Hewlett Packard Enterprise’s Edge-to-Cloud Transition Faces Cost and Competitive Pressures

HPE leverages AI-native networking and hybrid cloud to capture growth, yet rising costs and integration challenges weigh on profitability.

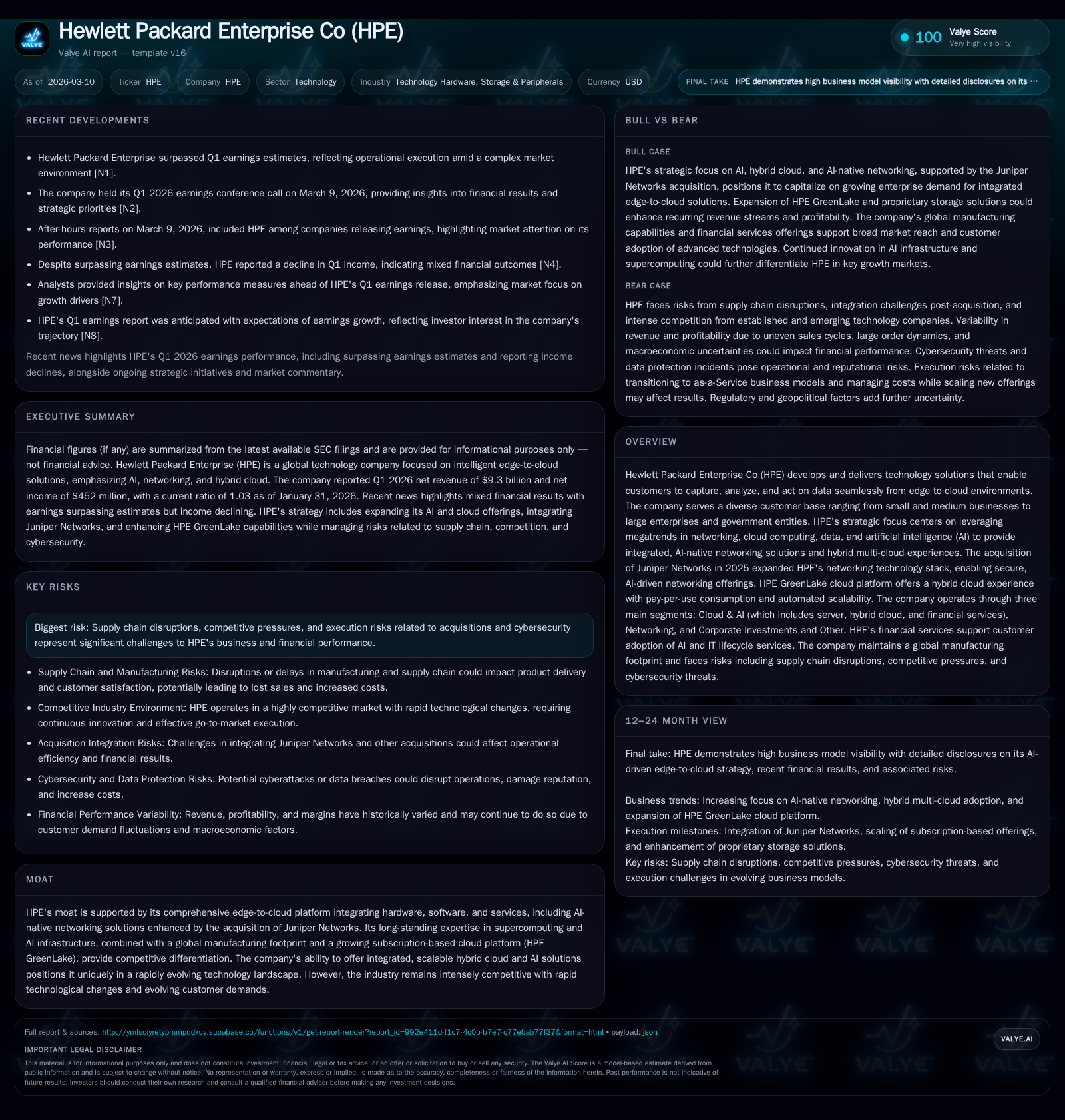

Hewlett Packard Enterprise Company (HPE) has grown its revenue steadily through strategic acquisitions like Juniper Networks and a pivot toward AI-driven, hybrid cloud solutions anchored by its GreenLake platform. Fiscal 2025 saw a 13.8% revenue increase, whereas operating income turned negative due primarily to merger-related costs and goodwill impairments. Going forward, the company aims to capitalize on megatrends in AI, edge computing, and multi-cloud adoption but faces risks including supply chain constraints, intense competition, and macroeconomic uncertainties. Its capital allocation continues to favor dividends with modest share repurchases amid significant investments in integration and innovation.

Overview

Hewlett Packard Enterprise Co (HPE) is a global technology leader focused on enabling customers to capture, analyze, and act on data seamlessly across edge-to-cloud environments. The company targets a wide enterprise base from SMBs to government entities with solutions spanning networking, cloud computing, high-performance servers optimized for AI workloads, and subscription-based hybrid cloud services under the GreenLake platform [S4][S14].

Over recent years, the company strategically repositioned itself around four megatrends: networking innovation especially powered by AI-native technology; hybrid multi-cloud adoption; exponential data growth at the edge; and artificial intelligence as a transformative workload. The acquisition of Juniper Networks in 2025 expanded HPE’s networking portfolio significantly, enhancing its ability to provide integrated secure networking fabric built specifically for AI-driven applications [S4][S10].

Historical Growth and Performance

Revenue showed consistent growth from $28.5B in FY2022 to $34.3B in FY2025—a compound annual rise supported by demand for server infrastructure with higher average unit pricing, plus synergies from Juniper Networks’ addition causing notable uplift in Networking revenue [F1][S13]. However, this growth came alongside challenging cost dynamics:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 34.3 | 0.1 | 2.9 | -0.4 | +13.8% | -97.8% |

| 2024 | 30.1 | 2.6 | 4.3 | 2.2 | +3.4% | +27.4% |

| 2023 | 29.1 | 2.0 | 4.4 | 2.1 | +2.2% | +133.3% |

| 2022 | 28.5 | 0.9 | 4.6 | 0.8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 684 | 202 | 627 |

| 2024 | 676 | 150 | 1974 |

| 2023 | 619 | 421 | 1600 |

| 2022 | 621 | 512 | 1471 |

Source: SEC companyfacts cache [F1].

Gross profit margins narrowed notably from prior years due primarily to higher component costs impacting Server, Networking, and Hybrid Cloud segments coupled with increased supply chain and logistics expenses [S13]. This resulted in an operating loss of $437 million in FY2025 versus operating profits exceeding $2 billion in previous years largely because of goodwill impairment charges and merger-related expenses tied to integrating Juniper Networks.

Operating cash flow fell sharply by nearly one-third to $2.9 billion while capital expenditure remained sizable at $2.29 billion as investments were made in supply chain optimization and R&D [F1][S13]. Despite this operational strain, HPE maintained dividend payouts around $684 million annually but curtailed share repurchases compared to prior years reflecting prudence amid integration investments.

Business Segments & Strategic Focus

Recent organizational changes consolidated Server, Hybrid Cloud, and Financial Services into one Cloud & AI segment reflecting the company’s focus on data-first modernization solutions addressing traditional IT workloads alongside new AI-centric computing demands [S14][S22].

- Cloud & AI: Encompasses general-purpose servers alongside workload-optimized systems for supercomputing, AI training/inference infrastructure including fanless liquid cooling tech that powers large-scale deployments at government and commercial customers globally [S14][S16]. Storage offerings include cloud-native solutions under HPE Alletra plus data protection services aligned with GreenLake flexibility.

- Networking: Expanded post-Juniper acquisition with hardware such as Wi-Fi access points; switches; routers; plus software-managed networking via Mist AI platforms providing end-to-end orchestration with embedded AI analytics powering "AI for Networks" initiatives foundational for next-gen enterprise networks.

- Corporate Investments & Other: Includes advisory services, telco solutions transitioned out of Networking segment post-reorg alongside Hewlett Packard Labs focusing on future tech exploration.

The added scale from Juniper enables HPE to bundle hardware-software-services in AI-driven networking that integrates tightly with its cloud platform—promoting differentiated hybrid multi-cloud experiences with automated scalability via GreenLake’s pay-per-use models [S4][S10].

Growth Drivers & Challenges Ahead

Growth Catalysts:

- Increasing adoption of AI workloads requires high-performance compute paired with next-gen secure network fabrics where HPE’s combined server-network offerings claim leadership.

- Expansion of edge data volumes fuels demand for seamless distributed cloud management delivered through GreenLake’s consumption-based approach.

- The evolution toward hybrid multi-cloud architectures across industries aligns well with HPE’s holistic product portfolio combining hardware, software-defined infrastructure, and flexible financing solutions.

- Synergy realization from Juniper integration targeting at least $600 million annual savings by fiscal 2028 through headcount optimization and supply chain efficiency investments supports margin improvement over time [S13].

Constraints & Risks:

- Supply chain disruptions persist notably for GPUs critical in accelerated computing nodes; these constraints have pressured margins and delayed customer acceptance timelines particularly for newer generation products driving uneven demand across segments [S1][S10].

- Heightened competitive environment including from Dell Technologies combining strong Infrastructure Solutions Group growth exemplifies market pressure forcing continual innovation investments just to maintain share [N5][N9][S5].

- Macroeconomic uncertainties such as tariff fluctuations elevate component prices adding cost pressures despite pricing adjustments efforts; geopolitical tensions compound risks on sourcing and logistics hubs primarily concentrated across Asia-Pacific regions vulnerable to regulatory or conflict risks [S1][S6][S20].

- Execution risk remains prevalent around successful completion and integration of acquisitions beyond Juniper plus maintaining intellectual property defenses especially amid evolving AI IP laws which pose potential litigation or compliance costs [S11][S12][S18].

Capital Allocation & Financial Returns

HPE displays disciplined capital allocation balancing growth investment while returning capital via dividends:

- Return on Equity currently approximates a low ~0.2% given minimal net income margin despite equity base near $24.7 billion reflecting recent operating losses offsetting equity gains [F1].

- Operating Free Cash Flow estimated at approximately $627 million (operating cash flow minus capex) indicates constrained cash generation relative to historical levels though still positive overall allowing sustained dividend payments (~$684 million annually).

- Share repurchases have been modest ($202 million FY2025), down from prior years suggesting cautious management stance amidst reorganization costs combined with strategic investment priorities including R&D spend sustained despite margin pressure ($600 million+ synergy-related investment planned over midterm) [F1][S13].

This conservative allocation approach underscores management’s prioritization on funding transformational initiatives while maintaining shareholder returns even as near-term profit recovery timelines remain uncertain.

What To Watch Next (Analysis)

While explicit company guidance on upcoming milestones post-Q1 FY26 is not directly cited in filings or news around the March earnings release date [N1,N3], key indicators include:

- Progression on integration synergies from Juniper alongside stabilization of margins especially within the Networking unit.

- Adoption rates of GreenLake subscriptions reflecting customer shift toward subscription/aaS models underpinning recurring revenue base expansion.

- Resolution or easing of supply chain bottlenecks particularly GPU sourcing influencing both revenue recognition pacing and margin trajectories.

- Competitive positioning against peers such as Dell which recently reported strengthening growth suggesting sector momentum capable of sustaining if macro environment holds stable.

- Monitoring geopolitical developments impacting trade policies affecting input cost inflation or operational continuity given HPE’s broad geographic exposure.

Conclusion

Hewlett Packard Enterprise remains positioned strategically well within the burgeoning edge-to-cloud ecosystem leveraged by advanced AI-driven networking integrated with flexible hybrid-cloud solutions supported by GreenLake's consumption model.

However, the transition is not without friction: elevated operational costs stemming from merger integration combined with supply chain pressures have compressed profitability despite continued revenue growth driven by industry megatrends.

Capital discipline appears prudent amidst these headwinds balancing innovation investment against cash returns including steady dividends but tempered buybacks.

The coming periods will be pivotal to assess how effectively HPE can translate scale advantages into sustainable profit recovery while navigating an increasingly complex regulatory landscape around technology evolution especially AI plus global geopolitical uncertainties impacting supply chains.

Disclaimer: This analysis is provided solely for informational purposes based on available public documents as of March 10, 2026, without any investment advice or recommendations concerning Hewlett Packard Enterprise Co or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments