SS Innovations International Doubles Revenue in 2025 but Faces Persistent Operating Losses

The company’s growth in the Indian surgical robotics market is tempered by ongoing net losses and liquidity challenges.

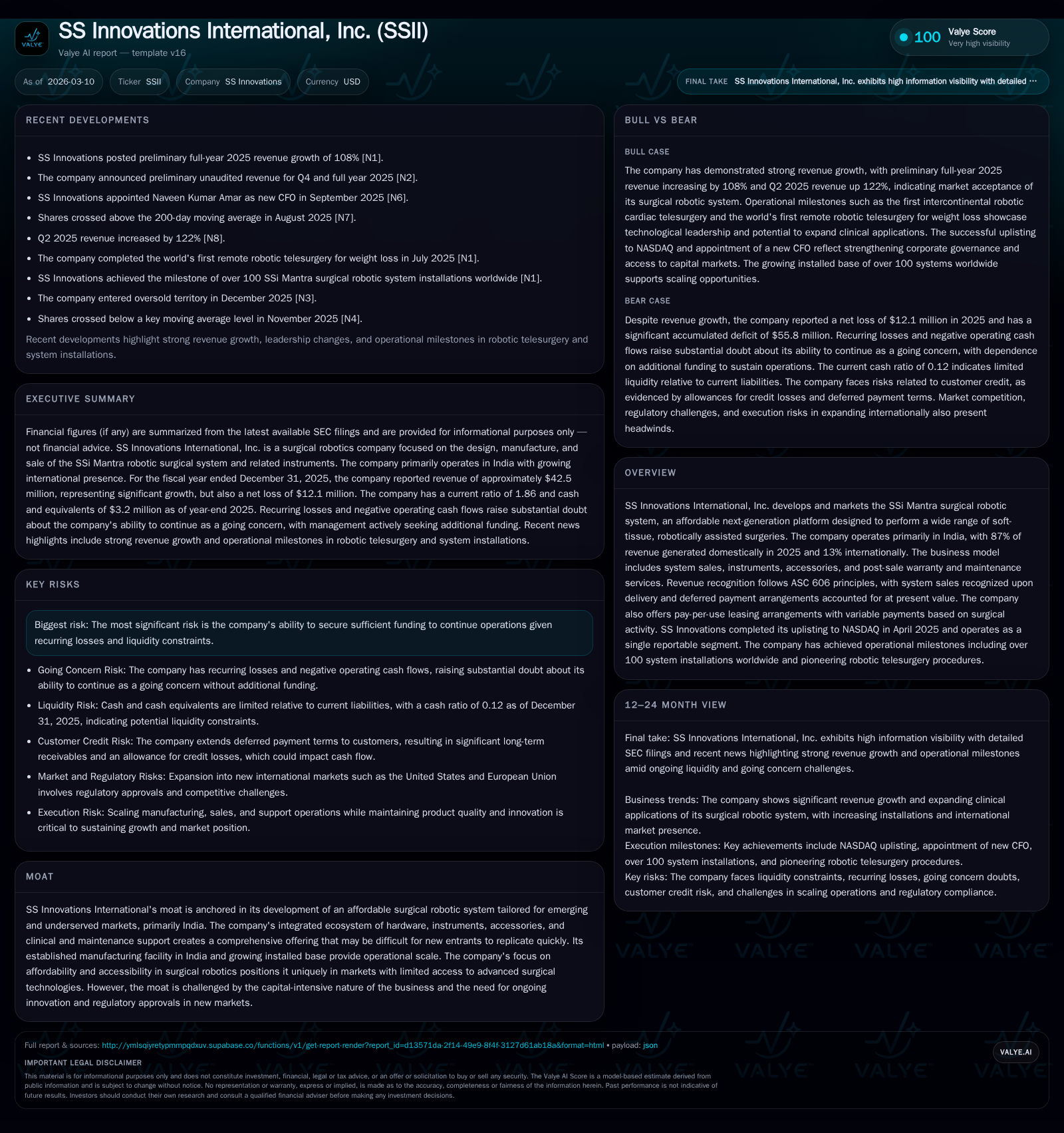

SS Innovations International, Inc. reported a revenue surge of over 100% in 2025, driven primarily by increased system sales of its affordable SSi Mantra surgical robotic platform in India. Despite the top-line expansion, SSII remains unprofitable with operating losses narrowing but still significant. The company generated negative operating cash flows exacerbated by elevated stock-based compensation and investment in manufacturing capacity. While management completed an equity raise in early 2026 to support working capital and market expansion, sustained funding remains critical given recurring losses and capital intensity.

Historical Performance

SS Innovations International's financial trajectory through 2023-2025 reveals the steep growth ambitions intersecting with operational scaling challenges typical of early stage medtech companies focused on robotic surgery innovation.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 42 | -12 | -19 | -8 | +105.7% | +36.7% |

| 2024 | 21 | -19 | -10 | -19 | +251.5% | +8.3% |

| 2023 | 6 | -21 | -15 | -20 | -843.4% | |

| 2022 | -2 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -22 | -31.7 |

| 2024 | -10 | -142.3 |

| 2023 | -18 | -105.9 |

| 2022 |

Source: SEC companyfacts cache [F1].

[Source: SSII Form 10-K FY2023-FY2025; F1]

Revenue more than doubled in each of the last two years driven predominantly by system sales which represented the bulk of total revenues ($38.4M out of $42.5M in 2025). This sharp top-line growth aligns with operational milestones such as surpassing installations of over 100 robotic systems—a key metric reflecting expanding clinical adoption within India’s underserved hospitals where affordability is critical [S1], [S19].

Gross margins improved substantially alongside scaled manufacturing output in its Gurugram-based facility [S6]. However, operating profitability remains elusive as investing in R&D ($3.7M in 2025), SG&A ($14.8M), and notably stock-based compensation expense ($8.1M) heavily burdens results [S6], [S19]. Despite this sizable spend profile driving losses ($8.2M operating loss), the net loss's moderation relative to prior years (-$12.1M net loss vs. -$19.2M in 2024) indicates gradual operating leverage [F1]. The roughly -32% ROE calculated signals capital intensity coupled with continuing focus on market penetration rather than profit generation currently.

Operating cash flows remain negative and deepened to nearly -$18.5M reflecting working capital demands from receivables—partly relating to deferred payment customer arrangements recognized at present value—and elevated capex spending mostly aimed at capacity enhancements [S23], [S26]. Capital expenditure increased materially (+453%) evidencing SSII’s efforts to strengthen production infrastructure and operational scale necessary for international market expansion plans [S13].

Future Growth Prospects

SS Innovations International’s primary growth driver remains its SSi Mantra platform which is positioned as an affordable alternative to legacy surgical robots facing high price points and complex ecosystems generally deployed in developed markets [S1]. The strategic emphasis on India (87% revenue concentration in 2025) speaks to leveraging underpenetrated segments where cost-effective technology can disrupt surgery standards [S18]. Emerging international markets contribute a growing minority share enhancing diversification albeit modest currently.

Growth levers include:

- Continued expansion of installed base increasing recurring revenue from instruments/accessories and extended warranty services.

- Scaling pay-per-use leasing arrangements tied to surgical activity introduces variable income stream likely beneficial for smaller hospitals or constrained capital environments [S8].

- R&D progress toward broader indication approvals could broaden procedure applicability beyond soft-tissue surgeries.

- Entry into developed market territories such as the US and EU is planned post regulatory clearances using proceeds from recent equity raises [S13].

Constraints mining growth are substantial capital requirements for product development cycles and regulatory compliance expansions needed internationally alongside competitive technological advancements from entrenched incumbents [N#],[S1]. The need for continual innovation while maintaining affordability represents a delicate balancing act.

Forecasts / Milestones / What To Watch

While explicit guidance is not provided in available disclosures [N#]/[S#], key developments warrant monitoring:

- Rate of new system installations quarterly/annually as a proxy for clinical adoption momentum.

- Expansion of service contracts and instrument sales that improve margin stability.

- Progress updating SSi Mantra capabilities or FDA/CE regulatory milestones enabling US/EU launches.

- Capital raising efforts beyond March 2026 private placement which injected approximately $18.6 million into the balance sheet targeting general corporate purposes including growth initiatives [S13].

- Ability to achieve positive operating cash flow as scale benefits mature.

Returns / Capital Allocation

SS Innovations has no dividend policy or history given ongoing losses and reinvestment needs [F1], [S14]. Equity issuance remains the dominant capital allocation tool used recently evidenced by an active share incentive program comprising stock options and restricted stock units valued at $8.1 million expense during year ending December 31, 2025 [S19]. Such equity incentives are essential talent retention & motivation levers in competitive tech-driven medical device sectors.

Balance sheet improvements were supported by gross proceeds near $18.6 million through private placements involving insiders including CEO Dr. Sudhir Srivastava and Vice Chairman Dr. Frederic Moll along with institutional participants such as Manipal Global Health Services [S13], illustrating shareholder alignment though dilution risks exist.

Liquidity metrics showed healthy current ratio (~1.86x) supported by cash & cash equivalents totaling approx $3.2 million plus restricted cash around $6.4 million combining fixed deposits held as collateral on overdraft banking facilities ensuring operational flexibility despite substantial short-term liabilities exceeding $26 million primarily from bank overdrafts and accounts payable [F1], [S20], [S4].

Operating free cash flow remained significantly negative (~ -$22 million calculated as CFO minus capex), underscoring ongoing investment phases before returning towards self-sustaining cash generation is feasible [F1].

Industry Context & Moat Analysis (Analyst Commentary)

SS Innovations International carves a niche focusing on affordability — a strategic moat uncommon among surgical robotics providers who typically target premium-margins via entrenched hospital relationships within developed economies. This low-cost yet comprehensive platform concept addressing emerging markets' accessibility gaps could unlock significant demand if executed effectively.

Nevertheless the pathway is laden with formidable barriers: costly regulatory approvals across geographies; continuous product refinement needed to compete technologically; establishing brand trust amongst surgeons; managing complex service & maintenance logistics; and sustaining sufficient funding amidst volatile liquidity conditions.

The company’s vertically integrated model — encompassing design through manufacturing plus post-sale clinical support — reinforces control over quality and pricing enabling differentiation particularly suited for price-sensitive markets like India where healthcare infrastructure varies widely regionally.

However reliance on insiders for financing along with perennial heavy losses highlight how nascent the model remains commercially despite technical achievements so far.

This analysis is based solely on publicly filed SEC disclosures through March 10th, 2026 [F1], supplemented by internal risk considerations highlighted therein without any endorsement or investment advice implied.

Disclaimer: This document serves informational purposes only and does not constitute financial advice or recommendations regarding SS Innovations International or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments