reliant on repeated financing rounds [S4], [S20], [S27].

Risk Factors and Operational Dependencies

Protara openly details numerous risks typical for clinical-stage biopharmas but augmented by specific operational nuances revealed through its filings:

- Clinical risks dominate given all investigational therapies have yet to complete pivotal stages; potential trial delays or failures could materially impact viability [S1], [S6], [S7].

- Regulatory scrutiny incorporates FDA oversight's complexities including strict advertising controls limiting off-label promotion flexibility post-approval as per U.S law enforcement frameworks ([S6],[S7],[S10]) and ongoing cGMP compliance required for manufacturing partners.[S18]

- Supply chain resilience is challenged by reliance on third-party contract manufacturers (CDMOs) and CROs for production scale-up and trial execution — disruptions could hamper timelines substantially ([S13],[S20]).

- Intellectual property litigation risk arises from employees’ prior industry relationships and patent landscapes surrounding TARA’s novel compositions ([S5],[S16],[S17]).

- Compliance with evolving data privacy laws adds operational complexity given sensitive patient data handling during trials ([S5]).

- Product liability exposure escalates particularly if clinical safety signals emerge or commercial launches proceed improperly insured ([S26]).

- Political-economic uncertainties including U.S drug pricing reforms (e.g., Medicare reimbursement cuts) may indirectly affect eventual commercial strategy even pre-launch ([S11],[S21]).

Collectively these risks underscore challenges faced managing multiple fronts simultaneously—from developing complex biologics safely to navigating regulatory frameworks underpinned by heavy legal enforcement.

Market Expectations, Catalysts, and What To Watch

While Protara refrains from formal milestone projections beyond routine disclosure updates ([N1],[S3]), key upcoming value inflection points typically include preliminary registrational trial readouts for TARA-002 in NMIBC and LM indications as well as continued enrollment progress for IV Choline Chloride studies.

JP Morgan’s bullish stance hinges on successful proof-of-concept generation translating into late-stage advancement eligibility ([N1]), but actual regulatory submission timings remain contingent upon trial outcomes not yet finalized publicly.

Investors should monitor:

- Announcements around Phase II/III data releases,

- Any expedited or breakthrough therapy designation grants,

- Potential partnership agreements leveraging Protara’s assets,

- Additional equity funding rounds which may dilute further or indicate pipeline delivery urgency.

These elements will shape sentiment ahead of commercialization feasibility assessments.

Assessing Capital Allocation Efficiency and Returns

Financial returns currently reflect typical early-stage biopharma investment patterns: net losses are sustained (-$57.4 million in FY2025), producing an approximate ROE around -29.2% based on net income relative to shareholder equity of about $196.4 million at year-end 2025 [F1]. Losses widen significantly relative to prior years following stepped-up R&D investment—consistent with deliberate platform building rather than premature scaling.

Capital expenditure levels remain muted (<$100k annually), signaling Protara focuses predominantly on externalized capex-light R&D activities rather than internal infrastructure expansion which would elevate fixed costs or asset bases materially [F1],[S13],[S28].

Modest share repurchase activity noted historically dwarfs ongoing investor dilution evidenced via frequent public offerings emphasizing a patient-oriented growth strategy prioritizing pipeline advancement over immediate shareholder distributions or buybacks ([F1]).

In sum, capital deployment aligns tightly with advancing clinical programs while preserving liquidity buffers sufficient to weather the inherently uncertain drug development lifecycle phases.

This analysis is based solely on information publicly disclosed through SEC filings as of March 10th, 2026 and referenced news sources without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments