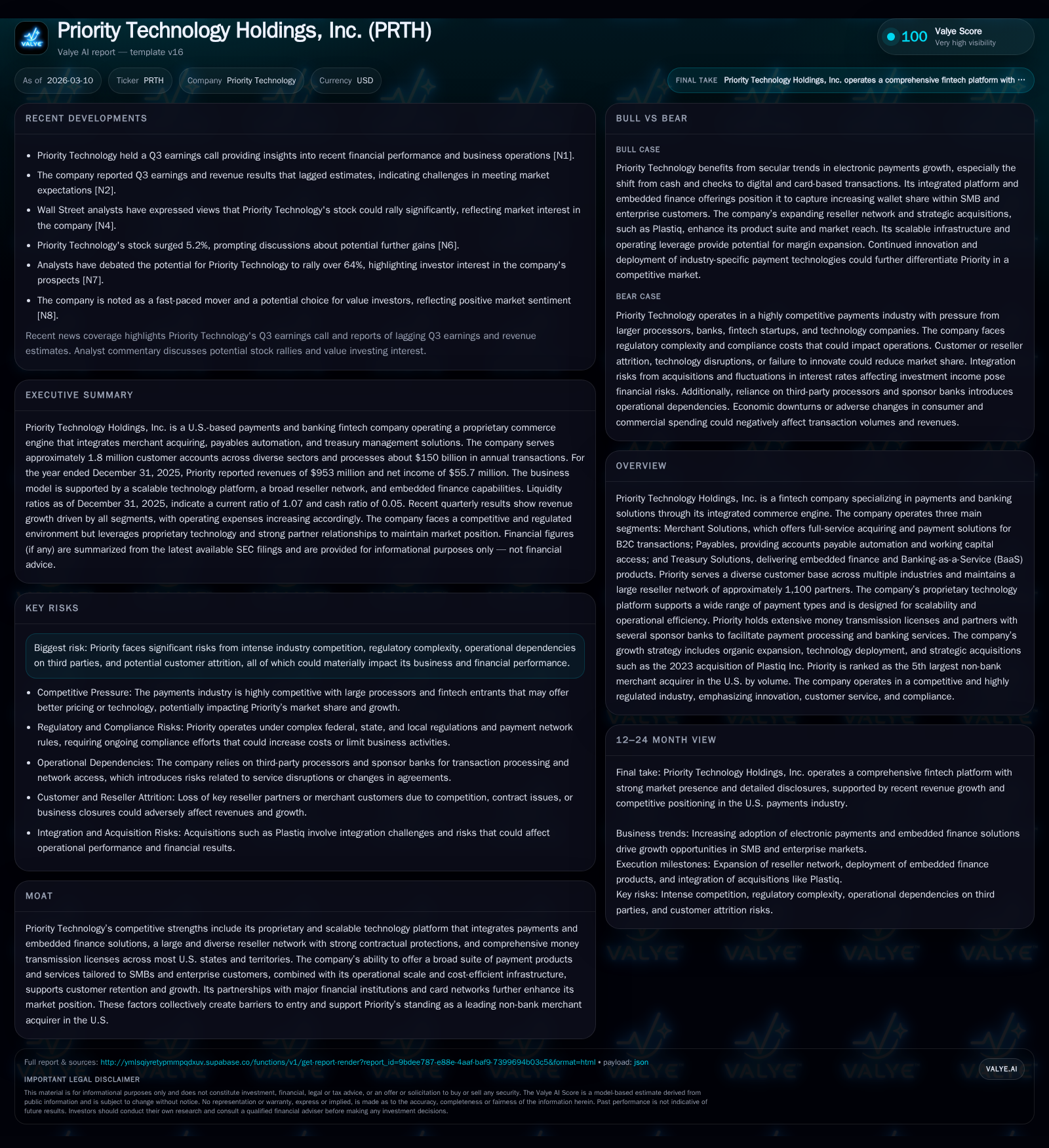

Priority Technology Holdings: Scaling Integrated Commerce Amid Growing Fintech Demand

Priority Technology leverages a proprietary commerce engine to integrate payments and embedded finance, fueling growth across merchant solutions, payables automation, and treasury services.

Priority Technology Holdings has evolved from a founder-led startup to the fifth largest U.S. non-bank merchant acquirer by volume, underpinned by its scalable, proprietary technology platform and expansive reseller network. Its three core segments—Merchant Solutions, Payables, and Treasury Solutions—serve over 1.8 million customers while processing approximately $150 billion annually. Despite improving operating income and strong cash flow growth in 2025, the company operates with negative equity and a levered capital structure amid regulatory complexities. Future growth depends on expanding embedded finance offerings and reseller penetration while navigating competitive and regulatory headwinds.

Evolution of Priority’s Growth and Operational Drivers

Priority Technology Holdings has developed substantially since its founding in 2005 as a founder-financed fintech startup focused on bridging software and payments through an institutional-caliber commerce engine [S1][S24]. As of early 2026 filings, it ranks as the fifth largest non-bank merchant acquirer in the U.S., according to the March 2025 Nilson Report [S24]. This growth reflects strategic investments in a fully integrated proprietary technology platform supporting multiple payment types—including card acquiring/issuing, ACH, wire transfers—and embedded finance capabilities.

Serving roughly 1.8 million customer accounts that process about $150 billion annually in transactions while administering approximately $1.7 billion in account balances [S1][S24], Priority’s business model centers on accelerating cash flow cycles for SMBs and enterprises via integrated commerce solutions. Operating income expanded from $56.2 million in FY2022 to $141.2 million in FY2025—a compounded increase exceeding 150% over three years—with year-over-year growth moderating to 5.9% most recently [F1].

Operating cash flow demonstrated enhanced liquidity generation capacity with a 16.8% increase year-over-year reaching approximately $100 million in FY2025 [F1], underpinning both organic growth initiatives and capital investments.

Segment Dynamics: Merchant Solutions, Payables, and Treasury Solutions

Priority’s revenue streams are structured into three interrelated segments supporting end-to-end financial workflows:

Merchant Solutions: Leading full-service payment processing for B2C transactions at points of sale and online channels. This segment acts as a non-bank merchant acquirer offering card acceptance alongside value-added services via cloud-based platforms such as MX Connect and MX Merchant [S11][S19][S20]. Sales channels comprise independent sales organizations (ISOs), financial institutions (FIs), independent software vendors (ISVs), and value-added resellers (VARs).

Payables: Focused on accounts payable automation tools coupled with working capital acceleration products including partnerships like CPX and Plastiq with major card networks [S11][S17]. It targets commercial payments markets that lag consumer electronic payments adoption by streamlining buyer-supplier transactions.

Treasury Solutions: Encompasses embedded finance and Banking-as-a-Service (BaaS) offerings enabling non-financial businesses to integrate banking functions seamlessly within their applications [S11][S17]. Extensive money transmission licenses across forty-six U.S. states plus D.C. provide operational breadth.

This tripartite approach enables cross-segment synergies powered by Priority’s scalable commerce engine that consolidates all money movement activities within one integrated technology stack [S16][S24].

Financial Overview: Improving Profitability and Cash Flows in FY2025

The table below summarizes Priority Technology’s key financial metrics for fiscal years 2022 through 2025 per latest SEC data [F1]:

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 43830 | |||

| 2025 | 100 | 141 | 25 |

| 2024 | 86 | 133 | 22 |

| 2023 | 81 | 82 | 21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 43830 | ||

| 2025 | 0 | 75 |

| 2024 | 24 | 64 |

| 2023 | 25 | 60 |

Source: SEC companyfacts cache [F1].

Operating income shows continued margin improvement while net income appears flat based on available data, possibly reflecting expense or impairment factors not detailed explicitly [F1]. Capital expenditures rose nearly 15% year-over-year in FY2025 aligned with ongoing investments into technology enhancements supporting organic growth strategies [F1].

Despite generating substantial free cash flow estimated at approximately $75 million (operating cash flow minus capex), Priority reported negative book equity of about -$100 million as of FY2025 likely attributable to cumulative historical losses or balance sheet adjustments without further granularity provided [F1].

Capital Structure and Allocation Strategies

As of late 2025, Priority carries significant indebtedness exceeding $1 billion primarily under an amended credit agreement maturing July 2032 plus a Residual Finance Credit Facility [S4][S6][S10]. These debt instruments impose restrictive covenants limiting dividend payments (none declared or paid during FY2025 compared to prior years), asset disposals, new indebtedness incurrence, mergers/consolidations, and other corporate activities [S4][S6][S8][S9]. The revolving credit facility matures July 2030.

A critical covenant—the Total Net Leverage Ratio—limits net debt relative to adjusted EBITDA starting at approximately 6.9x through early-mid-2026 before tightening to about 6.4x thereafter; Priority was compliant as of Q3-2025 filings [S4][S8]. Capital allocation reflects caution under these constraints with modest share repurchases (~$1.25 million in FY2023) versus larger dividend distributions prior to ceasing dividends last year [F1][S9].

Liquidity is supported by cash reserves around $77 million at year-end FY2025 plus availability under revolving credit facilities sufficient for near-term working capital needs [F1][S18].

Governance of Risk and Regulatory Compliance

Risk management remains vital given the sensitive nature of payment data handled—including credit/debit card details and bank account information—and reliance on third-party vendors increasing cybersecurity exposure such as ransomware or denial-of-service attacks [S1][S12][S22]. Although cyber insurance coverage exists, incidents can be costly reputationally and financially.

Complex multi-state regulatory compliance involves money transmission licensing across forty-six states plus D.C., along with adherence to PCI DSS standards safeguarding cardholder data security [S12][S15][S22]. These frameworks require continuous investment in controls.

Notably, Priority settled litigation related to California Invasion of Privacy Act claims concerning call recording practices for $19.5 million finalized in May 2025; this settlement impacted prior periods but is not expected to materially affect future results [S12][S22].

Additional risks arise from evolving regulatory scrutiny on bank-non-bank partnerships essential for embedded finance offerings that integrate banking features into non-bank platforms; failure here could jeopardize critical sponsoring bank relationships needed for service delivery [S22][S23].

Outlook: Market Opportunities and Headwinds

Management underscores significant growth potential from expanding embedded finance services within underserved SMBs alongside enterprise clients seeking integrated treasury management within core business applications [S2]. Expansion through the existing reseller network (~1,100 partners) broadens distribution reach into verticals complemented by selective acquisitions focused on recurring revenue streams with scalable operations.

However, competitive pressures intensify from banks leveraging scale advantages alongside fintech innovators rapidly deploying APIs beyond legacy systems used by larger acquirers [S20][S23]. Regulatory changes or shifts in card association fees could pressure margins requiring vigilant price management.

Monitoring revenue mix evolution per segment will be crucial as Treasury Solutions grows rapidly but demands continued investment while Merchant Solutions faces margin compression risks amid pricing competition.

Key Metrics to Monitor Moving Forward

Critical performance indicators include:

- Growth trajectory of transaction volumes beyond the current ~$150 billion annual run-rate,

- Stability or expansion of operating margins amid competitive pricing dynamics,

- Sustained free cash flow generation despite elevated capital expenditures,

- Compliance with credit facility covenants especially Total Net Leverage Ratio reflecting financial flexibility,

- Reseller network retention rates indicative of service quality,

- Contribution of embedded finance revenues relative to total sales illustrating integration success.

Continued executive emphasis on agile technology deployment combined with disciplined balance sheet management will shape Priority Technology’s enterprise value creation prospects.

This analysis is based exclusively on information publicly filed by Priority Technology Holdings through its March 10, 2026 Form 10-K filing along with supplementary SEC reports without speculative assumptions beyond documented disclosures or reasonable interpretative analysis within provided evidence parameters.[F1][S#]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments